By: Sam Brunson

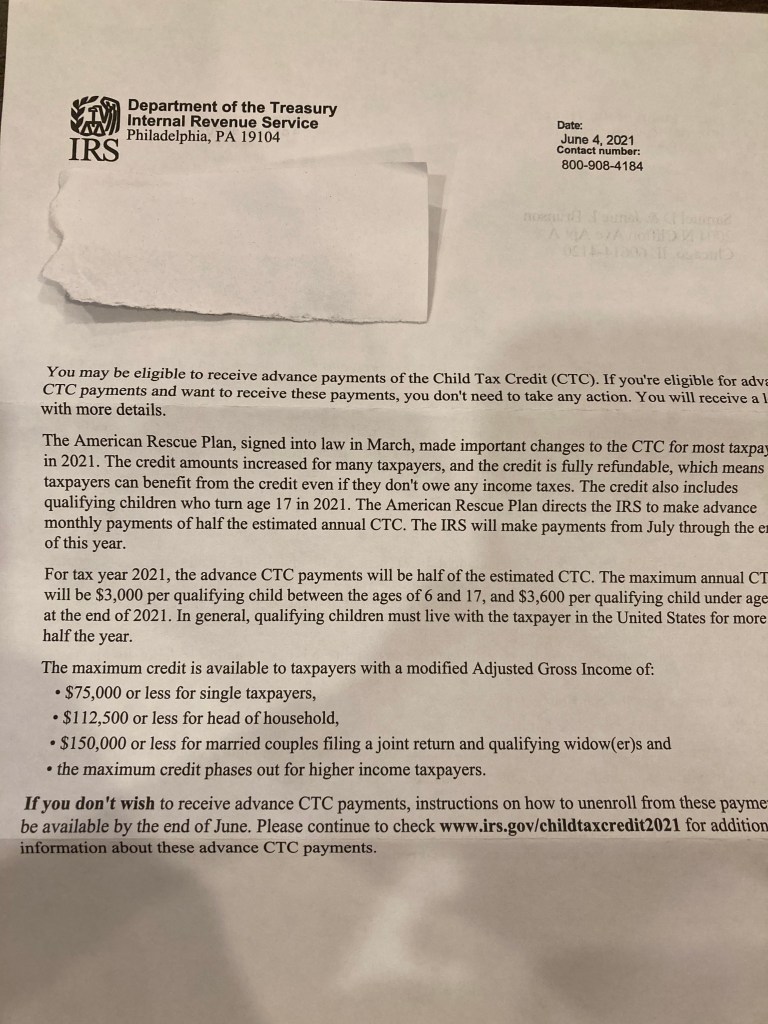

Yesterday my neighbor texted me to mention that three pieces of my mail had been left in his mailbox; he dropped them off in front of my door. Two were just standard junk mail but one is potentially important: a letter from the Department of the Treasury.

Perhaps you also got this letter: it has some important information about the way the the child tax credit now works. In short, the American Rescue Plan, a law signed in March, makes a number of significant changes to the child tax credit.

Two of those changes are particularly notable. First, it increases the amount of the credit to $3,000 for most children and $3,600 for children five and younger.

Second, it makes allows the IRS to make advance payments of the child tax credit. Essentially, unless parents choose otherwise, starting in July the will receive monthly payments of $250 or $300 per child (depending on the child’s age).

Third, the credit is fully refundable. Even if a parent doesn’t have enough income to owe taxes, they will receive the full amount of the child tax credit.

Finally, the age limit for the child tax credit has been increased from 16 to 17. (Note that currently these changes are all temporary–they only apply to 2021, though the may be extended as some point.)

Continue reading “Advance Payments of the Child Tax Credit”

“[W]ork is a valued activity, both for individuals and society; and fulfills the need of an individual to be productive, promotes independence, enhances self-esteem, and allows for participation in the mainstream of life in America.” Rehabilitation Act of 1973

“[W]ork is a valued activity, both for individuals and society; and fulfills the need of an individual to be productive, promotes independence, enhances self-esteem, and allows for participation in the mainstream of life in America.” Rehabilitation Act of 1973