We’ve started a new YouTube series we wanted to share with our readers! It’s called “Break Into Tax” (BiT) and can be found at tinyurl.com/BreakIntoTax.

The idea behind BiT is that we’ll discuss and break down tax-related concepts, broadly defined. This includes issues that may be of interest to law students and others newer to tax or to particular issues. The topics we plan to cover include substantive tax law concepts, tax policy concerns, the study of taxation, and the pursuit of tax as a career. We also welcome suggestions for topics in the comments on our videos!

We come at the issues from the perspective of tax law professors in the U.S. and Canada with cross-border interests. The BiT series is not at all designed to be of interest only to people from these two countries. We expect to focus on concepts that are foundational enough or general enough to be of broad interest.

Our introduction video, located here, is a good place to start. It shares more about us and the BiT channel. Our first playlist covers Tax Policy Colloquia: what are they, how to ask a good question in a tax workshop, and tips for students writing reaction papers.

The Tax Policy Colloquium at Indiana University Maurer School of Law, which I’ve been blogging about, ran in person in Bloomington until our Spring Break. The fourth talk of the semester was given by Prof. Orly Mazur of SMU Dedman School of Law on March 5, 2020. She presented her interesting law-and-technology paper titled “Can Blockchain Revolutionize Tax Compliance?” (In general, she argued that it can’t: blockchain is unlikely to dramatically change tax enforcement by, for example, replacing third-party information reporting.)

The subsequent IU Tax Policy Colloquium talk, by Prof. Rita de la Feria of the University of Leeds School of Law, was on March 27. She presented a paper, coauthored with Michael Walpole of UNSW, titled “The Impact of Public Perceptions on VAT Rates Policy,” which is part of a larger project proposing a progressive VAT. The paper argues that, although having a single consumption tax rate that is broadly applied is most equitable, there typically are numerous exemptions and/or lower rates, for political economy reasons.

Prof. de la Feria

With the move to online classes due to the pandemic, this talk occurred via Zoom. It was unfortunate that, due to the pandemic, we were not able to host Rita in Bloomington. However, the silver lining was that I was able to invite tax experts and other faculty from all over the world to attend. Rita and I also both publicized the talk on social media. As a result, several academics and other tax experts either asked to attend, or, if they saw the notice too late, asked if there is a video they could watch, which there is. In addition to me, Rita, and the students in the class, there were 22 attendees, which produced a terrific discussion. The students later told me how wonderful it was to have so many international tax experts asking questions and making comments. Continue reading “Virtual Tax Policy Colloquia”→

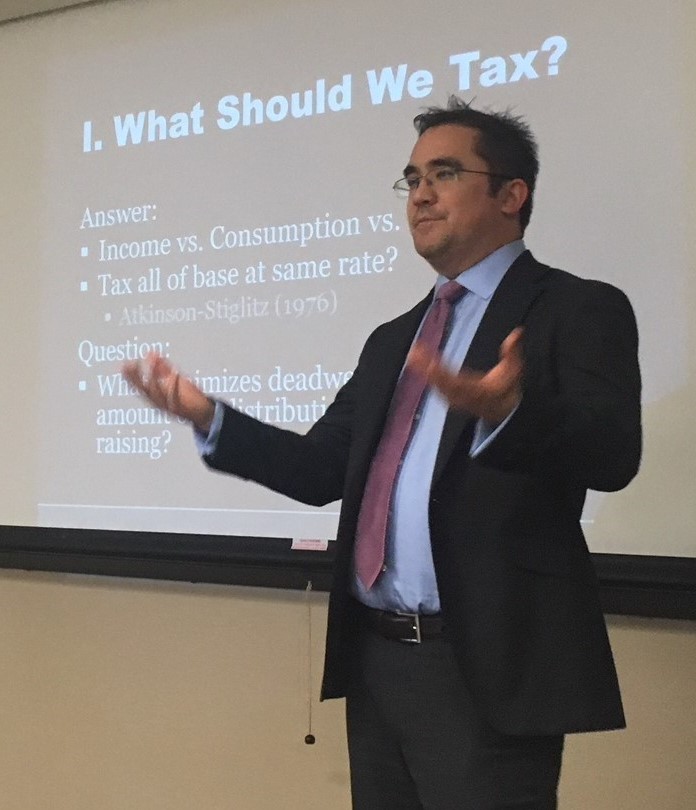

On February 20, 2020, the Indiana University Maurer School of Law welcomed our third Tax Policy Colloquium guest of the year: Prof. Zachary Liscow from Yale Law School. Zach presented his draft article titled “Equality, Taxation, and Law and Economics In the 21st Century.”

