Call for Papers

AALS Section on Nonprofit and Philanthropy Law

2023 Annual Meeting

January 4-7

San Diego, CA

Nonprofits & Philanthropy

The AALS Section on Nonprofit and Philanthropy Law announces a call for papers to be presented as works-in-progress in our committee session at the 2023 AALS Annual Meeting in San Diego, CA from January 4-7, 2023.

The Section seeks submissions on a variety of topics and methodological approaches related to Nonprofit and Philanthropy Law. Given the recent importance and novelty of state nonprofit law, we are especially interested in scholarship that illuminates, elucidates, and otherwise engages with the work states are doing in the nonprofit world, but are happy to consider any scholarship in the field. We are interested in all states of article development.

Eligibility: Scholars teaching at AALS member or nonmember fee-paid schools. We particularly encourage new voices in the field to submit.

Due Date: June 15, 2022

Form and Content of Submission: Submissions may range from early drafts to articles that have been submitted for publication, but not articles that will have already been published by January 7, 2023.

Submission Method: please submit papers electronically to sbrunson@luc.edu with “AALS Nonprofit and Philanthropy Law Submission” in the email subject line.

Submission Review: Papers will be selected for inclusion in the program after review by members of the AALS Section on Nonprofit and Philanthropy Law.

Additional Information: Presenters are responsible for their own expenses associated with the conference. If you have any questions, please contact the chair, Sam Brunson, at sbrunson@luc.edu.

Category: Nonprofits

Whistleblowers and Disinformation: “Whistling at the Fake” Roundtable

By Diane Ring

Information lies at the heart of a sound democracy, good governance, and well-grounded decision making, whether at the individual, community, business, or government level. Yet every day we see how misinformation and disinformation undermines all of these goals.

In response to this problem, a new research project, Whistling at the Fake (with Dr. Costantino Grasso as PI, and funded by NATO’s Public Diplomacy Division) aims to address the gap in the public’s understanding of the full scope and impact of misinformation and disinformation, and to empower the general public and regulators with tools, suggestions and recommendations for the future. The project focuses in particular on the role of whistleblowers and other informed insiders in “exposing misleading and hostile information activities and increasing public resistance to acts of this nature.”

As part of its project, Whistling at the Fake is hosting Roundtables on zoom– the first of which is this Friday, January 28, 2022 at 10:00am EST. The Roundtable, “Disinformation and the Private Sector” includes three sessions: (1) Exploring the Phenomenon, (2) Disinformation and Corporate Power and Wealth, and (3) Special Issues and Recommendations. The international panel includes experts from law, media, business, research, along with whistleblowers. To join what should be an amazing zoom Roundtable, register here!

Project Veritas and Illegality

By Sam Brunson

On November 5—two days after the presidential election—James O’Keefe posted an interview with a postal worker claiming that he and his colleagues were instructed to backdate ballots that they received after election day. The next day he filed an affidavit swearing that he and his colleagues had been instructed to continue picking up ballots after the November 3 deadline.

After an interview with U.S. Postal Service investigators, Richard Hopkins, the postal worker, recanted his statements. He also told investigators that his affidavit had been written by Project Veritas, the organization O’Keefe founded and with which he is associated.

Project Veritas, it turns out, is a tax-exemption organization. And its association with Hopkins may have put its exemption at risk. By signing an untrue affidavit, Hopkins almost certainly broke the law. And several attorneys interview in the Salon story say that Project Veritas may also have broken the law as a result of its involvement in the false affidavit.

Continue reading “Project Veritas and Illegality”How the Espinoza Tax Credits Work

By Sam Brunson

On Tuesday the Supreme Court issued its opinion in Espinoza, holding that Montana couldn’t prohibit “student scholarship organizations” from making tuition payments to religiously-affiliated private schools. I wrote about the decision over on the Nonprofit Law Prof Blog.

After writing the post, I saw this entry in a SCOTUSblog symposium on the Espinoza decision. And, like the authors of that piece, I found the Supreme Court’s decision unsurprising (for reasons that I mention on the other blog). But one part of their analysis jumped out at me as reflecting a critical misunderstanding of the way Montana’s tax credit scheme worked.

