By: Leandra Lederman, with thanks to my in-house comics expert, Nickolas Cole

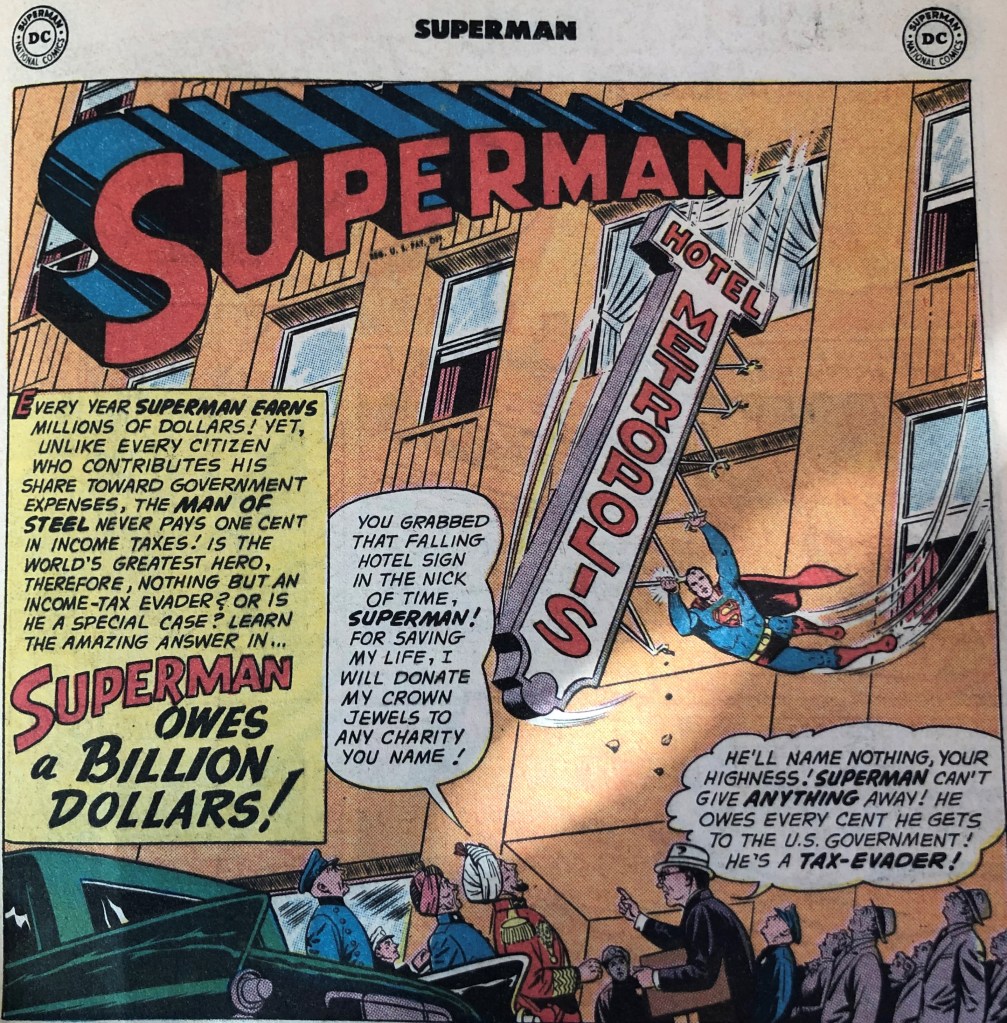

Nick, who’s been a Superman fan since childhood, got me the Oct. 1961 issue of the Superman comic for Christmas. It’s got a story in it billed as “Superman Owes a Billion Dollars” in taxes! Here’s the splash panel:

The basic premise is that a new Revenue Agent “at the Internal Revenue Bureau in Metropolis,” Rupert Brand,* discovers “no record that Superman has ever paid taxes!” (In case you’re wondering, nope, the IRS was not called the “Internal Revenue Bureau” back then. In 1953, it changed its name from the “Bureau of Internal Revenue” to the “Internal Revenue Service.” Perhaps a clue that not to rely on any of the tax statements in the story!)

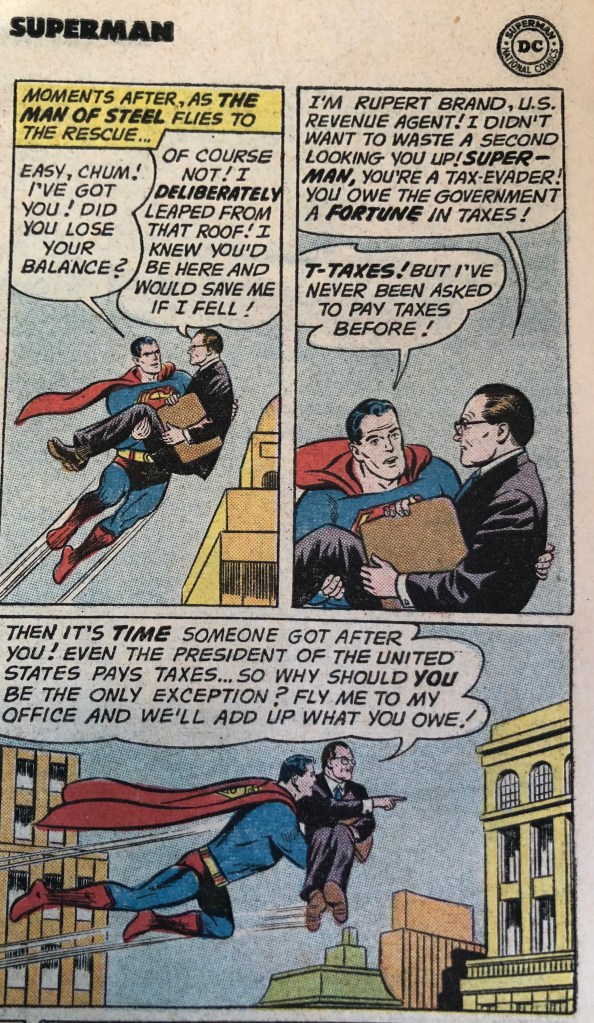

Brand figures out the quickest way to reach Superman about this apparent delinquency, and explains that even the President of the United States pays taxes (cf. these blog posts), and so must Superman!

Why does Superman owe tax? Well, the story explains that “each year, Superman captures countless criminals, collecting a fortune in reward money!” And not just that, “whenever he digs up buried treasure” [treasure trove, anyone?] “or squeezes coal into diamonds, he earns more untold millions! All that wealth is income!”

Continue reading “Superman, Tax Evader?”

By:

By: