The Tax Valentines poems on Twitter are always a highlight of the winter for me. Tax folks can be very creative weaving together romance and tax concepts! This year, there seemed to be fewer overall, but there still are plenty to be found if you search #TaxValentines on Twitter. Prof. Kathleen DeLaney Thomas even shared Tax Valentines her students wrote as a fundraiser for public interest grants for UNC Law students!

Here are a couple of new ones I didn’t get a chance to post on Twitter:

Last month, the VIRTEU Roundtable Series launched with a discussion I had the opportunity to moderate on the basic connections between tax crime and corruption. (VIRTEU [Vat fraud: Interdisciplinary Research on Tax crimes in the European Union]). Clearly, we were only just getting started — the discussion ended because time was up but the questions continued. This week’s roundtable takes a closer look at the role that CSR (corporate social responsibility), business ethics and human rights can, should, or do play in business conduct, in tax enforcement strategies, and in the design of tax law itself.

These three frames for regulating (business) behavior are regularly examined and debated in the corporate and regulatory literature, but their application to the tax system remains under explored. If you are interested in thinking more about the tax side, join us this Friday February 12, 2021 at 5:30-7pm GMT (12:30-2:00pm EST). For more information on the panel, see below. To join, visit the registration link here.

We’ve started a new YouTube series we wanted to share with our readers! It’s called “Break Into Tax” (BiT) and can be found at tinyurl.com/BreakIntoTax.

The idea behind BiT is that we’ll discuss and break down tax-related concepts, broadly defined. This includes issues that may be of interest to law students and others newer to tax or to particular issues. The topics we plan to cover include substantive tax law concepts, tax policy concerns, the study of taxation, and the pursuit of tax as a career. We also welcome suggestions for topics in the comments on our videos!

We come at the issues from the perspective of tax law professors in the U.S. and Canada with cross-border interests. The BiT series is not at all designed to be of interest only to people from these two countries. We expect to focus on concepts that are foundational enough or general enough to be of broad interest.

Our introduction video, located here, is a good place to start. It shares more about us and the BiT channel. Our first playlist covers Tax Policy Colloquia: what are they, how to ask a good question in a tax workshop, and tips for students writing reaction papers.

It is no surprise to those working in the tax field, whether in government, private practice, academia or the nonprofit sector, that not all taxpayer mistakes are innocent. Some taxpayers affirmatively engage in fraud, and sometimes that fraud is wrapped up with corruption. The high profile spate of tax leaks beginning in 2008 helped put a more public face on many aspects of an old problem.

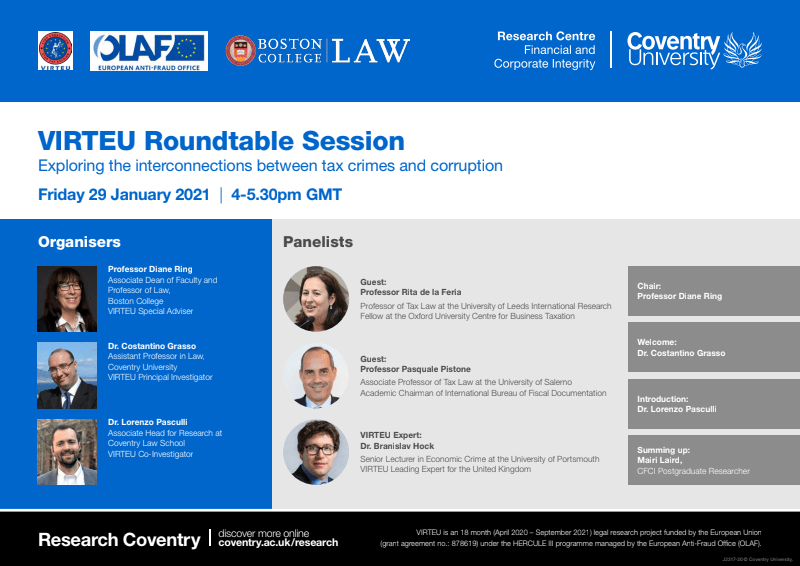

As part of an effort to better respond to tax crimes and corruption, the EU has funded an interdisciplinary and comparative research legal research project — VIRTEU [Vat fraud: Interdisciplinary Research on Tax crimes in the European Union]. This project is aimed at exploring connections between tax fraud and corruption. Focused in part on VAT fraud, the relevant issues and the kinds of questions that must be asked are universal across the tax system.

