Call for Papers

AALS Section on Nonprofit and Philanthropy Law

2023 Annual Meeting

January 4-7

San Diego, CA

Nonprofits & Philanthropy

The AALS Section on Nonprofit and Philanthropy Law announces a call for papers to be presented as works-in-progress in our committee session at the 2023 AALS Annual Meeting in San Diego, CA from January 4-7, 2023.

The Section seeks submissions on a variety of topics and methodological approaches related to Nonprofit and Philanthropy Law. Given the recent importance and novelty of state nonprofit law, we are especially interested in scholarship that illuminates, elucidates, and otherwise engages with the work states are doing in the nonprofit world, but are happy to consider any scholarship in the field. We are interested in all states of article development.

Eligibility: Scholars teaching at AALS member or nonmember fee-paid schools. We particularly encourage new voices in the field to submit.

Due Date: June 15, 2022

Form and Content of Submission: Submissions may range from early drafts to articles that have been submitted for publication, but not articles that will have already been published by January 7, 2023.

Submission Method: please submit papers electronically to sbrunson@luc.edu with “AALS Nonprofit and Philanthropy Law Submission” in the email subject line.

Submission Review: Papers will be selected for inclusion in the program after review by members of the AALS Section on Nonprofit and Philanthropy Law.

Additional Information: Presenters are responsible for their own expenses associated with the conference. If you have any questions, please contact the chair, Sam Brunson, at sbrunson@luc.edu.

“Taxman” (Sam’s Version)

By Sam Brunson

Almost seven years ago(!), Leandra wrote about the Beatles’s “Taxman” to celebrate its 50th anniversary. At around the same time, I tried to figure out and record the song.

At the time, unfortunately, neither my playing nor my recording chops were up to the challenge. Over the pandemic, though, I spent some time and money on instruments and recording equipment and have gotten a lot better at it.

So about a week ago, I decided to record a version of “Taxman.” I listened around to various versions and ended up modeling my version largely on the recording by Bill Wyman’s Rythm Kings (and, to a lesser extent, Soulive).

Continue reading ““Taxman” (Sam’s Version)”Whistleblowers and Disinformation — Roundtable #2: The Public Sector

By Diane Ring

We are back again this week looking at the role of misinformation and disinformation in democracy, good governance, and well-grounded decisionmaking! On Friday, we are hosting the second Roundtable in the Whistling at the Fake research project (with Dr. Costantino Grasso as PI, and funded by NATO’s Public Diplomacy Division). In our first Roundtable, we focused on disinformation in the private sector.

This Friday February 25, 2022 at 10:00am EST, the subject is Disinformation and the Public Sector.

The Roundtable includes three sessions: (1) Democracy and Disinformation – the Political Level; (2) Disinformation and Public Administration; and (3) Special Issues and Final Recommendations. The international panel includes experts from law, media, government, and civil society, along with whistleblowers. To join this exciting Roundtable session, register here!