As its title suggests, the article takes on income inequality. The article argues that the standard approach of redistributing only through the tax system and hinging non-tax policies on efficiency is misguided. It makes the case that (1) people want more equality than we currently have; (2) people do not think of tax and transfers together and fungibly trade off between types of redistribution but instead have (conceptually) “separate public accounts” for taxation and other government activities; (3) in part, that is because people have an idea of “desert” that is linked to cash income, resulting in resistance to heavily redistributionist taxation; and thus (4) rather than striving for “optimal” taxation and efficient legal rules, the government should tilt non-tax policies (such as transportation policy) to increase their redistributive aspects. As the abstract states, this argument “turns standard economics prescriptions on their heads.”

The article is fascinating and a compelling read. The idea that people think separately about taxes and transfers seems very plausible. I had not thought before about the idea of desert applying to pre-tax income but it is quite persuasive. It adds a further layer to the argument I made in a 2004 article titled “The Entrepreneurship Effect.” That article argued that the Internal Revenue Code systematically favors business deductions over investment deductions; the difference between them is that the former require labor and the latter do not; and this reflects societal favoritism for entrepreneurship. The idea that “desert” particularly inheres in labor income adds a layer in that it helps source the societal value put on labor income and entrepreneurship. Continue reading “IU Tax Policy Colloquium: Liscow, “Equality, Taxation, and Law and Economics In the 21st Century””→

On February 6, 2020, the Indiana University Maurer School of Law welcomed our second Tax Policy Colloquium guest of the year: Prof. Werner Haslehner from the University of Luxembourg’s Department of Law, who is currently a Global Research Fellow and adjunct professor at NYU Law School. Werner presented his draft essay titled “International Tax Competition—the Good, the Bad, and the Ugly.”

States of course compete for tax base. Werner’s essay explains that “States’ general freedom to act (which we may call sovereignty) and taxpayer’s freedom to choose (which we may call liberty) – although neither is without limits – inescapably lead to competitive pressures and reactions.” (p.4) And some of this competition has been labelled as “harmful” by the OECD, the European Commission, and others. Yet, the essay points out, there is no accepted definition of the phrase “harmful tax competition.” The essay briefly reviews the literature and points out differences in approach to defining this concept. This part of the essay draws in part on Lily Faulhaber’s compelling article, The Trouble with Tax Competition: From Practice to Theory, 71 Tax L. Rev. 311 (2018), which pointed out the lack of definitional consensus and offered a typology of tax competition.

Werner’s essay further argues that, as commonly understood, there is no economic standard that supports a distinction between “harmful” and other types of tax competition. The essay thus proposes to replace the phrase “harmful tax competition” with “unfair tax competition.” (p.13) The essay specifically proposes “to refer as a basis for such a constraint to one of the most salient principles of moral philosophy: Immanuel Kant’s categorical imperative. According to this norm’s first formulation, one is to ‘act only in accordance with that maxim through which one can at the same time will that it become a universal law’.” (p.16). The essay provides two examples of behaviors that would be considered “unfair” under this standard: (1) ring-fencing (the provision of a tax benefit only to foreigners, not domestic taxpayers) and (2) secrecy (which, in response to a question I posed, Werner clarified refers to “secrecy as a service”—assisting foreign taxpayers in tax evasion). Continue reading “IU Tax Policy Colloquium: Haslehner, “International Tax Competition—The Good, the Bad, and the Ugly””→

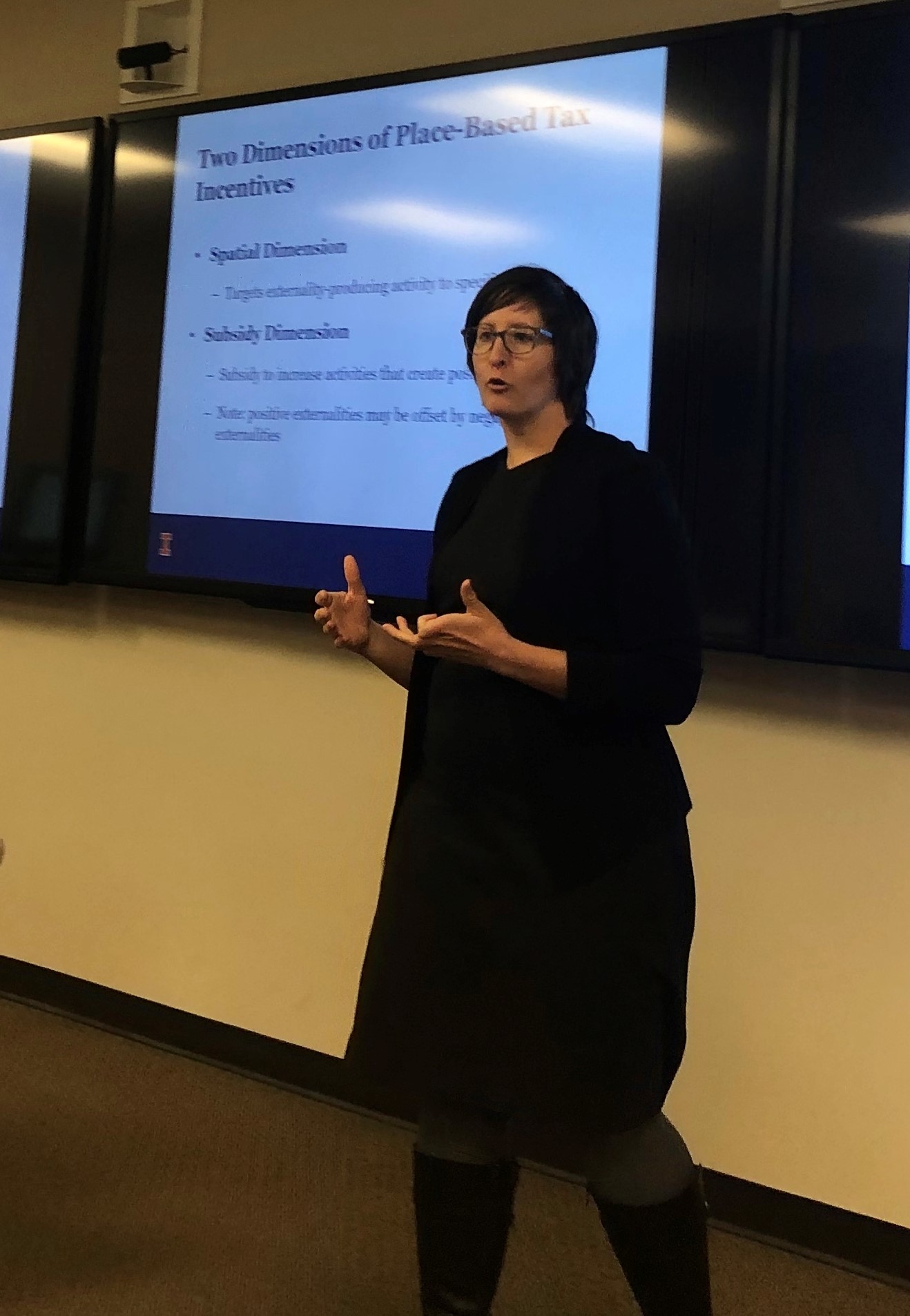

On January 23, the Indiana University Maurer School of Law welcomed our first Tax Policy Colloquium guest of the year: Prof. Michelle Layser from the University of Illinois College of Law. She presented her draft paper on the design of place-based tax incentives, then called “When, Where, And How To Design Community-Oriented Place-Based Tax Incentives,” and since retitled “How Place-Based Tax Incentives Can Reduce Geographic Inequality.” An updated draft is available on SSRN.