VIRTEU, for which I am a special advisor, is hosting a Roundtable Discussion Series this spring that brings together experts from academic institutions, nongovernmental organizations, and the private sector to engage in topical discussions around the general problem of tax fraud and corruption. Along with the the VIRTEU project’s Principal Investigator Dr. Costantino Grasso and Co-Investigator Dr. Lorenzo Pasculli, I will be organizing and hosting the series, which is also sponsored by Boston College Law School, Coventry University Research Centre on Financial and Corporate Integrity, and OLAF (the European Anti-Fraud Office).

The first session, “Exploring the interconnections between tax crimes and corruptions“, will be held via Zoom on Friday January 29, 2021 (at 11:00am EST/ 4:00pm GMT). Here is the registration link. See below for more details – and join us for what promises to be an invigorating discussion of the connections between the legal and policy frameworks for corruption and for tax crimes.

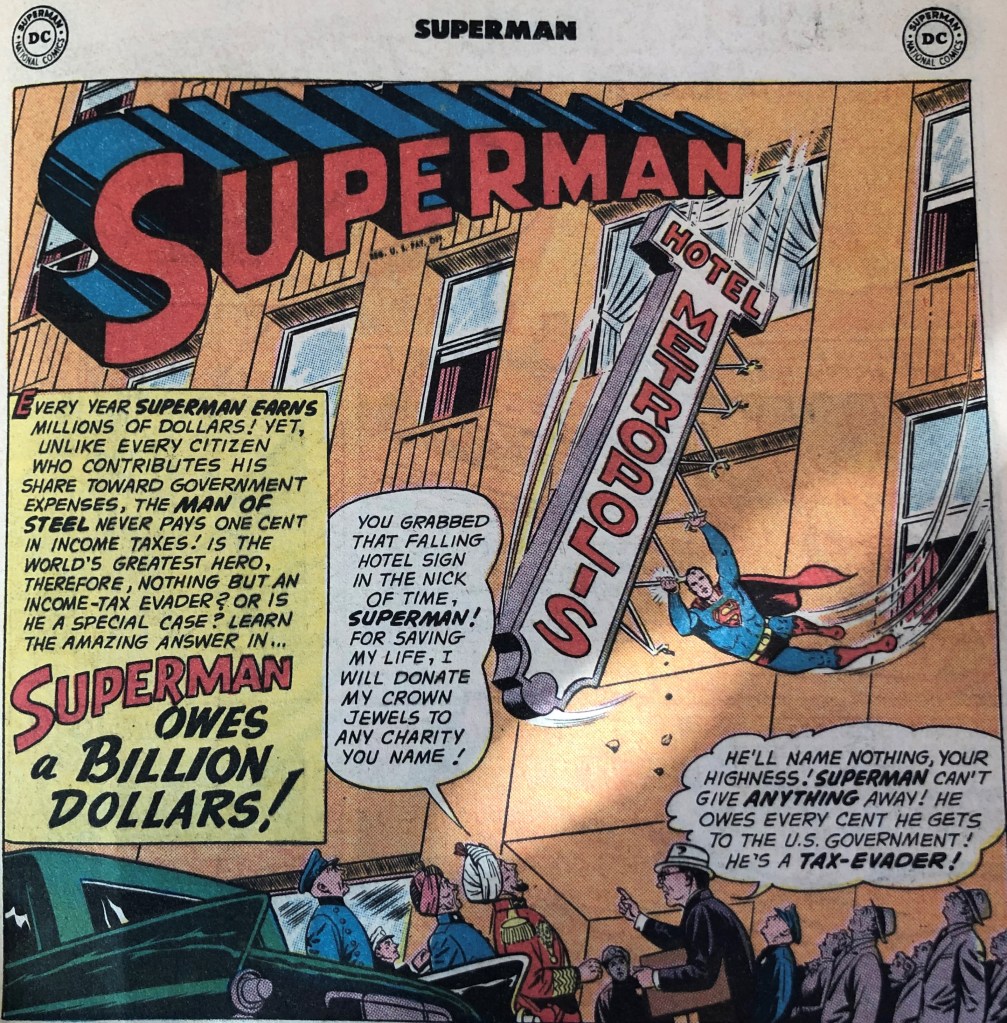

Nick, who’s been a Superman fan since childhood, got me the Oct. 1961 issue of the Superman comic for Christmas. It’s got a story in it billed as “Superman Owes a Billion Dollars” in taxes! Here’s the splash panel:

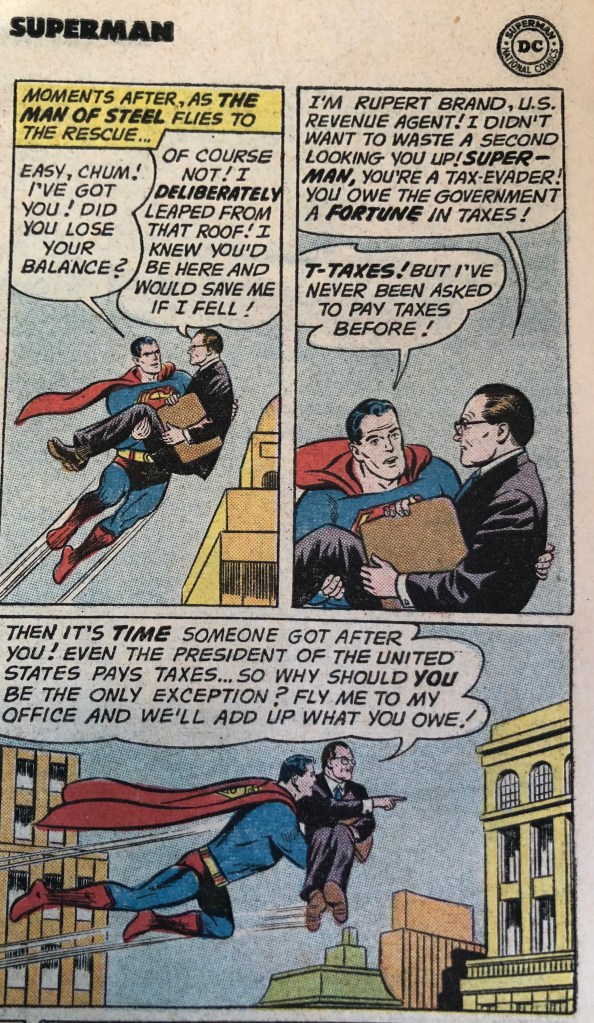

The basic premise is that a new Revenue Agent “at the Internal Revenue Bureau in Metropolis,” Rupert Brand,* discovers “no record that Superman has ever paid taxes!” (In case you’re wondering, nope, the IRS was not called the “Internal Revenue Bureau” back then. In 1953, it changed its name from the “Bureau of Internal Revenue” to the “Internal Revenue Service.” Perhaps a clue that not to rely on any of the tax statements in the story!)

Brand figures out the quickest way to reach Superman about this apparent delinquency, and explains that even the President of the United States pays taxes (cf.these blog posts), and so must Superman!

Why does Superman owe tax? Well, the story explains that “each year, Superman captures countless criminals, collecting a fortune in reward money!” And not just that, “whenever he digs up buried treasure” [treasure trove, anyone?] “or squeezes coal into diamonds, he earns more untold millions! All that wealth is income!”

One of the key components of the CARES Act was the Paycheck Protection Program, a $500 billion lifeline to American businesses dealing with the effects of the COVID-19 pandemic and the resulting public health measures that slowed commerce across the country. Like any significant financial program, the PPP came with tax questions. The program provided participants with loans rather than grants, but those loans would be forgiven if taxpayers complied with the conditions of that program. Normally, loan forgiveness results in income to the beneficiary, but Congress provided an exemption for those amounts under the PPP. Taxpayers would therefore get to keep their entire grants if they complied with the conditions of the program. Or so many thought.

On November 5—two days after the presidential election—James O’Keefe posted an interview with a postal worker claiming that he and his colleagues were instructed to backdate ballots that they received after election day. The next day he filed an affidavit swearing that he and his colleagues had been instructed to continue picking up ballots after the November 3 deadline.

After an interview with U.S. Postal Service investigators, Richard Hopkins, the postal worker, recanted his statements. He also told investigators that his affidavit had been written by Project Veritas, the organization O’Keefe founded and with which he is associated.

Project Veritas, it turns out, is a tax-exemption organization. And its association with Hopkins may have put its exemption at risk. By signing an untrue affidavit, Hopkins almost certainly broke the law. And several attorneys interview in the Salon story say that Project Veritas may also have broken the law as a result of its involvement in the false affidavit.

Tax losses pose a special problem for the federal fisc. I’ll get to that in a minute, but first some set-up as to how tax noncompliance differs on the income side versus the deduction and credit side. The overall purposes of this post are to address some questions I’ve gotten and pull together some tax enforcement themes that are implicated by the recent NY Times reporting on Pres. Trump’s returns.