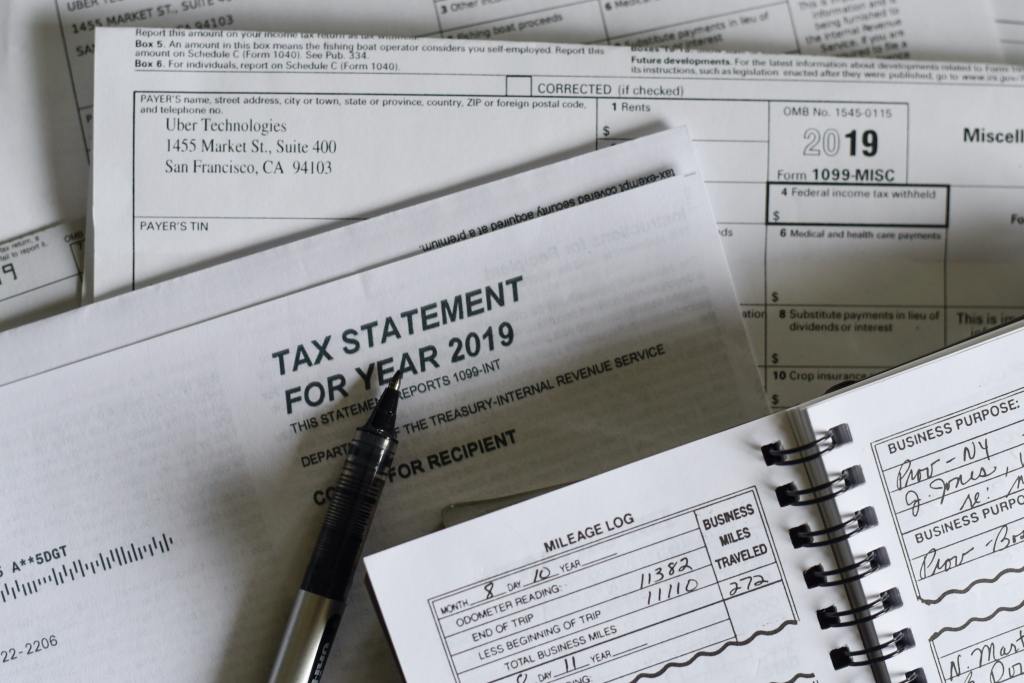

Taxing Venmo?!?

By Samuel D. Brunson

Over the last couple weeks, I’ve seen people in a couple very disparate groups worry about the 1099s they’re going to receive. (One group is saxophone enthusiasts who occasionally sell instruments and mouthpieces on eBay and Reverb.)

And why are they worried? Basically because the American Rescue Plan Act of 2021 makes it much more likely that they’ll receive 1099s, even for casual selling. Section 6050W of the Code requires companies like Paypal and Venmo (and other non-credit card payment processors) to report payments made, both to the payees and to the IRS.

Continue reading “Taxing Venmo?!?”Whistleblowers and Disinformation: “Whistling at the Fake” Roundtable

By Diane Ring

Information lies at the heart of a sound democracy, good governance, and well-grounded decision making, whether at the individual, community, business, or government level. Yet every day we see how misinformation and disinformation undermines all of these goals.

In response to this problem, a new research project, Whistling at the Fake (with Dr. Costantino Grasso as PI, and funded by NATO’s Public Diplomacy Division) aims to address the gap in the public’s understanding of the full scope and impact of misinformation and disinformation, and to empower the general public and regulators with tools, suggestions and recommendations for the future. The project focuses in particular on the role of whistleblowers and other informed insiders in “exposing misleading and hostile information activities and increasing public resistance to acts of this nature.”

As part of its project, Whistling at the Fake is hosting Roundtables on zoom– the first of which is this Friday, January 28, 2022 at 10:00am EST. The Roundtable, “Disinformation and the Private Sector” includes three sessions: (1) Exploring the Phenomenon, (2) Disinformation and Corporate Power and Wealth, and (3) Special Issues and Recommendations. The international panel includes experts from law, media, business, research, along with whistleblowers. To join what should be an amazing zoom Roundtable, register here!

Why Do Non-OECD, Non-G20 Countries Pursue International Tax Cooperation? Shu-Yi Oei Investigates in an Empirical Study of Membership in the BEPS Inclusive Framework

by Diane Ring

A dominant theme of international taxation over the past 15 years has been that of cooperation and consensus—from the BEPS Project to the new Multilateral Instrument to the new BEPS Inclusive Framework. Regardless of one’s assessment of nations’ true commitments to such cooperation and consensus, it is clear that notable changes in the framework of international tax engagement are afoot.

Yet, countries themselves remain very different in terms of the wealth, GDP, natural resources, tax revenues, commercial base, infrastructure, technological capacity, and financial systems. It is not obvious that cooperation and consensus are uniformly in countries’ interests, particularly in light of who is drafting the agenda. Most pointedly, it is reasonable to ask why non-OECD, non-G20 countries would be willing to commit to global tax cooperation.

In a new empirical paper, “World Tax Policy in the World Tax Polity? An Event History Analysis of OECD/G20 BEPS Inclusive Framework Membership,” Shu-Yi Oei tackles this question by studying the OECD/BEPS Inclusive Framework, which currently has a total of 140 member states, of which 96 are non-OECD, non-G20 countries. Using event history regression methods, Oei seeks to answer the question of how these states came to join the Inclusive Framework. She posits a series of hypotheses regarding membership drivers and tests them against a new database that she has constructed. In a paper that is accessible to both international tax policy makers and empiricists, Oei provides a compelling answer to the question. Not surprisingly, the actions and initiatives of international organizations and blocs play a the significant role in the story. In fact, many of the findings prove consistent with earlier work that Oei and I have written (both separately and together) including analyses of international relations dynamics in international tax, the scope of actors shaping international tax policy, the potential for disjuncture between international agreement and domestic action, the potential influence of nonstate actors, and the ability of powerful states to draw other nations into specific tax policy choices. Oei’s new empirical paper propels this research agenda forward by allowing greater insight into the world of international tax.

