On February 1, Amazon Prime Video started streaming Blues Brothers. Now, in spite of its being one of the great movies of the 20th century, and having one of the greatest soundtracks ever, I hadn’t seen it in years, and definitely not since I moved to Chicago. So I decided to watch it, both because I love the movie and because I wanted to see its view of Chicago now that I know this city.

I remembered that the plot revolved around Jake and Elwood trying to raise $5,000 for the orphanage they grew up in or the orphanage will be closed, but I’d forgotten that the $5,000 was to pay the orphanage’s property tax assessment:

I’d also never watched a movie with Amazon’s X-Ray feature before. And X-Ray announced that the motivation for their mission from God is a factual error, because Illinois doesn’t tax church property.

On April 5, Indiana University Maurer School of Law’s Tax Policy Colloquium welcomed Andrew Hayashi from the University of Virginia School of Law. Andrew presented his fascinating new paper, “Countercyclical Tax Bases.” (The paper isn’t publicly available yet, but Andrew offered to share it by email with interested readers.)

The paper argues that the choice of tax base should take into account what tax base is most helpful to the economy in recessions. It points out that recessions are not rare; between 1980 and 2010, there were 5 recessions, covering 16% of that period. The paper does two main things. First, it provides interesting stylized examples showing how, following an economic shock that reduces income or housing value, three types of tax bases (income, sales, and property) each interact with household credit constraints and adjustment costs (committed consumption of housing) to either stabilize or aggravate the negative economic shock. These examples illustrate quantitatively how different tax bases can affect taxpayer behavior in a recession, and thus the local economy.

Second, the paper contains an original empirical study of county tax bases for 2007-2014, to see the effect of tax bases on the recessions of 2001 and the Great Recession of 2008-2009. Andrew combined data from the Government Finance Database, Zillow, the FBI’s Uniform Crime Reports, and the IRS’s Statistics of Income, among other places. Although the results for the two recessions were not identical, Andrew generally found in his OLS regressions that counties that relied more on property taxes had smaller increases in unemployment during the two recessions and may have recovered from the recession more quickly. Sales taxes generally had countercyclical effects, as well, particularly in stabilizing government revenues during the Great Recession. In general, counties that were most reliant on income taxes suffered the most in the two recessions (though the results for income taxes generally were not statistically significant). Continue reading “IU Tax Policy Colloquium: Hayashi, “Countercyclical Tax Bases””→

I grew up in the north suburbs of San Diego and, while I haven’t lived in Southern California in a couple decades now, I try to keep a vestigial self-identification as a Southern Californian.[fn1] Part of that self-identification is listening to the Voice of San Diego podcast; it keeps me vaguely up-to-date on current politics in San Diego.

This question gets more complex by the day. On Dec. 27, the IRS issued Announcement 2017-210, which can be found on their website. https://www.irs.gov/newsroom/irs-advisory-prepaid-real-property-taxes-may-be-deductible-in-2017-if-assessed-and-paid-in-2017 My first reaction to this was, good for the IRS for doing their job to provide guidance to taxpayers. But there is a caveat. The job of the IRS is not easy because it is subject to political constraints (the acting IRS Commissioner, David Kautter, also serves as Assistant Treasury Secretary for Tax Policy). It is unusual for the Assistant Secretary to also serve as acting IRS Commissioner – indeed this has never happened before, at least in recent memory – and it raises questions precisely about issues like the one about the state and local deduction – does the IRS announcement reflect a nonpolitical view or is it designed to serve the political purposes of the Trump administration?).

Those who are not aficionados of IRS documents may not focus on the fact that the IRS Announcement is not a Revenue Ruling, which would carry some legal status. An Announcement generally does not break new legal ground. The Accouncement states: “ A prepayment of anticipated real property taxes that have not been assessed prior to 2018 are not deductible in 2017.” (this is also ungrammatical, by the way). One would expect an Announcement that states a legal conclusion to provide a citation with legal authority, but the Announcement does not do so.

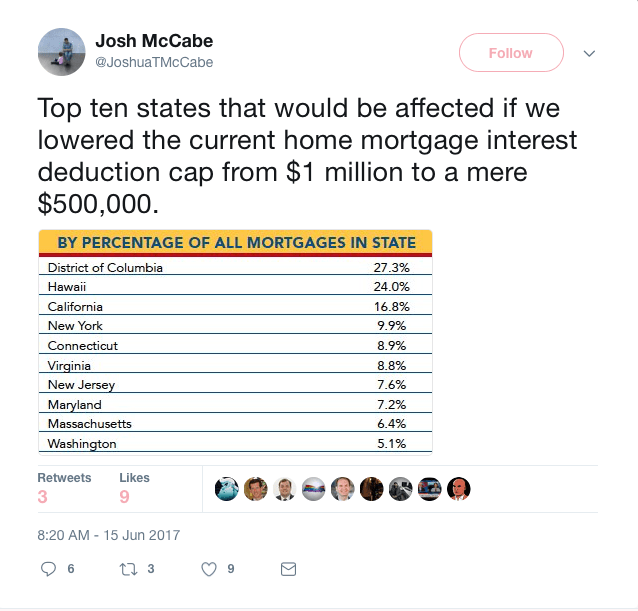

The Trump and Republican tax plans have circled around the idea of repealing the mortgage interest deduction. Although I’m not convinced it will happen (see e.g., Treasury Secretary Mnuchin’s remarks). The mere threat of the repeal has garnered a fair amount of attention.

For example, the other day this chart was making its rounds on twitter.

I have not verified the methodology of the chart or the data. I interpret that the chart examines (in absolute numbers) how many mortgages exist at $1,000,000. The implicit conclusion of the chart is that homeowners in states like D.C., Hawai’i, California and New York have the most at stake in retaining the deduction.

Why?

Because there seems to be evidence that the mortgage interest deduction contributes to housing inflation. Back in 2011 the Senate held hearings on incentives for homeownership. [1] It has been suggested that the elimination of the deduction will drop home prices between 2 and 13% with significant regional differences. [2] So, if the mortgage interest deduction is eliminated, then the aforementioned states might have numerous problems, including a smaller property tax base.

I was listening to “The Morning Shift” on WBEZ this morning, and they started talking about property tax. Now, property tax isn’t really my thing, but the story caught my ear for a couple reasons.