Shelly explained that this draft is the second paper in a multi-part project she is conducting on place-based tax incentives. Last year, she published the first piece in the series, “A Typology of Place-Based Investment Tax Incentives,” 25 Wash. & Lee J. Civ. Rights & Soc. Just. 403 (2019). Place-based tax incentives are geography-based incentives that generally are intended to help low-income areas by fostering investment in those areas. The 2019 article distinguished among place-based tax incentives on two dimensions: direct and indirect tax subsidies and spatially-oriented versus community-oriented incentives. “Direct tax subsidies provide tax breaks directly to businesses that invest in low-income communities.” (p. 415) Indirect tax subsidies are instead provided to investors in such business (pp. 417-18). She cites as examples the New Markets Tax Credit (NMTC) of IRC § 45D and the Opportunity Zones (OZ) provisions in IRC § 1400Z-1 et seq. (The OZ provisions are the most oddly numbered Internal Revenue Code sections I’ve ever seen!). Spatially-oriented tax incentives focus on specific geographically-defined Continue reading “IU Tax Policy Colloquium: Layser, “When, Where, And How To Design Community-Oriented Place-Based Tax Incentives””→

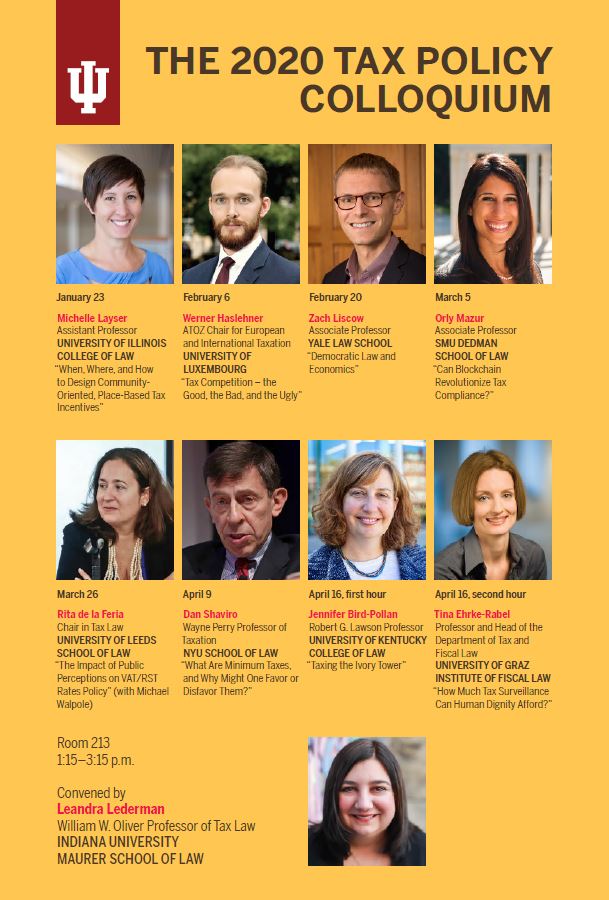

Indiana University Maurer School of Law’s Tax Policy Colloquium will reconvene this Thursday, January 23, 2020. Michelle Layser from the University of Illinois College of Law will start us off, presenting her new paper titled “When, Where, and How to Design Community Oriented Place-Based Tax Incentives.” It’s a really interesting study of tax-expenditure design in the context of geography-based tax incentives. Prof. Layser’s paper includes original “heat maps” of Chicago showing areas with high poverty levels, areas with high numbers of low-wage jobs, areas that are eligible for the New Markets Tax Credit, and areas designated as Opportunity Zones. The talk promises to be really interesting!

The full schedule of talks is listed below, after the jump, and is also shown in the poster pictured above. Overall, this year’s line-up of speakers is more international than usual, following my wonderful Fulbright research stay at the University of Luxembourg in Spring 2019.

As I did the last time I ran the Colloquium, I’m planning to blog each workshop afterwards, with permission of the speakers. If you will be in Bloomington and are interested in attending one or more workshops, just let me know and I can add you to the email list or send you a particular paper once I receive it. (Most of the paper drafts will not be publicly available.) Continue reading “The IU Maurer Law School’s 2020 Tax Policy Colloquium”→

On February 28, Indiana University Maurer School of Law’s Tax Policy Colloquium, hosted this year by my colleague David Gamage, welcomed Vanessa Williamson from the Brookings Institution. Vanessa presented a report that is due to be released at the end of March on a “Filer Voter” experiment she conducted at Volunteer Income Tax Assistance (VITA) sites in Cleveland, Ohio and Dallas, Texas.

For those who may not be familiar with it, VITA is an IRS-run program that offers free tax return preparation (generally federal and state) for taxpayers who made $54,000 in income or less (for 2018) and meet certain other requirements. An IRS web page provides training materials and certification tests for volunteers. The IRS works with local groups in that it provides VITA grants to partner organizations. For example, in Bloomington, the VITA program is run by United Way of Monroe County.