Season 2 of Break Into Tax

By: Leandra Lederman

By now, you may have seen one or more videos on the Break Into Tax YouTube channel (www.BreakIntoTax.com) that I started earlier this year with Allison Christians (McGill). We’ve created overview videos on tax policy, tax procedure, an array of income tax topics, legal writing, and more. We’ve done “Tax Papers Unlocked” micro-workshops on current tax scholarship. We’ve also released some #WhyTakeTax videos for students featuring a lot of tax profs, plus some tax humor videos. All Break Into Tax videos are intended to be entertaining, and most also are designed to be informative!

After about 30 videos, we wrapped up what we term “season 1.” It’s now time for season 2! We released a new intro video today, which you can find here. As mentioned there, I’ll be running this season. I’ve got some fun videos coming up, including more on income tax, more tax humor, a “crossover episode,” and something for folks interested in academia. Subscribe to the channel and turn on notifications if you don’t want to miss these as they come out!

If you’re a professor, I hope you’ll assign some of the Break Into Tax videos in lieu of a reading, for review, or as an optional resource! If you’re a student, I hope you find the explanations and illustrations helpful. Join us as you break into tax!

International Symposium: “The Professionals: Dealing with the Enablers of Economic Crime”

By Diane Ring

Just as summer is in full swing, the VIRTEU Project is back with a close look at a less than sunny side of economic life — the role that professionals (read lawyers, accountants and auditors) can play in enabling economic crime. This coming Wednesday July 21, 2021 (starting at 10:15am ET) join us in a three-panel zoom symposium that investigates how and why professionals may play this enabling role, and what responses and solutions we might consider. We will look carefully at real life case studies and talk with experts from various sectors as we explore this ongoing issue.

Register here to join us for this zoom symposium.

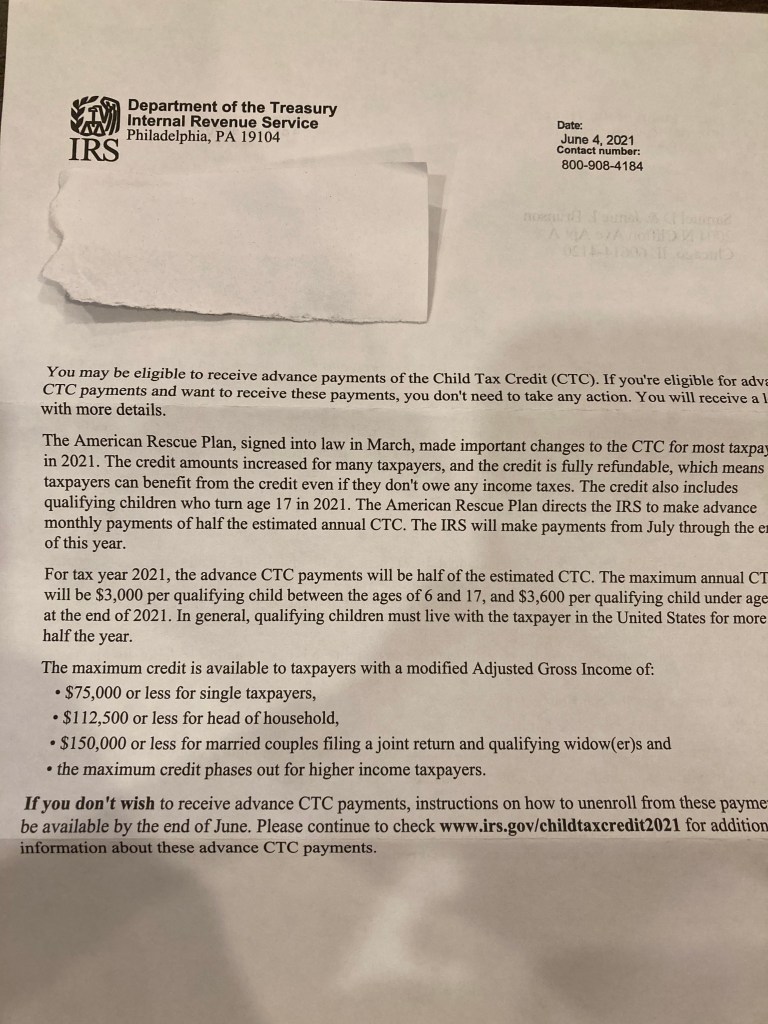

Advance Payments of the Child Tax Credit

By: Sam Brunson

Yesterday my neighbor texted me to mention that three pieces of my mail had been left in his mailbox; he dropped them off in front of my door. Two were just standard junk mail but one is potentially important: a letter from the Department of the Treasury.

