One of the key components of the CARES Act was the Paycheck Protection Program, a $500 billion lifeline to American businesses dealing with the effects of the COVID-19 pandemic and the resulting public health measures that slowed commerce across the country. Like any significant financial program, the PPP came with tax questions. The program provided participants with loans rather than grants, but those loans would be forgiven if taxpayers complied with the conditions of that program. Normally, loan forgiveness results in income to the beneficiary, but Congress provided an exemption for those amounts under the PPP. Taxpayers would therefore get to keep their entire grants if they complied with the conditions of the program. Or so many thought.

Continue reading “PPP Deductibility: Will anyone think of the States?”Category: State and Local Taxes

How the Espinoza Tax Credits Work

By Sam Brunson

On Tuesday the Supreme Court issued its opinion in Espinoza, holding that Montana couldn’t prohibit “student scholarship organizations” from making tuition payments to religiously-affiliated private schools. I wrote about the decision over on the Nonprofit Law Prof Blog.

After writing the post, I saw this entry in a SCOTUSblog symposium on the Espinoza decision. And, like the authors of that piece, I found the Supreme Court’s decision unsurprising (for reasons that I mention on the other blog). But one part of their analysis jumped out at me as reflecting a critical misunderstanding of the way Montana’s tax credit scheme worked.

Specifically, the authors wrote:

The secular instruction in these schools means that the state gets full secular value for its money. There are complications in putting a dollar amount on this secular value. It might be the schools’ full cost, given that they satisfy compulsory-education requirements. Or some of the cost might be attributed to teaching religion. But one thing we know: the secular value is far more than zero. A $2,250 tuition voucher (the amount involved in the court’s 2002 decision in Zelman v. Simmons-Harris) can easily be allocated entirely to secular value. All the more so in Espinoza, where the tax credit was capped at $150.

(Emphasis mine.)

This paragraph isn’t critical to the blog post; it’s not mentioned in the majority’s analysis. And yet I’m afraid it may have been in the back of the mind of the Justices. Because, after all, what’s $150 out of private school tuition? Continue reading “How the Espinoza Tax Credits Work”

Taking Control of the State Tax Base During the Pandemic

COVID-19 has impacted society in nearly every dimension, and state and local governments have been hit especially hard. Those governments are simply not equipped to deal with major revenue shocks like those that accompany a global pandemic. In that vein, a group of scholars has joined forces to create Project SAFE (State Actions in Fiscal Emergencies), which is focused on providing research-backed policy recommendations for states. Among the project’s areas of focus is how states can help themselves by modifying their own taxing and spending programs and priorities.

One of the features of state taxation that I have been looking at quite a bit in recent years is states’ conformity practices—states using the federal tax code for purposes of defining their own tax bases. Continue reading “Taking Control of the State Tax Base During the Pandemic”

Updated Working Paper on Pandemic Regulation Includes Analysis of the CARES Act, H.R. 748

My co-authors and I (Hiba Hafiz, Shu-Yi Oei, and Natalya Shnitser) have just posted an updated version of our Working Paper, Regulating in Pandemic: Evaluating Economic and Financial Policy Responses to the Coronavirus Crisis. The Working Paper is revised and updated to incorporate the provisions of H.R. 748 (the “Coronavirus Aid, Relief, and Economic Security Act” or the “CARES” Act) enacted into law on March 27, 2020. In addition, the revised draft considers recent action by the Federal Reserve, the Department of Labor, and other agencies all through the analytical framework we offer for evaluating these initiatives.

Jussie Smollett and the Illinois Film Tax Credit

By Sam Brunson

On Tuesday, Joe Magats, first assistant state’s attorney for Cook County, announced that he was dropping the charges against actor Jussie Smollett. Instead of a trial and punishment, Smollett agreed to forfeit his $10,000 bond and do community service.

Cook County prosecutors say this is a relatively normal type of alternative prosecution, one that prosecutors have recommended for over 5,700 offenders. It allows prosecutors to use their resources to prosecute violent offenders.