The Importance of Third-Party Reporting

A lot of tax noncompliance occurs with respect to income. Not for folks with mainly wage and salary income who maybe earn a little bit of interest from a bank account. All of that is reported by third parties (the payors) to the IRS, on information returns like Form W-2 or Form 1099. The taxpayer/payee receives a copy the information return and that both simplifies reporting and communicates what information the IRS has about the transaction. As Joe Dugan and I argue in a forthcoming article, third-party reporting is very effective. With the IRS able to do simple return matching to catch any incorrect reporting (intentional or otherwise), IRS figures like this bar graph show that there’s not a lot of noncompliance where there’s substantial third-party information reporting.

Where much tax noncompliance occurs is with respect to income earned by the self-employed and small businesses, where there’s much less third-party reporting and also more use of untraceable cash. (I added the red circle to the IRS image below.)

I was inspired last night while watching the debate to write some limericks about President Trump’s tax returns. I’m sharing them here to collecting them in one place. It would be great to see others add to the collection, too–there may not be as much love as on #TaxValentines Day–but #TaxLimericks could be a broader genre!

There once a crass “billionaire“ Who spent 70K on his hair He attacks with his tweets But the Times got receipts And the profits just aren’t there #TrumpTaxes#TaxLimericks

For the last several months, I’ve been meeting a guitarist and sometimes other musicians at a Chicago park to play outdoor socially-distanced jazz. This Sunday, driving home, my wife asked me if we knew what Trump had paid in taxes. “Of course not,” I confidently responded. “It looks like we do now,” she said.

And with that, my work goals for this week changed. I’m sure everybody reading this has seen Sunday’s New York Times story (and probably also its follow-up from yesterday). Along with a ton of other tax people, I’ve been trying to make sense of and contextualize the story, both to myself and to the public. And I’ve largely been doing my thinking in real-time on Twitter.[fn1]

I thought that I’d assemble a lot of those Twitter threads here into one place. At most I’ll lightly edit them and I’ll link to the actual threads on Twitter, too. Because over there I included GIFs on almost every tweet and I think I outdid myself. The relevant content will be here, though. Continue reading “#TrumpTaxReturns”→

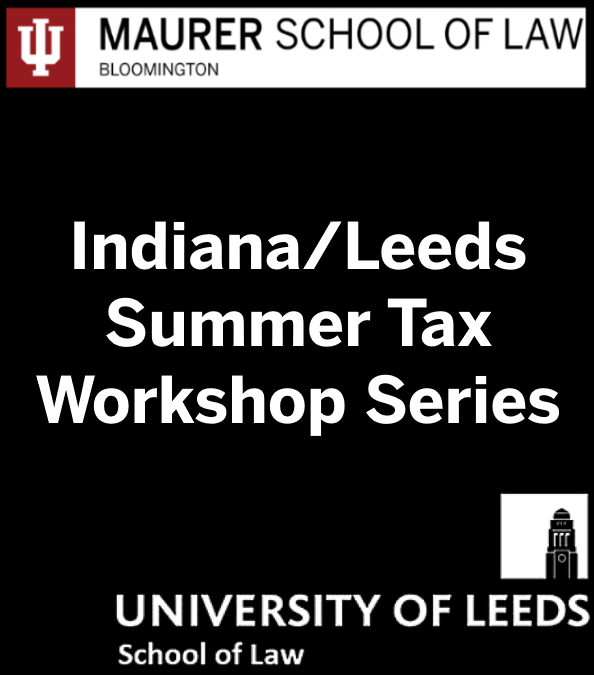

The 2020 Indiana/Leeds Summer Tax Workshop Series ended on Thursday, after 13 weeks of talks. It was terrific getting to spend the summer with so many tax enthusiasts–professors, practitioners, and students–from all over the world! Dr. Leopoldo Parada and I really enjoyed co-hosting this series, and we expect to continue it next summer!

We received speaker permission to share videos of most of the talks. The speaker’s scripted remarks and our introductions are included. Those videos can be found at this link.

The complete speaker list and papers presented were as follows:

May 21

Ruth Mason, University of Virginia

The Transformation of International Tax

May 28

Stephen Daly, King’s College London

Trust, Tax Administration and State Aid

June 4

Susan Morse, University of Texas

Modern Custom in Tax

June 11

James Repetti, Boston College

The Appropriate Roles for Equity and Efficiency in a Progressive Income Tax

June 18

Diane Ring & Shuyi Oei, Boston College

Regulating in Pandemic: Evaluating Economic and Financial Policy Responses to the Coronavirus Crisis

June 25

Umut Turksen, Coventry University

The Role of Human Factors in Tax Compliance and Countering Tax Crimes

July 2

Allison Christians, McGill University

Accurately Counting Value in the International Tax System

July 9

Joshua Blank, University of California, Irvine

Automated Legal Guidance

July 16

Michael Devereux, University of Oxford

The OECD GloBE Proposal

July 23

Ana Paula Dourado, University of Lisbon

The Concept of Digital Economy for Tax Purposes: a Reassessment

July 30

Ricardo García Antón, Tilburg University

Enhancing the Group Interest in Transfer Pricing Analysis

Aug. 6

Steven Dean, New York University

A Constitutional Moment in Cross-Border Taxation

Aug. 13

Monica Victor, University of Florida

The Taxman’s Guide to the Galaxy: Allocating Taxing Rights in the Space-based Economy

Thank you again to all those who joined us, and we hope to see you next year! #IndianaLeedsSummerTax

On Tuesday the Supreme Court issued its opinion in Espinoza, holding that Montana couldn’t prohibit “student scholarship organizations” from making tuition payments to religiously-affiliated private schools. I wrote about the decision over on the Nonprofit Law Prof Blog.

After writing the post, I saw this entry in a SCOTUSblog symposium on the Espinoza decision. And, like the authors of that piece, I found the Supreme Court’s decision unsurprising (for reasons that I mention on the other blog). But one part of their analysis jumped out at me as reflecting a critical misunderstanding of the way Montana’s tax credit scheme worked.

Specifically, the authors wrote:

The secular instruction in these schools means that the state gets full secular value for its money. There are complications in putting a dollar amount on this secular value. It might be the schools’ full cost, given that they satisfy compulsory-education requirements. Or some of the cost might be attributed to teaching religion. But one thing we know: the secular value is far more than zero. A $2,250 tuition voucher (the amount involved in the court’s 2002 decision in Zelman v. Simmons-Harris) can easily be allocated entirely to secular value. All the more so in Espinoza, where the tax credit was capped at $150.

(Emphasis mine.)

This paragraph isn’t critical to the blog post; it’s not mentioned in the majority’s analysis. And yet I’m afraid it may have been in the back of the mind of the Justices. Because, after all, what’s $150 out of private school tuition? Continue reading “How the Espinoza Tax Credits Work”→

Susan Morse and Stephen Shay have blogged on Procedurally Taxing on both May 22 and June 11 on Altera’s efforts to have the U.S. Supreme Court grant certiorari in Altera v. Commissioner. Altera is a closely followed case involving an administrative law challenge to the validity of a Treasury regulation, so I wanted to flag those blog posts for Surly Subgroup readers.

Recall that in Altera, the Court of Appeals for the Ninth Circuit upheld a cost-sharing regulation under IRC § 482, reversing the Tax Court’s unanimous decision invalidating the regulation as arbitrary and capricious. The Ninth Circuit ruled 2-1 for the government in both its original opinion, which was withdrawn due to the death of one of the judges on the panel, and again in a revised opinion. The Ninth Circuit also denied rehearing en banc, a victory for the IRS’s rulemaking process. (Full disclosure: in addition to joining in two earlier amicus briefs in favor of the Commissioner, which Susie and Steve spearheaded, I co-authored with them and Clint Wallace a 2019 amicus Brief in Opposition to the Petition for Rehearing En Banc.)

As I posted previously, this summer, Dr. Leopoldo Parada from the University of Leeds School of Law and I (with the support of the Indiana University Maurer School of Law) will co-host the new Indiana/Leeds Summer Tax Workshop Series. It will meet online via Zoom on Thursdays from 10:30am-noon Eastern time (3:30-5pm British Summer Time). If you are interested in cutting-edge tax issues, we hope you will consider attending!

We received many terrific submissions in response to the Call for Papers. As stated there, we prioritized tax topics that would be of interest to scholars in multiple countries. We are very fortunate to have Professor Ruth Mason from the University of Virginia kicking off what promises to be an outstanding series! The following is the full list of speakers and the papers they’ll be presenting: Continue reading “Announcing the 2020 Indiana/Leeds Summer Tax Workshop Series!”→

COVID-19 has impacted society in nearly every dimension, and state and local governments have been hit especially hard. Those governments are simply not equipped to deal with major revenue shocks like those that accompany a global pandemic. In that vein, a group of scholars has joined forces to create Project SAFE (State Actions in Fiscal Emergencies), which is focused on providing research-backed policy recommendations for states. Among the project’s areas of focus is how states can help themselves by modifying their own taxing and spending programs and priorities.

By:

By:

{kind=link}