Perhaps you also got this letter: it has some important information about the way the the child tax credit now works. In short, the American Rescue Plan, a law signed in March, makes a number of significant changes to the child tax credit.

Two of those changes are particularly notable. First, it increases the amount of the credit to $3,000 for most children and $3,600 for children five and younger.

Second, it makes allows the IRS to make advance payments of the child tax credit. Essentially, unless parents choose otherwise, starting in July the will receive monthly payments of $250 or $300 per child (depending on the child’s age).

Third, the credit is fully refundable. Even if a parent doesn’t have enough income to owe taxes, they will receive the full amount of the child tax credit.

Finally, the age limit for the child tax credit has been increased from 16 to 17. (Note that currently these changes are all temporary–they only apply to 2021, though the may be extended as some point.)

Continue reading “Advance Payments of the Child Tax Credit”Announcing the 2021 Indiana/Leeds Summer Tax Workshop Series!

By: Leandra Lederman

As I blogged previously, Dr. Leopoldo Parada from the University of Leeds School of Law and I (with the support of the Indiana University Maurer School of Law) will co-host the Indiana/Leeds Summer Tax Workshop Series again this summer. It will meet online via Zoom on Fridays from 11:30am-1pm Eastern Daylight Time (4:30-6pm British Summer Time). Last summer’s series went really well. If you are interested in cutting-edge tax issues, we hope you will consider attending!

We received numerous excellent submissions in response to this year’s Call for Papers. As stated there, we prioritized tax topics that would be of interest to scholars in multiple countries. Here is the list of speakers and the papers they’ll be presenting:

Like last year, the workshop will take place on Zoom, as a regular Zoom session. We will introduce the speaker, who will have about 20 minutes for scripted remarks, and the remainder of the time will be allocated to questions and discussion. Approximately a week in advance of each talk, we expect to share the draft paper online on the following website: law.indiana.edu/summer-tax.

The Indiana/Leeds Summer Tax Workshop Series is open to attendance by interested faculty, tax experts, and students. This summer, you will need to register in order to obtain the Zoom link and the password for any password-protected papers. Please register at TinyURL.com/INLeeds2021.

Students and other attendees who would like to list on their c.v. that they “participated in the 2021 Indiana/Leeds Summer Tax Workshop Series” should do the following:

- Attend at least 5 of the scheduled sessions.

- Type in the “chat” window of the Zoom session of each session you attend a brief introduction containing your name, school or other institution, location, and degree candidacy or job title.

We encourage all attendees to introduce themselves in the chat window, as well.

If you have questions, feel free to email us at llederma@indiana.edu and L.Parada@leeds.ac.uk. We hope to see you (virtually) this Friday and at the other sessions this summer!

Call for Papers for the 2021 Indiana/Leeds Summer Tax Workshop Series

By: Leandra Lederman

This summer, the Indiana University Maurer School of Law and the University of Leeds School of Law will run the Indiana/Leeds Summer Tax Workshop Series again. Like last summer, Dr. Leopoldo Parada and I will host it. It will meet online via Zoom on Fridays from 11:30am-1pm Eastern time (4:30-6pm British Summer Time), starting May 28, 2021. We expect to invite a couple of speakers and select the remainder from a call for papers.

The Call for Papers opens today and will close on May 14, 2021 at midnight British Summer Time (7pm Eastern Daylight Time). If you are interested in presenting in the Workshop, please send the following before then to both llederma@indiana.edu and L.Parada@leeds.ac.uk, with “Indiana/Leeds Workshop submission” in the subject line of your email:

- Your name, title, and affiliation.

- The paper title and an abstract of no more than 1,000 words.

- Whether or not you already have a draft of the paper. (We plan to circulate a draft of each paper—a minimum of 10 pages—a week in advance of each talk.)

- Whether or not the paper has been accepted for publication, and, if so, when it is expected to be published.

- A list of any Fridays between May 28 and July 16 that you would not be available to present, or a statement that any Friday in that date range would work for you.

In selecting papers, preference will be given to tax topics of broad, general interest. These can involve international or domestic tax issues, but a preference will be given to topics that would be of interest to scholars in more than one country. Like last summer, we expect an international group of attendees. Note also that speakers will be strongly encouraged to limit their scripted remarks to 20 minutes, to allow ample time for questions and discussion.

