By Sam Brunson

On Wednesday, I posted about how tax law played a central role in the college admissions scandal. As I’ve read through a little more of the affidavit, I decided to highlight two additional detail in this whole scandal, details that suggest that, for at least some of the participants, the tax consequences were very important.

Bruce Isackson and Facebook Stock

Bruce Isackson is the president of WP Investments, a real estate investment and development fund.[fn1] According to the affidavit, he used the fake athlete thing (soccer for the older daughter, rowing for the younger) to get two daughters into USC. He seems to have also paid for his younger daughter to get a better ACT score.

What’s interesting for purposes of this post is how he paid.

For both daughters, he made a significant portion of his payment with Facebook stock:

Why pay with Facebook stock? Well, it looks like Mr. Isackson was tremendously tax-sensitive. In fact, on one phone call with Singer, he confirmed that he would get a letter saying he’d received no goods or services in exchange for his donation so that he could substantiate his tax deduction.

So why would he pay with Facebook stock? Because making a charitable contribution with appreciated property provides a double benefit. The first is, the donor can deduct the fair market value of the property (here, $251,249 and $249,420). The second? It allowed Isackson to not pay taxes on his stock’s appreciation.

What do I mean? Well, we don’t know how much he paid for his Facebook stock. I don’t know how much he paid for his stock, but let’s say he bought it in January 2015, when it cost about $78 per share. If that’s the case (and again, I don’t know when he bought it), he would have a basis of $167,700 in the 2,150 shares he gave KWF in 2016. If he were to sell those shares on July 15, 2016, he would have realized a long-term capital gain of $83,549. And, assuming he was in the highest tax bracket, he would have owed almost $20,000 of taxes on that amount.[fn2]

Assuming Isackson paid taxes in the highest tax bracket (39.6% at the time), his putative charitable contribution would have reduced his tax bill by almost $100,000. That $100,000 reduction in taxes would have occurred whether he paid in cash or property. But by paying in appreciated property, he was able to avoid realizing gain (and, again, I’m making up the amount of gain he avoided: if he bought his Facebook stock earlier, there was probably more built-in gain), saving himself another $20,000 or more in taxes he may have owed.

Paying Through Your Private Foundation?

The you have Elisabeth Kimmel. Kimmel is the owner and president of Midwest Television, Inc., which, about a year ago, sold two San Diego television stations and two radio stations for $325 million. According to the affidavit, she bribed her daughter’s way into Georgetown as a fake tennis player, and her son’s way into USC as a fake track recruit.

But she didn’t pay (her own) cash. And she didn’t pay in Facebook stock. Instead, she paid through the Meyer Charitable Foundation:

Guidestar‘s Form 990s for MCF only go back to 2016, so I can’t look at its donations for the years in question. According to its 2018 Form 990, though, Kimmel served as the assistant secretary of the foundation (and I assume that Gregory Kimmel, the vice president, was her spouse).

Now, using a private foundation to make fraudulent bribes has the same problems as the other bribes, but using a private foundation also creates additional problems. In brief, private foundations are tax-exempt organizations that don’t actively do charitable things, and that receive the bulk of their revenue from insiders, not from the public at large. For various reasons, they’re regulated more closely than public charities, and have to comply with a number of additional rules. Violating those rules exposes both the foundation and its managers to various excise taxes. What excise taxes might the Meyer Charitable Foundation face?

Notably, I think the payment would qualify as an act of self-dealing. It involved the foundation paying a legal obligation of one of the managers. If that’s true, there are two initial excise taxes. The foundation owes an excise tax of 10% of the amount implicated in the self-dealing (here, 10% of the $275,000 is $27,500). In addition, any manager who participated owes a 5% tax (or $13,750); I would be shocked if Kimmel weren’t liable for this.

And there’s more: if the self-dealing isn’t corrected within the taxable period, the foundation faces a 200% tax, and managers face an additional 50% tax.

Foundations are also required to distribute at least 5% of their net asset value annually. Qualifying distributions include distributions for administrative expenses and for charitable purposes. The payments to KWF were not charitable, and probably don’t count toward the 5% distribution requirement. If those distributions put it over 5%, their disallowance would subject the foundation to an excise tax of 30% of the amount it underdistributed.

Also, the IRS can almost certainly revoke the Meyer Charitable Foundation’s tax exemption. To qualify as exempt, an organization cannot provide private inurement (that is, personal benefit). Paying bribe money to get a manager’s children into college? Almost certainly private inurement.

I Wish I Were Teaching Nonprofits This Semester

Ultimately, I wish I were teaching nonprofits this semester. If nothing else, the world around the college admissions scandal is the kind of final exam question that writes itself.

[fn1] I’m actually surprised that he’s still included on the fund’s website. I imagine that will change in the foreseeable future, so here’s a permalink to the page as it appears at 11:18 am on March 15, 2019.

[fn2] That is, a 20% long-term capital gain rate and a 3.8% net investment income tax rate.

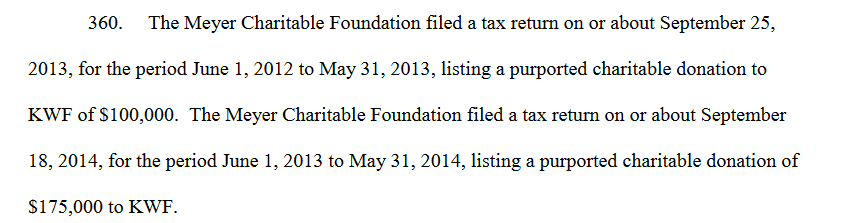

I pulled down the 2013 and 2014 Meyer Charitable Foundation 990-PFs from Guidestar (we have a subscription). Not only did the $100,000 inflate contributions for that year, the entire $967,650 of donations for that year were applied to the prior year, to cover undistributed income of $966,210.

Furthermore, the 2014 MCF 990-PF shows a $175,000 contribution to KWF. Total contributions that year were $1,074,325, covering prior year undistributed income of $1,068,515.

LikeLike