Not surprisingly, there’s some outrage about this alternative prosecution, notably from Chicago Mayor Rahm Emanuel and CPD Superintendent Eddie Johnson. But this is a tax blog, not a criminal justice blog, so questions about the justice (or not) of dropping Smollett’s prosecution are outside of our usual scope. Which is why I’m going to focus, instead, on Illinois Representative Michael McAuliffe and his terrible, horrible, no good, very bad bill. Continue reading “Jussie Smollett and the Illinois Film Tax Credit”

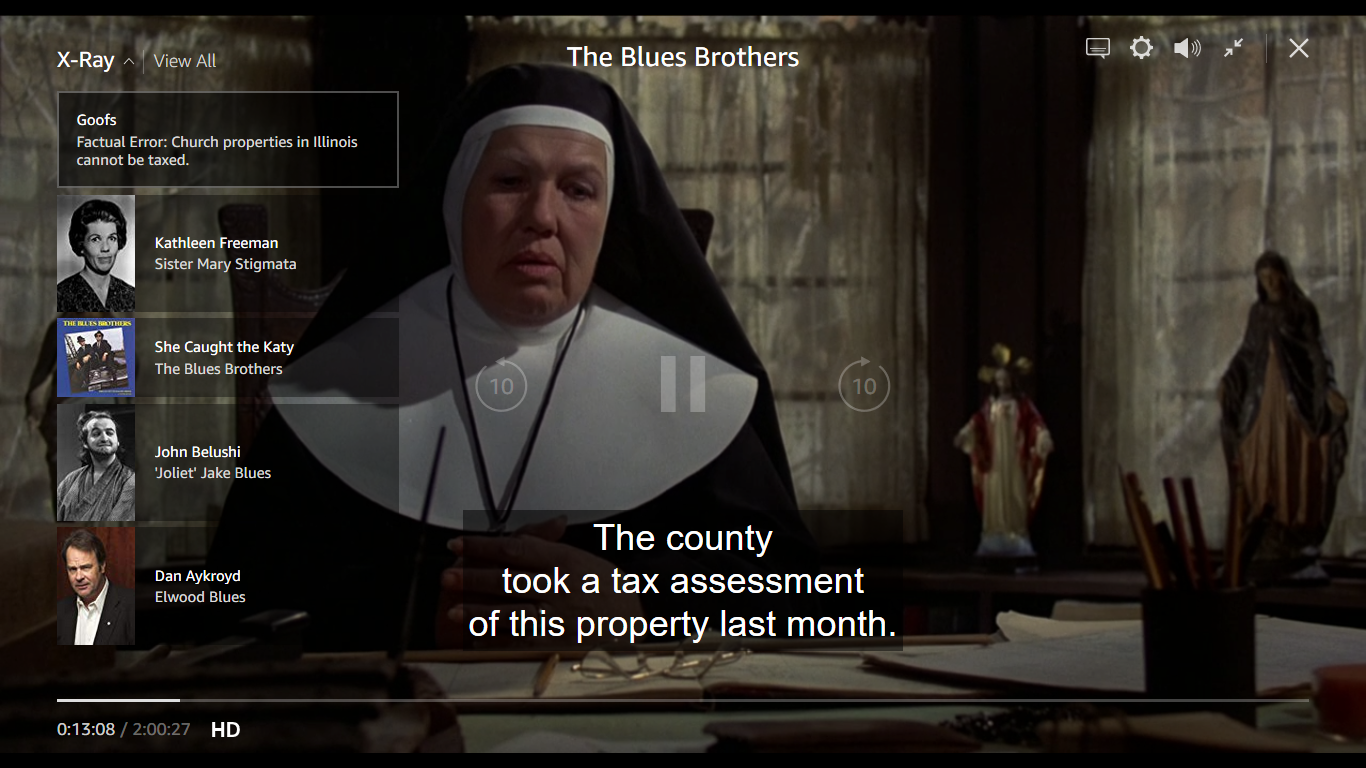

A Mission From God: Blues Brothers and Tax

By Sam Brunson

On February 1, Amazon Prime Video started streaming Blues Brothers. Now, in spite of its being one of the great movies of the 20th century, and having one of the greatest soundtracks ever, I hadn’t seen it in years, and definitely not since I moved to Chicago. So I decided to watch it, both because I love the movie and because I wanted to see its view of Chicago now that I know this city.