Videos of all but one of last summer’s talks are online at http://www.tinyurl.com/indianaleeds. These recordings include only the introductory remarks and the scripted portion of the speaker’s presentation. We plan to take the same approach this summer for those speakers who grant permission.

If you have questions, feel free to email us at L.Parada@leeds.ac.uk and llederma@indiana.edu.

Tax Return of the Jedi

By: Leandra Lederman

It started on Twitter with the following tweet from Prof. Musgrave:

I replied with what became my most popular tweet to date. (The bar was not high.)

As Twitter replied with funny comments, the idea quickly became fodder for Break Into Tax, the YouTube channel that Allison Christians and I launched last month. So, here it is: TAX RETURN OF THE JEDI: UNOFFICIAL PARODY TRAILER. Don’t miss the Circular 230 disclaimer at the end!

Institutional Corruption and Avoidance of Taxation: Final VIRTEU Roundtable

By Diane Ring

The most recent Roundtable session in the series of four VIRTEU [Vat fraud Interdisciplinary Research on Tax crimes in the European Union] sessions this spring focused on the limited success we have seen with the formal regimes of gatekeepers tasked with ensuring that taxpayers accurately meet their reporting and taxpaying obligations. The session then explored the role that whistleblowers play in remedying the resulting enforcement gaps. (A recording of this 3rd Roundtable is available here). Building on that discussion, the 4th and final Roundtable session, to be held Friday March 12, 2021 at 12:30pm EST (5:30pm GMT), will turn to the related topic, Institutional corruption and tax avoidance.

This March 12th discussion will examine corruption broadly understood to encompass not only the most direct forms of corruption (e.g. bribes) but more indirect forms (including implicit deals with officials), on to questions of undue influence, conflict of interest and the power of lobbying. Attention will be given to not only government actors, but also structural and institutional features that impact corruption and avoidance of taxation, including the role of large corporations, wealth, and power bases. For more information on the Roundtable, see below. To join us for the discussion, please register here.

Supervillainy and the U.S. Tax Code

By: Leandra Lederman

Recently, my resident D.C. comics fan, Nickolas Cole, asked me to watch with him Episode 3 of the animated Harley Quinn TV series, “So, You Need A Crew?”. (Warning: this show is not safe for work.) He thought I would enjoy the premise of the episode, which is that female supervillains face a glass ceiling. (You can’t make this stuff up. Well, actually, I suppose you can and someone did!)

I’m not much of a fan of cartoons but I thought the quirky humor was pretty well done. So, there I am watching Harley Quinn struggle to recruit a crew to work for her when all of a sudden, there’s the U.S. Master Tax Guide! And it has the voice of Wanda Sykes. The writers didn’t miss a trick. The intro to the tax stuff features the tax-preparation boutique “TAXES 4 FREE* *NOT 4 FREE,” seemingly ripped from the headlines. (That appears at 1:17 here, but if you don’t mind cursing cartoon characters, you may enjoy the whole three-minute segment, which captures a lot of the premise of the episode.)

Continue reading “Supervillainy and the U.S. Tax Code”VIRTEU Roundtable #3: Whistleblowing, Reporting, and Auditing in the area of taxation

by Diane Ring

We do not yet live in a world in which taxpayer compliance can simply be assumed. Instead, we must rely on the interplay of reporting requirements, internal and external auditing, and ultimately whistleblowing, to help ensure compliance with the tax system. How do they fit together? What can we expect from reporting and auditing? When do they breakdown, and why? How does whistleblowing–both the actual cases and the “threat” of whistleblowing–shape law, taxpayer behavior, and society’s understanding of compliance. And when does this tax noncompliance intersect with government corruption and fraud? What recommendations and options might we consider for the future?

Next week, the VIRTEU Roundtable Series tackles these questions in its 3rd Roundtable: “Whistleblowing, Reporting and Auditing in the area of taxation.” (VIRTEU [Vat fraud: Interdisciplinary Research on Tax crimes in the European Union]). This session builds on the first two Roundtables which gathered experts from around the world to discuss tax crime, corruption, CRS, and business ethics, and which can be viewed online: (1) Roundtable #1: Exploring the Interconnections between tax crimes and corruption; and (2) Rountable #2: CSR, Business Ethics, and Human Rights in the area of taxation.

The 3rd Roundtable, on “Whistleblowing, Reporting and Auditing in the area of taxation,” will be held Friday February 26, 2021 at 5:30-7:00pm GMT (12:30-2:00pm EST). For more information on the panel, see below. To join us, visit the registration link here.