Vanessa’s Filer Voter experiment involved offering some taxpayers who come to VITA sites for tax-return preparation the opportunity to register to vote. The experiment was structured as follows: Each VITA session was divided in half by time, and within each session, the first half or second half was randomly assigned the treatment of offering voter registration, and the other half of the session was the control. The study included collection of demographic information and consent forms from taxpayers in both the treatment and control groups. Continue reading “IU Tax Policy Colloquium: Williamson, Filer Voter: An Experiment Testing Voter Registration at Tax Time”→

On February 14, the Indiana University Maurer School of Law’s Tax Policy Colloquium hosted Larry Zelenak from Duke University School of Law. Larry presented his fun new paper, co-authored with his colleague Rich Schmalbeck, “The NCAA and the IRS: Life at the Intersection of College Sports and the Federal Income Tax.” Larry really hit this one out of the park, with a crowd that was nearly standing-room-only! Larry also hosted a terrific Valentine’s evening event, “Tax Sitcom Night,” featuring three classic sitcom episodes in which couples encounter the federal income tax together. I’ll discuss each of these briefly in this blog post.

Larry and Rich’s paper argues that the IRS has not done as much as Congress to cut back on “unreasonably generous tax treatment” of college athletics. The paper covers four principal topics, which Larry explained was a combination of Rich’s work on two issues and Larry’s on the other two. The four topics are:

The possible application of the unrelated business income tax to college sports;

the federal income tax treatment of athletic scholarships;

the recently changed tax treatment of charitable deductions for most of the cost of season tickets to college ball games; and

the new 21% excise tax of IRC § 4960 on compensation in excess of $1 million on certain employees of tax-exempt organizations.

Each of these topics is interesting in its own right, and together they make a strong case that the IRS, and Congress at times, have tilted the playing field in favor of college athletics at the expense of protection of the federal fisc. I won’t give a play-by-play of these four issues here, as the paper does a great job of it and is available on SSRN, but I will mention a couple of highlights. Continue reading “Zelenak: IU Tax Policy Colloquium, “The NCAA and the IRS” & Tax Sitcom Night”→

On April 5, Indiana University Maurer School of Law’s Tax Policy Colloquium welcomed Andrew Hayashi from the University of Virginia School of Law. Andrew presented his fascinating new paper, “Countercyclical Tax Bases.” (The paper isn’t publicly available yet, but Andrew offered to share it by email with interested readers.)

The paper argues that the choice of tax base should take into account what tax base is most helpful to the economy in recessions. It points out that recessions are not rare; between 1980 and 2010, there were 5 recessions, covering 16% of that period. The paper does two main things. First, it provides interesting stylized examples showing how, following an economic shock that reduces income or housing value, three types of tax bases (income, sales, and property) each interact with household credit constraints and adjustment costs (committed consumption of housing) to either stabilize or aggravate the negative economic shock. These examples illustrate quantitatively how different tax bases can affect taxpayer behavior in a recession, and thus the local economy.

Second, the paper contains an original empirical study of county tax bases for 2007-2014, to see the effect of tax bases on the recessions of 2001 and the Great Recession of 2008-2009. Andrew combined data from the Government Finance Database, Zillow, the FBI’s Uniform Crime Reports, and the IRS’s Statistics of Income, among other places. Although the results for the two recessions were not identical, Andrew generally found in his OLS regressions that counties that relied more on property taxes had smaller increases in unemployment during the two recessions and may have recovered from the recession more quickly. Sales taxes generally had countercyclical effects, as well, particularly in stabilizing government revenues during the Great Recession. In general, counties that were most reliant on income taxes suffered the most in the two recessions (though the results for income taxes generally were not statistically significant). Continue reading “IU Tax Policy Colloquium: Hayashi, “Countercyclical Tax Bases””→

Indiana University Maurer School of Law’s 2019 Tax Policy Colloquium will kick off on Thursday, January 17. My colleague David Gamage is hosting the Colloquium this year, and I’m really excited to hear from the terrific line-up of speakers! Andrew Hayashi from Viriginia Law School will kick off the semester with his work in progress, Countercyclical Tax Bases.