Specifically, the authors wrote:

The secular instruction in these schools means that the state gets full secular value for its money. There are complications in putting a dollar amount on this secular value. It might be the schools’ full cost, given that they satisfy compulsory-education requirements. Or some of the cost might be attributed to teaching religion. But one thing we know: the secular value is far more than zero. A $2,250 tuition voucher (the amount involved in the court’s 2002 decision in Zelman v. Simmons-Harris) can easily be allocated entirely to secular value. All the more so in Espinoza, where the tax credit was capped at $150.

(Emphasis mine.)

This paragraph isn’t critical to the blog post; it’s not mentioned in the majority’s analysis. And yet I’m afraid it may have been in the back of the mind of the Justices. Because, after all, what’s $150 out of private school tuition? Continue reading “How the Espinoza Tax Credits Work”

IU Tax Policy Colloquium: Layser, “When, Where, And How To Design Community-Oriented Place-Based Tax Incentives”

By: Leandra Lederman

On January 23, the Indiana University Maurer School of Law welcomed our first Tax Policy Colloquium guest of the year: Prof. Michelle Layser from the University of Illinois College of Law. She presented her draft paper on the design of place-based tax incentives, then called “When, Where, And How To Design Community-Oriented Place-Based Tax Incentives,” and since retitled “How Place-Based Tax Incentives Can Reduce Geographic Inequality.” An updated draft is available on SSRN.

Shelly explained that this draft is the second paper in a multi-part project she is conducting on place-based tax incentives. Last year, she published the first piece in the series, “A Typology of Place-Based Investment Tax Incentives,” 25 Wash. & Lee J. Civ. Rights & Soc. Just. 403 (2019). Place-based tax incentives are geography-based incentives that generally are intended to help low-income areas by fostering investment in those areas. The 2019 article distinguished among place-based tax incentives on two dimensions: direct and indirect tax subsidies and spatially-oriented versus community-oriented incentives. “Direct tax subsidies provide tax breaks directly to businesses that invest in low-income communities.” (p. 415) Indirect tax subsidies are instead provided to investors in such business (pp. 417-18). She cites as examples the New Markets Tax Credit (NMTC) of IRC § 45D and the Opportunity Zones (OZ) provisions in IRC § 1400Z-1 et seq. (The OZ provisions are the most oddly numbered Internal Revenue Code sections I’ve ever seen!). Spatially-oriented tax incentives focus on specific geographically-defined Continue reading “IU Tax Policy Colloquium: Layser, “When, Where, And How To Design Community-Oriented Place-Based Tax Incentives””

More on the College Admissions Scandal

By Sam Brunson

On Wednesday, I posted about how tax law played a central role in the college admissions scandal. As I’ve read through a little more of the affidavit, I decided to highlight two additional detail in this whole scandal, details that suggest that, for at least some of the participants, the tax consequences were very important.

Bruce Isackson and Facebook Stock

Bruce Isackson is the president of WP Investments, a real estate investment and development fund.[fn1] According to the affidavit, he used the fake athlete thing (soccer for the older daughter, rowing for the younger) to get two daughters into USC. He seems to have also paid for his younger daughter to get a better ACT score.

What’s interesting for purposes of this post is how he paid. Continue reading “More on the College Admissions Scandal”

