By: Leandra Lederman

Tax losses pose a special problem for the federal fisc. I’ll get to that in a minute, but first some set-up as to how tax noncompliance differs on the income side versus the deduction and credit side. The overall purposes of this post are to address some questions I’ve gotten and pull together some tax enforcement themes that are implicated by the recent NY Times reporting on Pres. Trump’s returns.

The Importance of Third-Party Reporting

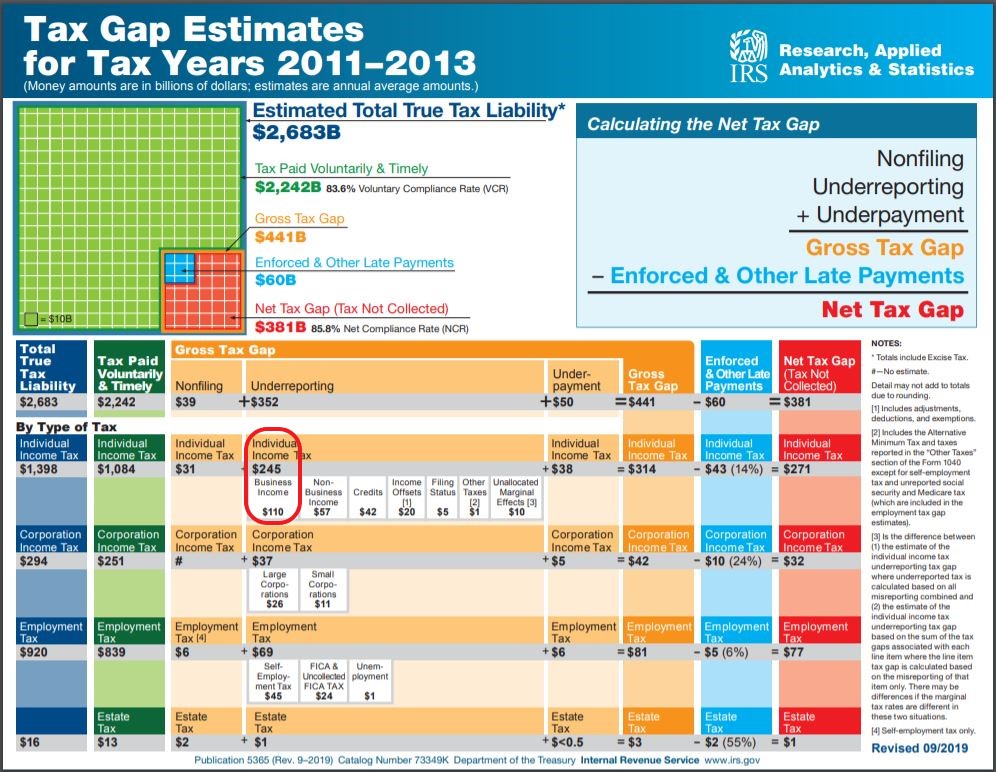

A lot of tax noncompliance occurs with respect to income. Not for folks with mainly wage and salary income who maybe earn a little bit of interest from a bank account. All of that is reported by third parties (the payors) to the IRS, on information returns like Form W-2 or Form 1099. The taxpayer/payee receives a copy the information return and that both simplifies reporting and communicates what information the IRS has about the transaction. As Joe Dugan and I argue in a forthcoming article, third-party reporting is very effective. With the IRS able to do simple return matching to catch any incorrect reporting (intentional or otherwise), IRS figures like this bar graph show that there’s not a lot of noncompliance where there’s substantial third-party information reporting.

Where much tax noncompliance occurs is with respect to income earned by the self-employed and small businesses, where there’s much less third-party reporting and also more use of untraceable cash. (I added the red circle to the IRS image below.)

The income side is also a major concern because to cheat on an item of income, like a cash payment received for a service by a business, the taxpayer generally can just fail to report it. It’s invisible to the IRS without an audit, in the absence of third-party reporting. On the other hand, to claim a deduction or credit, the taxpayer has to affirmatively include something on the tax return. The IRS at least has some notice on the return that the taxpayer is reducing the tax bottom line with the claim.

Income vs. Deductions and Credits in the Statute of Limitations Rules

These differences in visibility are reflected in the statute of limitations rules. The general rule, in IRC § 6501(a), is that the IRS has 3 years from when the tax return was filed to assess taxes. If no return is filed, the statute doesn’t start running, letting the IRS wait until it has a return to examine. If the IRS can show fraud, the limitations period is unlimited. But most relevant here, in the case of a “substantial omission” from gross income, as defined in IRC § 6501(e), the limitations period is doubled to six years. The longer period for the IRS to act reflects the importance of large omissions, but it also is only on the income side, not the deduction/credit side. The U.S. Supreme Court pointed out in the 1958 Colony, Inc. case that “because of a taxpayer’s omission to report some taxable item, the Commissioner is at a special disadvantage in detecting errors. In such instances, the return, on its face, provides no clue to the existence of the omitted item.”

Why Losses Matter So Much

The TL;DR summary of the above is that omitting income that’s not reported to the IRS by the payor may be harder for the IRS to catch than an inflated deduction. But here’s the thing about omitted income: the omission only saves tax on that income, it doesn’t reduce taxes on the rest of your income. So, if you win $1,000 in a neighborhood poker game and you don’t report it and are not caught, you’ll save the tax on that $1,000 of income. But if you have income from another source, like wages, you’re not reducing the tax liability on those wages. On the other hand, if you claim a $1,000 deduction that isn’t subject to disallowance or limitation, you eliminate the income tax on $1,000 of income, such as from your salary.

Some deductions, though potentially very generous, such as depreciation, are allowed by Congress and are entirely legitimate to claim, where they apply. But deductions and credits may of course be inappropriately inflated by the taxpayer. One area that risks this is where a non-cash item has to be “valued” for tax purposes. An example is a contribution to a charity of non-cash property that is inflated in order to claim a larger charitable deduction. According to the New York Times reporting, it appears that Pres. Trump claimed a $21.1 million charitable deduction for a conservation easement on the Seven Springs estate. The magnitude of that deduction depends in large part on valuations of the property with and without the easement. Valuation is notoriously subject to abuses in the absence of a thick market providing arm’s-length values. (I am currently writing an essay on tax valuation.)

It also appears from NY Times reporting that Pres. Trump reportedly claimed an abandonment loss on his Atlantic City casinos, producing a large deduction. The Times article raised the question of whether the abandonment loss rules actually are met. IRS Publication 544 explains that “[a] loss from an abandonment of business or investment property that is not treated as a sale or exchange generally is an ordinary loss.” By contrast, a sale or exchange of a “capital asset” at a loss is treated as a capital loss. The deductibility of an individual’s capital losses is limited to capital gains plus $3,000 of ordinary income per year. (Individuals’ excess capital losses can be carried forward but not back.) So, an important issue here appears to be whether Pres. Trump truly abandoned the property or if the transaction was instead a “sale or exchange” of property.

Large deductions, such as claimed losses, can be used to greatly reduce or “zero out” the tax liability on income items (such as income earned from “The Apprentice”). If taxes were prepaid, such as through withholding or estimated tax, such a claim could produce a tax refund for the year. That’s expensive for the fisc.

Moreover, because the annual periods the federal income tax system generally uses are somewhat artificial, particularly compared to an ongoing business, the federal income tax law, in IRC § 172, allows “net operating losses” to be carried to other tax years. Thus, for example, losses that the tax code permits to be carried back to previous tax years can produce a tax refund for those past years. That can get really expensive for the fisc. And, based on New York Times reporting, claimed net operating losses appear to be how Pres. Trump claimed a $72.9 million tax refund (according to this NY Times article, “all the federal income tax he had paid for 2005 through 2008, plus interest”).

The use of large loss deductions to offset unrelated income is not a new issue. Large, artificial loss deductions have been a staple of abusive tax shelters, both for individuals (especially in the 1970s and 1980s) and for corporations (especially in the 1990s). Congress, the Treasury, the IRS, have successfully battled abusive deductions on multiple lines, including in the courts. I have written about aspects of these issues in two articles, A Tisket, A Tasket: Basketing and Corporate Tax Shelters, 88 Wash. U. L. Rev. 557 (2011) and W(h)ither Economic Substance?, 95 Iowa L. Rev. 389 (2010). But it is worth noting that the reality that tax losses can be used to offset unrelated income (in the absence of a “schedular” system that “baskets” related items and caps deductions based on income from that source) are costly to the fisc and manifest themselves in a variety of contexts.

#FundTheIRS

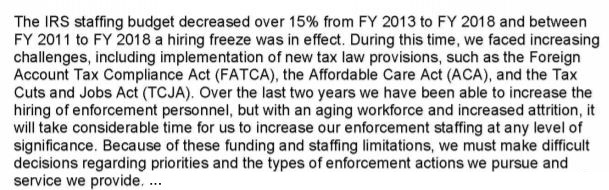

For the IRS to do its part to clamp down on tax abuse, it needs adequate funding. Studies show that audits have a hugely positive effect on tax compliance. It’s not just the direct receipts that enforcement brings in. Much more of it is the indirect effect that enforcement has on voluntary compliance. Congress has slashed IRS funding starting in 2011, while also added to the IRS’s responsibilities. Not surprisingly, audits as well as service have declined significantly. In order to curtail tax abuses, such as deducting inflated or artificial funding, Congress needs to return the IRS to at least the 2010 funding level, as adjusted for inflation. On Wednesday, the Treasury Inspector General for Tax Administration (TIGTA) released a report (unrelated to the Trump returns) titled “Individual Returns With Large Business Losses and No Income Pose Significant Compliance Risk.” Part of the IRS’s response to TIGTA (on page 19) was the following:

Basically, the IRS has been forced to make tough decisions about priorities due in part to significant cuts to its staffing budget. It’s not surprising that even before the NY Times story on Pres. Trump’s returns, many of us have been calling for Congress to adequately #FundTheIRS.