As I explained last year, The Tax Policy Colloquium is a course for students that features a series of speakers. The structure involves a background session with the students in alternate weeks, to help them get up to speed on the concepts presented in the paper draft. The workshops are open to the law school community and interested guests. They are usually attended not only by the students in the course but also by me, David Gamage, senior tax attorney/Maurer alumnus Tim Riffle, and a few other faculty, typically law school colleagues and/or tax or economics faculty from other schools on campus. We also invite other attorneys practicing in Bloomington and Indianapolis, tax Continue reading “The IU Maurer Law School’s 2019 Tax Policy Colloquium”→

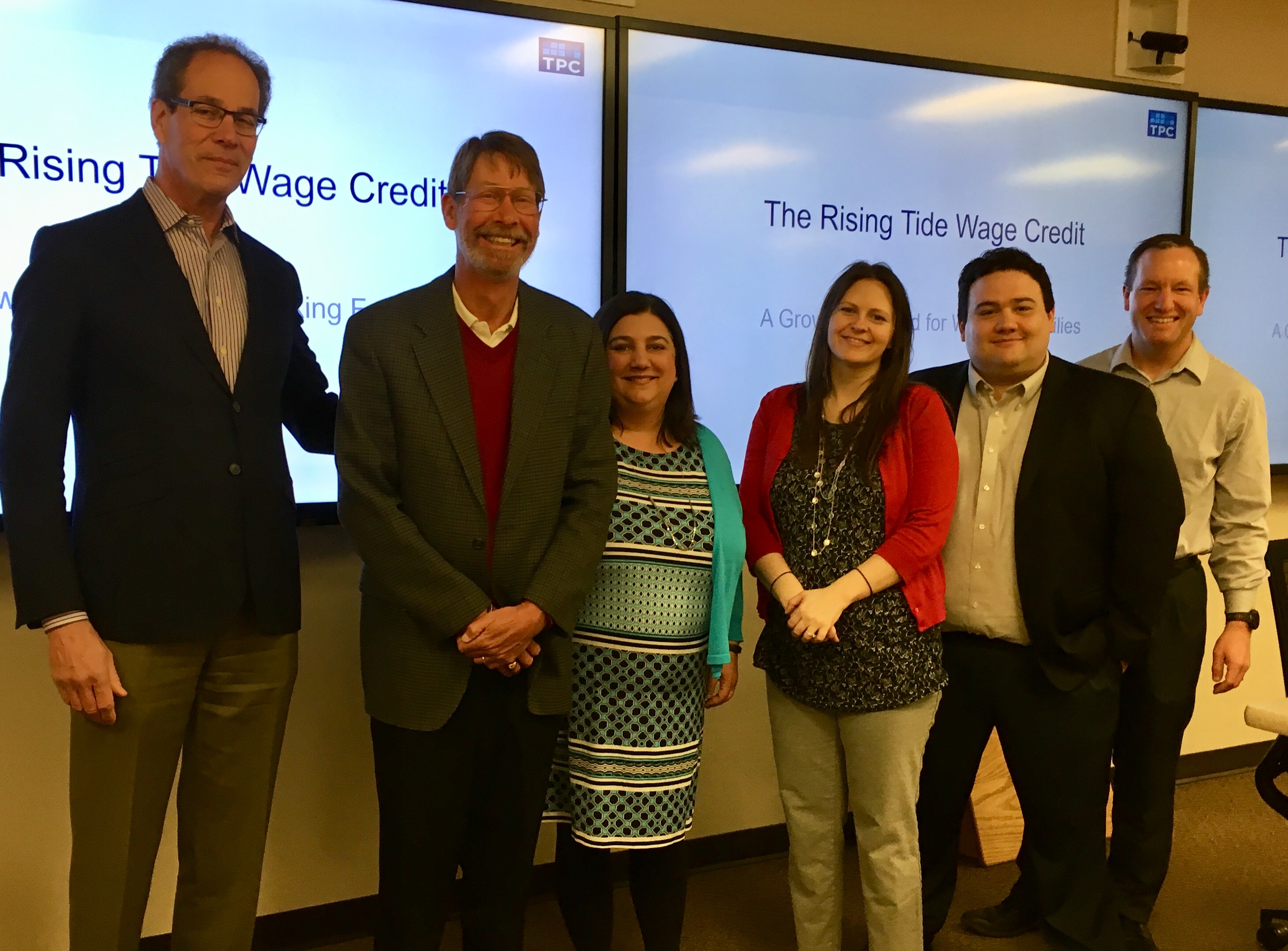

Left to right: Len Burman, Tim Riffle, Leandra Lederman, Karen Ward, Frank DiPietro, Brad Heim

By: Leandra Lederman

On April 5, the Indiana University Maurer School of Law’s Tax Policy Colloquium welcomed Len Burman from Syracuse University and the Urban Institute/Tax Policy Center, who presented “The Rising Tide Wage Credit.” This intriguing new paper is not yet publicly available.