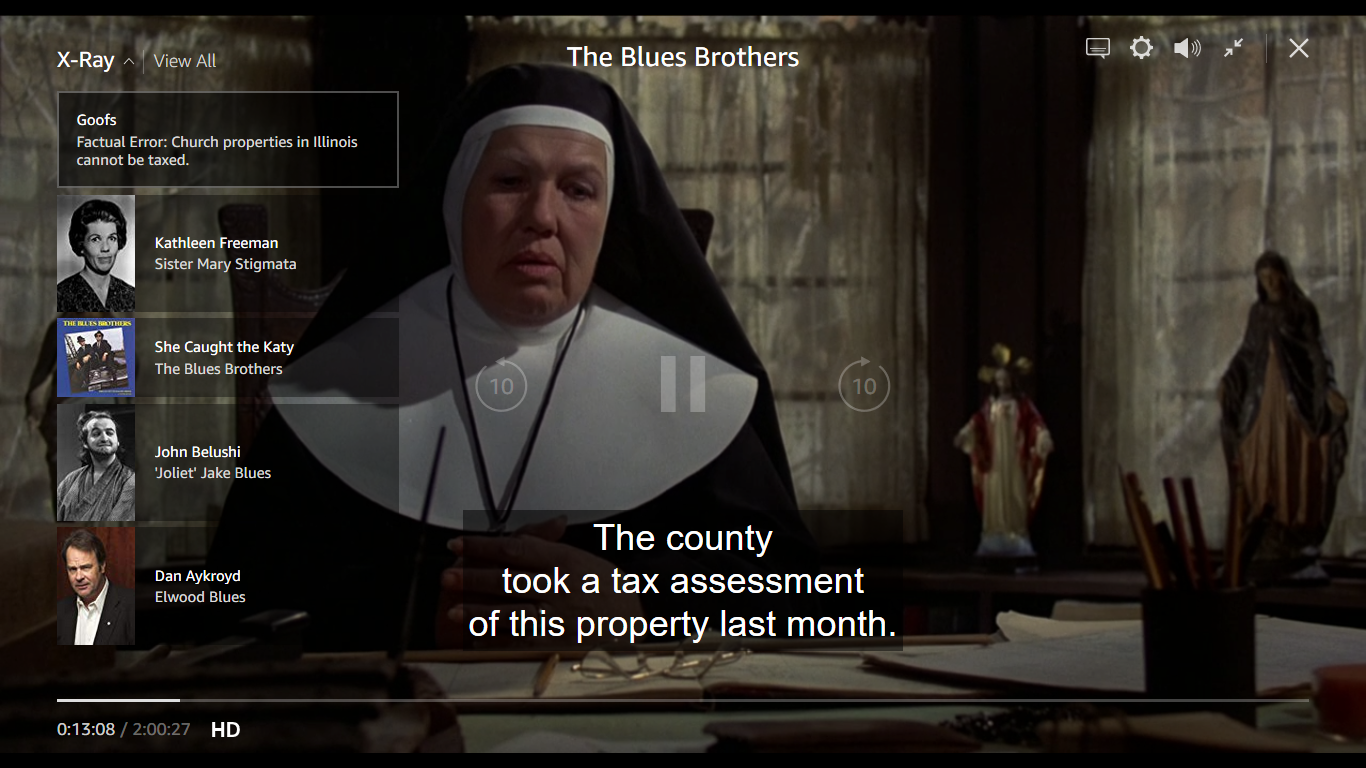

A Mission From God: Blues Brothers and Tax

By Sam Brunson

On February 1, Amazon Prime Video started streaming Blues Brothers. Now, in spite of its being one of the great movies of the 20th century, and having one of the greatest soundtracks ever, I hadn’t seen it in years, and definitely not since I moved to Chicago. So I decided to watch it, both because I love the movie and because I wanted to see its view of Chicago now that I know this city.

I remembered that the plot revolved around Jake and Elwood trying to raise $5,000 for the orphanage they grew up in or the orphanage will be closed, but I’d forgotten that the $5,000 was to pay the orphanage’s property tax assessment:

I’d also never watched a movie with Amazon’s X-Ray feature before. And X-Ray announced that the motivation for their mission from God is a factual error, because Illinois doesn’t tax church property.

Is that true? Continue reading “A Mission From God: Blues Brothers and Tax”

The Trump Foundation and the Private Foundation Termination Tax

Michael Cohen’s accusations against President Trump in his statement before the House Committee on Oversight and Reform yesterday include arranging for a straw bidder to purchase a portrait of President Trump at an auction, using Trump Foundation funds to repay the fake bidder, and keeping the art for himself. As part of the New York Attorney General’s stipulation agreement with The Trump Foundation, the foundation must sell two other Trump portraits it currently owns.

This stipulation agreement with the New York Attorney General has saved the Trump Foundation from a burdensome penalty tax in connection with the involuntary termination. As had been widely reported at the end of last year, the New York Attorney General announced on December 18 that its investigation had found “a shocking pattern of illegality involving the Trump Foundation – including unlawful coordination with the Trump presidential campaign, repeated and willful self-dealing, and much more.” Under the stipulation agreement, the Trump Foundation will dissolve and submit to the court a list of non-for-profit organizations to receive the Foundation’s remaining assets. The Attorney General and the state court will need to approve the organizations that receive the Trump Foundation’s funds. Continue reading “The Trump Foundation and the Private Foundation Termination Tax”

The IRS Did Not Violate the First Amendment in Declining to Exempt Organizations to Help Marijuana Dealers

Several commentators have called attention to the statement of the IRS in Revenue Procedure 2018-5, just reiterated in Rev. Proc. 2019-1, that it will not issue a determination letter recognizing exemption from income tax for “an organization whose purpose is directed to the improvement of business conditions of one or more lines of business relating to an activity involving controlled substances (within the meaning of schedule I and II of the Controlled Substances Act) which is prohibited by Federal law regardless of its legality under the law of the state in which such activity is conducted.”

These commentators suggest that this position could constitute impermissible viewpoint discrimination in violation of the First Amendment. I do not view the IRS announcement in this way. Instead, I see it as an application of the long-standing principle denying exemption to entities with an illegal purpose or engage primarily in illegal activities.

The illegality doctrine has long prevented exemption under section 501(c)(3), the category that encompasses what we generally call charities. In the words of Section 101(c) of the ALI Draft Restatement of the Law of Charitable Nonprofit Organizations, “[a] purpose is not charitable if it is not lawful, its performance requires the commission of criminal or tortious activity, or it is otherwise contrary to fundamental public policy.” Continue reading “The IRS Did Not Violate the First Amendment in Declining to Exempt Organizations to Help Marijuana Dealers”

Tax Panels at the 2019 AALS Annual Meeting

By: Shu-Yi Oei

The Association of American Law Schools will be holding the 2019 AALS Annual Meeting in New Orleans, LA from January 2-6, 2019. This year, I’m the chair of the AALS Tax Section. Your section officers (Heather Field, Erin Scharff, Kathleen Thomas, Larry Zelenak, Shu-Yi Oei) are pleased to bring you four tax-related panels at the Annual Meeting. Two are Tax Section main programs, and two are programs we are cosponsoring with other sections. Details below.

We’re also organizing a dinner for Taxprofs (and friends) on Saturday, January 5. If you’re on the distribution list, you should have received an email about that and how to RSVP. If you’d like more details, please email me.

We hope to see many of you at the Annual Meeting!

Tax Section Main Program: The 2017 Tax Changes, One Year Later (co-sponsored with Legislation & Law of the Political Process, and Trusts and Estates)

Saturday, January 5, 2019, 10:30 am – 12:15 pm

Moderator:

Shu-Yi Oei, Boston College Law School

Speakers:

Karen C. Burke, University of Florida Fredric G. Levin College of Law

Ajay K. Mehrotra, Northwestern University Pritzker School of Law

Leigh Osofsky, University of North Carolina School of Law

Daniel N. Shaviro, New York University School of Law

Program Description: Congress passed H.R. 1, a major piece of tax legislation, at the end of 2017. The new law made important changes to the individual, business, and cross-border business taxation. This panel will discuss the changes and the issues and questions that have arisen with respect to the new legislation over the past year. Panelists will address several topics, including international tax reform, choice-of-entity, the new qualified business income deduction (§ 199A), federal-state dynamics, budgetary and distributional impacts, the state of regulatory guidance, technical corrections and interpretive issues, and the possibility of follow-on legislation.

Business meeting at program conclusion.

New Voices in Tax Policy and Public Finance (cosponsored with Nonprofit and Philanthropy Law and Employee Benefits and Executive Compensation)

Saturday, January 5, 2019, 3:30-5:15 pm

Paper Presenters:

Ariel Jurow Kleiman (University of San Diego School of Law), Tax Limits and Public Control

Natalya Shnitser (Boston College Law School), Are Two Employers Better Than One? An Empirical Assessment of Multiple Employer Retirement Plans

Gladriel Shobe (BYU J. Reuben Clark Law School), Economic Segregation, Tax Reform, and the Local Tax Deduction

Commenters:

Heather Field (UC Hastings College of the Law)

David Gamage (Maurer School of Law, Indiana University at Bloomington)

Andy Grewal (University of Iowa College of Law)

Leo Martinez (UC Hastings College of the Law)

Peter Wiedenbeck (Washington University in St. Louis School of Law)

Program Description:

This program showcases works-in-progress by scholars with seven or fewer years of teaching experience doing research in tax policy, public finance, and related fields. These works-in-progress were selected from a call for papers. Commentators working in related areas will provide feedback on these papers. Abstracts of the papers to be presented will be available at the session. For the full papers, please email the panel moderator.

Continue reading “Tax Panels at the 2019 AALS Annual Meeting”

Seventh Circuit Preview: Gaylor v. Mnuchin

By Sam Brunson

A week from Wednesday, the Seventh Circuit will hear oral arguments in Gaylor v. Mnuchin, the case in which the Freedom From Religion Foundation is challenging the constitutionality of the parsonage allowance.[fn1]

In anticipation of the oral arguments, Professor Anthony Kreis and I are hosting a preview of the case this Wednesday, October 17, at noon. It will be in room 105 of the Corboy Law Center, 25 E. Pearson St., Chicago, IL 60611. There will be pizza, soda, and some great discussion. If you’re free for that hour (and, of course, in or near Chicago), I’d love to see you there! RSVP here. Continue reading “Seventh Circuit Preview: Gaylor v. Mnuchin”

A Series of Series? Tax, Regulation, and Faculty Workshops at Boston College Law School

I do love a good faculty workshop. Reading and spiritedly discussing the work of other academics always fills me with energy and inspiration for my own projects. Plus, it’s great to be able to spend time with new and old friends and find out what’s been baking in their brains.

Here at BC Law, I’m fortunate to be involved in two exciting workshop series: the BC Tax Policy Workshop and the BC Regulation and Markets Workshop. Both kicked off this week: On Tuesday, we hosted Professor Jens Dammann from the University of Texas at Austin and heard about his paper, “Deference to Delaware Corporate Law Precedents and Shareholder Wealth: An Empirical Analysis.” Today, we welcomed Professor Ajay Mehrotra (Northwestern Law; Executive Director, American Bar Foundation) and had a lively discussion of his book project, “The VAT Laggard: A Comparative History of U.S. Resistance to the VAT.” Tomorrow, BC Law will have its first Faculty Colloquium of the semester. Professor Guy-Uriel Charles (Duke Law; visiting at Harvard Law) will present “The American Promise: Rethinking Voting Rights Law and Policy for a Divided America.”

You can never have too many workshops!

Below are the dates and speakers for the remainder of the semester. If you’re a Boston-area law professor and are interested in attending or would like to be on our workshop email list, just let me know.

Tax Policy Workshop (Fall 2018):

Thursday September 13, 2018

Ajay Mehotra (Northwestern, and American Bar Foundation):

The VAT Laggard: A Comparative History of US Resistance to the VAT

(co-sponsored with BC Legal History Workshop)

Tuesday November 6, 2018

Andrew Hayashi (UVA): title TBD

Tuesday Nov. 13, 2018

Cliff Fleming (BYU): title TBD

Tuesday November 27, 2018

Emily Satterthwaite (University of Toronto): title TBD

(co-sponsored with BC Regulation and Markets Workshop)

New Paper on Tax Legislative Process and Statutory Drafting

Shu-Yi Oei

For those readers in search of some light summer reading, Leigh Osofsky (UNC Law) and I have been working on a paper on statutory drafting, entitled “Constituencies and Control in Statutory Drafting: Interviews with Government Tax Counsels.” We finally got around to posting it on SSRN, here.

In the paper, we report findings from interviews we conducted with government tax counsels who have participated in the tax legislative process, in which we asked questions about various aspects of drafting and creating tax legislation. In addition to reporting our findings, we also discuss the implications of our research for statutory interpretation, tax system design, and the legislative process.

For readers interested in legislation, tax drafting, statutory interpretation, tax shelters, and the political process, the paper is probably worth a look. Feel free to contact either of us with comments.

Dog Owners of Tribeca

My favorite news story from last week: it turns out that ten years ago, a group of dog owners in Tribeca installed a lock on a public New York City dog park, and started charging people a membership fee—$120 a year—if they wanted to use the (public!) park. They created a list of rules, most of which focused on keeping others out, and, if you violated the rules, you were kicked out, and apparently had to let your dog play with other proletariat dogs. (N.b.: this state of affairs lasted ten years, until the city finally cut the lock and reopened the park to the public.)

This story has everything: self-absorbed and self-righteous New Yorkers; a funny thing I read on Twitter while sitting in church Sunday; a bit on this week’s Wait Wait Don’t Tell Me. And, perhaps more importantly, a tax angle. See, these snooty, selfish New Yorkers did something more than hijack a public space—they formed a tax-exempt organization to manage it. Continue reading “Dog Owners of Tribeca”

Call for Papers: New Voices in Tax Policy and Public Finance (2019 AALS Annual Meeting, New Orleans, LA)

The AALS Tax Section committee is pleased to announce the following Call for Papers:

CALL FOR PAPERS

AALS SECTION ON TAXATION WORKS-IN-PROGRESS SESSION

2019 ANNUAL MEETING, JANUARY 2-6, 2019, NEW ORLEANS, LA

NEW VOICES IN TAX POLICY AND PUBLIC FINANCE

(co-sponsored by the Section on Nonprofit and Philanthropy Law and Section on Employee Benefits and Executive Compensation)

The AALS Section on Taxation is pleased to announce the following Call for Papers. Selected papers will be presented at a works-in-progress session at the 2019 AALS Annual Meeting in New Orleans, LA from January 2-6, 2019. The works-in-progress session is tentatively scheduled for Saturday, January 5.

Eligibility: Scholars teaching at AALS member schools or non-member fee-paid schools with seven or fewer years of full-time teaching experience as of the submission deadline are eligible to submit papers. For co-authored papers, both authors must satisfy the eligibility criteria.

Due Date: 5 pm, Wednesday, August 8, 2018.

Form and Content of submission: We welcome drafts of academic articles in the areas of taxation, tax policy, public finance, and related fields. We will consider drafts that have not yet been submitted for publication consideration as well as drafts that have been submitted for publication consideration or that have secured publication offers. However, drafts may not have been published at the time of the 2019 AALS Annual Meeting (January 2019). We welcome legal scholarship across a wide variety of methodological approaches, including empirical, doctrinal, socio-legal, critical, comparative, economic, and other approaches.

Submission method: Papers should be submitted electronically as Microsoft Word documents to the following email address: tax.section.cfp@gmail.com by 5 pm on Wednesday, August 8, 2018. The subject line should read “AALS Tax Section CFP Submission.” By submitting a paper for consideration, you agree to attend the 2019 AALS Annual Meeting Works-in-Progress Session should your paper be selected for presentation.

Submission review: Papers will be selected after review by the AALS Tax Section Committee and representatives from co-sponsoring committees. Authors whose papers are selected for presentation will be notified by Thursday, September 28, 2018.

Additional information: Call-for-Papers presenters will be responsible for paying their own AALS registration fee, hotel, and travel expenses. Inquiries about the Call for Papers should be submitted to: AALS Tax Section Chair, Professor Shu-Yi Oei, Boston College Law School, oeis@bc.edu.

{kind=link}