I remembered that the plot revolved around Jake and Elwood trying to raise $5,000 for the orphanage they grew up in or the orphanage will be closed, but I’d forgotten that the $5,000 was to pay the orphanage’s property tax assessment:

I’d also never watched a movie with Amazon’s X-Ray feature before. And X-Ray announced that the motivation for their mission from God is a factual error, because Illinois doesn’t tax church property.

Is that true? Continue reading “A Mission From God: Blues Brothers and Tax”

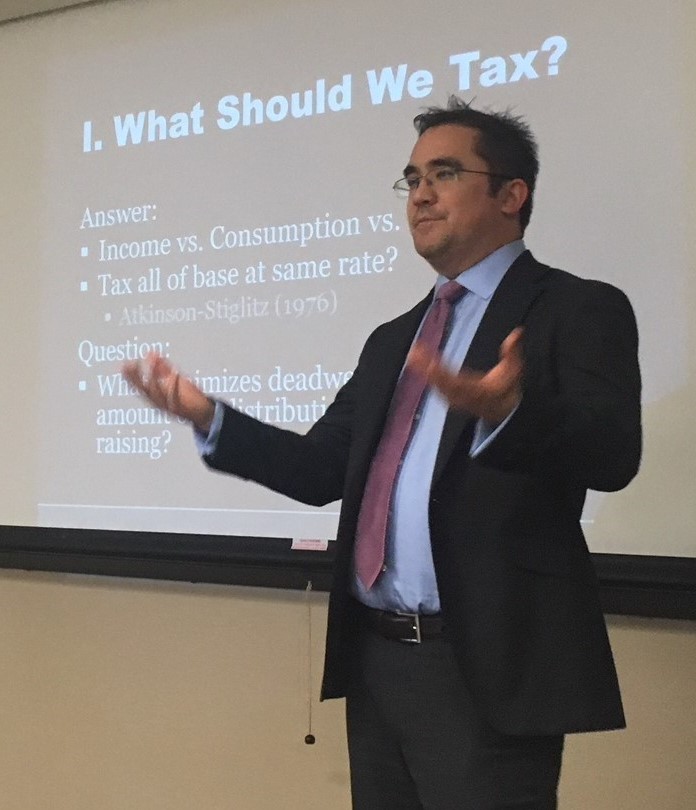

IU Tax Policy Colloquium: Hayashi, “Countercyclical Tax Bases”

By: Leandra Lederman

On April 5, Indiana University Maurer School of Law’s Tax Policy Colloquium welcomed Andrew Hayashi from the University of Virginia School of Law. Andrew presented his fascinating new paper, “Countercyclical Tax Bases.” (The paper isn’t publicly available yet, but Andrew offered to share it by email with interested readers.)

The paper argues that the choice of tax base should take into account what tax base is most helpful to the economy in recessions. It points out that recessions are not rare; between 1980 and 2010, there were 5 recessions, covering 16% of that period. The paper does two main things. First, it provides interesting stylized examples showing how, following an economic shock that reduces income or housing value, three types of tax bases (income, sales, and property) each interact with household credit constraints and adjustment costs (committed consumption of housing) to either stabilize or aggravate the negative economic shock. These examples illustrate quantitatively how different tax bases can affect taxpayer behavior in a recession, and thus the local economy.

Second, the paper contains an original empirical study of county tax bases for 2007-2014, to see the effect of tax bases on the recessions of 2001 and the Great Recession of 2008-2009. Andrew combined data from the Government Finance Database, Zillow, the FBI’s Uniform Crime Reports, and the IRS’s Statistics of Income, among other places. Although the results for the two recessions were not identical, Andrew generally found in his OLS regressions that counties that relied more on property taxes had smaller increases in unemployment during the two recessions and may have recovered from the recession more quickly. Sales taxes generally had countercyclical effects, as well, particularly in stabilizing government revenues during the Great Recession. In general, counties that were most reliant on income taxes suffered the most in the two recessions (though the results for income taxes generally were not statistically significant). Continue reading “IU Tax Policy Colloquium: Hayashi, “Countercyclical Tax Bases””

Tax Panels at the 2019 AALS Annual Meeting

By: Shu-Yi Oei

The Association of American Law Schools will be holding the 2019 AALS Annual Meeting in New Orleans, LA from January 2-6, 2019. This year, I’m the chair of the AALS Tax Section. Your section officers (Heather Field, Erin Scharff, Kathleen Thomas, Larry Zelenak, Shu-Yi Oei) are pleased to bring you four tax-related panels at the Annual Meeting. Two are Tax Section main programs, and two are programs we are cosponsoring with other sections. Details below.

We’re also organizing a dinner for Taxprofs (and friends) on Saturday, January 5. If you’re on the distribution list, you should have received an email about that and how to RSVP. If you’d like more details, please email me.

We hope to see many of you at the Annual Meeting!

Tax Section Main Program: The 2017 Tax Changes, One Year Later (co-sponsored with Legislation & Law of the Political Process, and Trusts and Estates)

Saturday, January 5, 2019, 10:30 am – 12:15 pm

Moderator:

Shu-Yi Oei, Boston College Law School

Speakers:

Karen C. Burke, University of Florida Fredric G. Levin College of Law

Ajay K. Mehrotra, Northwestern University Pritzker School of Law

Leigh Osofsky, University of North Carolina School of Law

Daniel N. Shaviro, New York University School of Law

Program Description: Congress passed H.R. 1, a major piece of tax legislation, at the end of 2017. The new law made important changes to the individual, business, and cross-border business taxation. This panel will discuss the changes and the issues and questions that have arisen with respect to the new legislation over the past year. Panelists will address several topics, including international tax reform, choice-of-entity, the new qualified business income deduction (§ 199A), federal-state dynamics, budgetary and distributional impacts, the state of regulatory guidance, technical corrections and interpretive issues, and the possibility of follow-on legislation.

Business meeting at program conclusion.

New Voices in Tax Policy and Public Finance (cosponsored with Nonprofit and Philanthropy Law and Employee Benefits and Executive Compensation)

Saturday, January 5, 2019, 3:30-5:15 pm

Paper Presenters:

Ariel Jurow Kleiman (University of San Diego School of Law), Tax Limits and Public Control

Natalya Shnitser (Boston College Law School), Are Two Employers Better Than One? An Empirical Assessment of Multiple Employer Retirement Plans

Gladriel Shobe (BYU J. Reuben Clark Law School), Economic Segregation, Tax Reform, and the Local Tax Deduction

Commenters:

Heather Field (UC Hastings College of the Law)

David Gamage (Maurer School of Law, Indiana University at Bloomington)

Andy Grewal (University of Iowa College of Law)

Leo Martinez (UC Hastings College of the Law)

Peter Wiedenbeck (Washington University in St. Louis School of Law)

Program Description:

This program showcases works-in-progress by scholars with seven or fewer years of teaching experience doing research in tax policy, public finance, and related fields. These works-in-progress were selected from a call for papers. Commentators working in related areas will provide feedback on these papers. Abstracts of the papers to be presented will be available at the session. For the full papers, please email the panel moderator.

Continue reading “Tax Panels at the 2019 AALS Annual Meeting”

Inheriting Property Tax Assessments in California

By Sam Brunson

I grew up in the north suburbs of San Diego and, while I haven’t lived in Southern California in a couple decades now, I try to keep a vestigial self-identification as a Southern Californian.[fn1] Part of that self-identification is listening to the Voice of San Diego podcast; it keeps me vaguely up-to-date on current politics in San Diego.

Today, as I was walking to the pet store, I turned on the most recent episode. On that episode, the regular hosts were joined by Liam Dillon, now a reporter for the LA Times. And they mentioned a story he’d recently written, about the inheritance of property tax rates in California. Continue reading “Inheriting Property Tax Assessments in California”

Paying with Data

By Adam B. Thimmesch

It is an oft repeated adage that if you are not paying for a product, then you are the product. This comment has traditionally been directed at products like Google, Facebook, and Instagram, but it is not just large software companies that are making use of consumer data as “payment” for their services. NPR recently published a story about a café in Rhode Island that is taking this one step further. They sell coffee in exchange for data.

According to the article, students and faculty at Brown University are the only customers allowed at the shop, and students get free coffee by allowing the coffee shop to gather and sell their data. The students also receive corporate pitches from the café’s workers. (Apparently professor data is not so valuable. They have to pay.) According to the article:

To get the free coffee, university students must give away their names, phone numbers, email addresses and majors, or in Brown’s lingo, concentrations. Students also provide dates of birth and professional interests, entering all of the information in an online form. By doing so, the students also open themselves up to receiving information from corporate sponsors who pay the cafe to reach its clientele through logos, apps, digital advertisements on screens in stores and on mobile devices, signs, surveys and even baristas. Continue reading “Paying with Data”

A Series of Series? Tax, Regulation, and Faculty Workshops at Boston College Law School

I do love a good faculty workshop. Reading and spiritedly discussing the work of other academics always fills me with energy and inspiration for my own projects. Plus, it’s great to be able to spend time with new and old friends and find out what’s been baking in their brains.

Here at BC Law, I’m fortunate to be involved in two exciting workshop series: the BC Tax Policy Workshop and the BC Regulation and Markets Workshop. Both kicked off this week: On Tuesday, we hosted Professor Jens Dammann from the University of Texas at Austin and heard about his paper, “Deference to Delaware Corporate Law Precedents and Shareholder Wealth: An Empirical Analysis.” Today, we welcomed Professor Ajay Mehrotra (Northwestern Law; Executive Director, American Bar Foundation) and had a lively discussion of his book project, “The VAT Laggard: A Comparative History of U.S. Resistance to the VAT.” Tomorrow, BC Law will have its first Faculty Colloquium of the semester. Professor Guy-Uriel Charles (Duke Law; visiting at Harvard Law) will present “The American Promise: Rethinking Voting Rights Law and Policy for a Divided America.”

You can never have too many workshops!

Below are the dates and speakers for the remainder of the semester. If you’re a Boston-area law professor and are interested in attending or would like to be on our workshop email list, just let me know.

Tax Policy Workshop (Fall 2018):

Thursday September 13, 2018

Ajay Mehotra (Northwestern, and American Bar Foundation):

The VAT Laggard: A Comparative History of US Resistance to the VAT

(co-sponsored with BC Legal History Workshop)

Tuesday November 6, 2018

Andrew Hayashi (UVA): title TBD

Tuesday Nov. 13, 2018

Cliff Fleming (BYU): title TBD

Tuesday November 27, 2018

Emily Satterthwaite (University of Toronto): title TBD

(co-sponsored with BC Regulation and Markets Workshop)

More Post-Wayfair Thoughts: Sales Tax?

By now, anyone who reads this post should be aware that the Supreme Court decided South Dakota v. Wayfair and overruled its physical presence rule last week. States now have expanded authority to require the collection of their consumption taxes by remote vendors like online retailers. Coverage of the case and its impact on states and vendors has been widespread, including my preliminary thoughts offered on this blog and with Darien Shanske and David Gamage elsewhere.

One aspect of the coverage that would usually drive state tax aficionados crazy is the continued reference to the case as involving sales tax.

For a long time, many of us have smugly corrected folks (often only in our own minds) and noted that it is the state use tax that is at issue when we are talking about online sales. That may be no more.

The South Dakota law that was challenged in Wayfair indeed requires remote vendors to collect the state’s sales tax rather than the state’s use tax. Historically, that would have been a big problem, but it didn’t trouble Justice Kennedy or the other members of the majority. This may require broader thinking than just analyzing what Wayfair means about states’ powers over remote vendors. The Court’s decision in Wayfair may have done much more than just overrule Quill; it may have unsettled some even longer-standing doctrine in this area.

South Dakota v. Wayfair: First Impressions

The Supreme Court issued a 5-4 decision overruling its long-standing physical presence rule in South Dakota v. Wayfair this morning. That decision provides welcomed relief to states (and to those of us who already pay use tax) and will have significant short- and long-term consequences. My reactions to Wayfair will surely extend for a long period of time, but here are some brief first thoughts.

The Basics

The Court’s holding was very limited: the physical presence rule no longer governs the determination of what constitutes a “substantial nexus” under the dormant Commerce Clause. The Court also found that nexus existed in the case based on the challengers’ connections with South Dakota. Finally, the Court did not bless the South Dakota statute completely, but remanded the decision back to the South Dakota courts to hear non-nexus based challenges to the law, if any exist.

What this means is that states will be able to continue (or expand) their efforts to require the collection of sales/use tax by online vendors. States will also need to monitor whether and how Congress responds, but they should be able to craft their laws to avoid state-court scrutiny until that time.

Continue reading “South Dakota v. Wayfair: First Impressions”

The Gig Economy Battles Continue: 9th Circuit Weighs In on Seattle Uber Driver Ordinance

By: Diane Ring

Today the 9th Circuit weighed in on the validity of a Seattle ordinance that requires businesses contracting with taxi-drivers, for-hire transportation companies, and “transportation network companies” to bargain with drivers if a majority of drivers seek such representation. The legislation, which effectively enables Uber and Lyft drivers to unionize, drew objections from Uber, Lyft and the Chamber of Commerce— which sued the City of Seattle. In an August 2017 post, I reviewed the ruling of the U.S. District Court for the Western District of Washington, which concluded that the Seattle ordinance was an appropriate exercise of the city’s authority and did not violate the Sherman Act (because of state action immunity) and was not preempted by the National Labor Relations Act (NLRA). So what did the 9th Circuit say?

Call for Papers: New Voices in Tax Policy and Public Finance (2019 AALS Annual Meeting, New Orleans, LA)

The AALS Tax Section committee is pleased to announce the following Call for Papers:

CALL FOR PAPERS

AALS SECTION ON TAXATION WORKS-IN-PROGRESS SESSION

2019 ANNUAL MEETING, JANUARY 2-6, 2019, NEW ORLEANS, LA

NEW VOICES IN TAX POLICY AND PUBLIC FINANCE

(co-sponsored by the Section on Nonprofit and Philanthropy Law and Section on Employee Benefits and Executive Compensation)

The AALS Section on Taxation is pleased to announce the following Call for Papers. Selected papers will be presented at a works-in-progress session at the 2019 AALS Annual Meeting in New Orleans, LA from January 2-6, 2019. The works-in-progress session is tentatively scheduled for Saturday, January 5.

Eligibility: Scholars teaching at AALS member schools or non-member fee-paid schools with seven or fewer years of full-time teaching experience as of the submission deadline are eligible to submit papers. For co-authored papers, both authors must satisfy the eligibility criteria.

Due Date: 5 pm, Wednesday, August 8, 2018.

Form and Content of submission: We welcome drafts of academic articles in the areas of taxation, tax policy, public finance, and related fields. We will consider drafts that have not yet been submitted for publication consideration as well as drafts that have been submitted for publication consideration or that have secured publication offers. However, drafts may not have been published at the time of the 2019 AALS Annual Meeting (January 2019). We welcome legal scholarship across a wide variety of methodological approaches, including empirical, doctrinal, socio-legal, critical, comparative, economic, and other approaches.

Submission method: Papers should be submitted electronically as Microsoft Word documents to the following email address: tax.section.cfp@gmail.com by 5 pm on Wednesday, August 8, 2018. The subject line should read “AALS Tax Section CFP Submission.” By submitting a paper for consideration, you agree to attend the 2019 AALS Annual Meeting Works-in-Progress Session should your paper be selected for presentation.

Submission review: Papers will be selected after review by the AALS Tax Section Committee and representatives from co-sponsoring committees. Authors whose papers are selected for presentation will be notified by Thursday, September 28, 2018.

Additional information: Call-for-Papers presenters will be responsible for paying their own AALS registration fee, hotel, and travel expenses. Inquiries about the Call for Papers should be submitted to: AALS Tax Section Chair, Professor Shu-Yi Oei, Boston College Law School, oeis@bc.edu.