The paper proposes replacing the existing Earned Income Tax Credit (EITC) with a new credit, the Rising Tide Wage Credit (RTWC), which, unlike the EITC, would be universal for workers, rather than phased out above low income levels. The RTWC also would differ from the EITC in that the amount of the RTWC would not depend on the number of children the taxpayer has. Instead, the RTWC would be a 100% credit in the amount of a worker’s wages, up to $10,000 of wages. The credit could be claimed on the taxpayer’s tax return, or subject to advance payment via the taxpayer’s employer. Thus, the maximum credit for an unmarried taxpayer would be $10,000, and for a married couple filing jointly would be $20,000. (The credit would not have a marriage penalty.) The credit would be indexed to increase with increases in GDP.

Because the proposed new credit would not vary with the number of children the taxpayer is supporting, the paper also proposes increasing the child tax credit from $2,000 to $2,500, and proposes making the child tax credit fully refundable (rather than partly refundable, as it is under current law). The RTWC and the increase in the child tax credit would be funded by a value added tax (VAT). The paper estimates that the proposal could be fully funded with an 8% VAT, along with federal income tax on the RTWC. A VAT was chosen as the funding mechanism because it is closely correlated with GDP. The paper discusses 3 illustrative examples and includes a table that shows the overall progressivity of the proposal under certain assumptions. Continue reading “IU Tax Policy Colloquium: Burman, “The Rising Tide Wage Credit””→

Left to right: Maicu Díaz de Terán, Tim Riffle, Emily Satterthwaite, Brian Broughman, Leandra Lederman, David Gamage, #taxprofbaby, Pamela Foohey, Austen Parrish

By: Leandra Lederman

On March 22, the Indiana University Maurer School of Law’s Tax Policy Colloquium welcomed Prof. Emily Satterthwaite from the University of Toronto Faculty of Law, who presented “Optional Taxation: Survey Evidence from Ontario Microentrepreneurs.” This interesting new paper is not yet publicly available.

The paper explores Canada’s “small supplier” exemption from value-added tax (VAT) registration. Canada’s exemption allows suppliers with less than CAD $30,000 of sales (turnover) in a year to avoid registering for and complying with the VAT unless they opt in. (This amount is not indexed for inflation, and Emily’s paper explains that this threshold is fairly low.) Although it may seem odd for someone to opt into a tax system, as Emily’s paper explains, some small suppliers have incentives to do so: if they buy supplies subject to VAT, they can offset that against VAT owed, and obtain a refund if VAT paid exceeds VAT due. In addition, some small suppliers may be encouraged by their VAT-registered customers to become part of a formal supply chain, because the VAT those customers pay on inputs is creditable. The downside of registering is the cost of doing so, which includes the requirement to file an annual return regardless of whether VAT is owed. Continue reading “IU Tax Policy Colloquium: Satterthwaite, “Optional Taxation: Survey Evidence from Ontario Microentrepreneurs””→

On March 1, the Indiana University Maurer School of Law welcomed Surly’s own Prof. Diane Ring from Boston College Law School as the fourth speaker of the year in our Tax Policy Colloquium. Diane presented a new paper, which I believe is not yet publicly available, titled “Silos and First Movers In the Sharing Economy Debates.” This interesting paper focuses on the classification of workers in the “sharing” or “gig” economy as employees or independent contractors, arguing that “[t]wo interacting forces create the most serious risk for inadequate policy formulation: (1) silos among legal experts, and (2) first-mover effects.” (Page 1 of the draft.) The silo argument is that lawyers operate in subject areas that are isolated from each other, such that tax experts, for example, fail to perceive the effects of tax-related worker-classification rule changes on non-tax (such as employment) law, and vice versa. The first-mover argument is that the first actors on the worker-classification issue can wield outsized influence, shaping the debate in legal contexts other than the one directly affected.

Left to right: Damage Gamage, Ari Glogower, Leandra Lederman, Tim Riffle

By: Leandra Lederman

On February 15, the Indiana University Maurer School of Law welcomed Prof. Ari Glogower from Ohio State University Moritz College of Law as the third speaker of the year in our Tax Policy Colloquium. Ari presented his paper titled “Taxing Inequality,” which argues in favor of a federal wealth tax and proposes a mechanism for integrating the base of such a tax with the base of the federal income tax. Ari’s paper sparked a really interesting discussion both in and outside the workshop on a wide range of issues, from distributive justice to the mechanics and likely impacts of his proposal.

The paper focused first on why we should have a federal tax on wealth. The draft points to rising economic inequality, and it grounds the need for a wealth tax in the theory of “relative economic power.” That theory, borrowed from political science, focuses on spending power—as opposed to actual spending—as a source of economic power. The basic idea is that the mere ownership pf wealth creates economic power without spending it. Moreover, “excessively unequal distributions of economic resources and market power can result in unequal divisions of political and social power as well.” (p.19) One of Ari’s paper’s contributions is to apply this economic-power theory as a justification for a progressive tax system.

The draft then describes the problem that tax-system designers have in imposing both a wealth tax and an income tax. Because the two types of taxes are imposed on different bases, if the taxes are not coordinated, taxpayers with very different abilities to pay based on their income or wealth may be taxed identically. The paper includes some nice examples of taxpayers with the same income but vastly different stocks of wealth and vice versa. It shows, for example, that a taxpayer with $200,000 of current income and no wealth (or negative wealth in the form of student-loan debt) has lower ability to pay than a taxpayer with $200,000 of current income and $35 million in wealth. (Ari’s talk included a great slide featuring an image of Scrooge McDuck swimming in money as the wealthy taxpayer, but for whatever reason, he resisted our suggestion to rename the paper “Taxing Scrooge McDuck”!) Continue reading “IU Tax Policy Colloquium: Glogower, “Taxing Inequality””→

Left to right: Jake Brooks, Leandra Lederman, Bill Popkin, David Gamage, Tim Riffle

On February 1, the Indiana University Maurer School of Law welcomed Prof. Jake Brooksfrom Georgetown Law School as the second speaker of the year in our Tax Policy Colloquium. Jake presented an early draft of a paper titled “The Case for Incrementalism in Tax Reform,” which led to a lively and interesting discussion about what incrementalism is, what constitutes fundamental reform, how politics may affect the making of tax policy, and whether and how tax law differs from other fields of law.

The paper, which is not yet publicly available, argues that “fundamental tax reform,” while sometimes necessary, should not generally be the goal of tax policy, and that instead, policymakers should take an incremental approach to changing tax laws. “Incrementalism” has a long history in political science, and was first described by Charles Lindblom in an influential 1959 article, “The Science of Muddling Through.” In general, Lindblom’s approach in that article was to reject the urge to use a formal method that involves clarifying the principal goals up front, identifying the means to achieve them, and then analyzing every relevant factor in the decision. Lindblom instead advocated the use of a more casual method that he termed “successive limited comparisons,” which ignored important possible outcomes or alternatives and did not involve distinguishing means and ends. (Page 81 of Lindblom.) Lindblom argued that this “muddling through” approach was not only what was actually practiced by administrators, but also a method for which they need not apologize because administrators are less likely to make serious and lasting mistakes if they proceed through small, incremental changes (pp.86-87). As Jake acknowledges, Lindblom wrote at a time with much more limited ability to model and process large quantities of empirical data. He notes that incrementalism has continued to be an important theory in the literature. Despite technological advances, we cannot see the future, and there remain limits to what empirical data can help us predict.

Jake’s argument is driven in part by arguments in favor of tearing the Internal Revenue Code out by its roots and starting over. I agree with Jake that such an approach seems extremely risky. Policy driven by rhetoric and “horror stories” risks being ill-conceived, hasty, driven by political rent-seeking, and even destructive, as I have written about in the context of IRS reform. But does that necessarily mean that legislative tax changes should take a Lindblom-style incremental approach? Continue reading “IU Tax Policy Colloquium: Brooks, “The Case for Incrementalism in Tax Reform””→

By:

By: