Call for Papers

AALS Section on Nonprofit and Philanthropy Law

2023 Annual Meeting

January 4-7

San Diego, CA

Nonprofits & Philanthropy

The AALS Section on Nonprofit and Philanthropy Law announces a call for papers to be presented as works-in-progress in our committee session at the 2023 AALS Annual Meeting in San Diego, CA from January 4-7, 2023.

The Section seeks submissions on a variety of topics and methodological approaches related to Nonprofit and Philanthropy Law. Given the recent importance and novelty of state nonprofit law, we are especially interested in scholarship that illuminates, elucidates, and otherwise engages with the work states are doing in the nonprofit world, but are happy to consider any scholarship in the field. We are interested in all states of article development.

Eligibility: Scholars teaching at AALS member or nonmember fee-paid schools. We particularly encourage new voices in the field to submit.

Due Date: June 15, 2022

Form and Content of Submission: Submissions may range from early drafts to articles that have been submitted for publication, but not articles that will have already been published by January 7, 2023.

Submission Method: please submit papers electronically to sbrunson@luc.edu with “AALS Nonprofit and Philanthropy Law Submission” in the email subject line.

Submission Review: Papers will be selected for inclusion in the program after review by members of the AALS Section on Nonprofit and Philanthropy Law.

Additional Information: Presenters are responsible for their own expenses associated with the conference. If you have any questions, please contact the chair, Sam Brunson, at sbrunson@luc.edu.

Author: Sam Brunson

I'm a tax law professor at the Loyola University Chicago School of Law.

“Taxman” (Sam’s Version)

By Sam Brunson

Almost seven years ago(!), Leandra wrote about the Beatles’s “Taxman” to celebrate its 50th anniversary. At around the same time, I tried to figure out and record the song.

At the time, unfortunately, neither my playing nor my recording chops were up to the challenge. Over the pandemic, though, I spent some time and money on instruments and recording equipment and have gotten a lot better at it.

So about a week ago, I decided to record a version of “Taxman.” I listened around to various versions and ended up modeling my version largely on the recording by Bill Wyman’s Rythm Kings (and, to a lesser extent, Soulive).

Continue reading ““Taxman” (Sam’s Version)”Taxing Venmo?!?

By Samuel D. Brunson

Over the last couple weeks, I’ve seen people in a couple very disparate groups worry about the 1099s they’re going to receive. (One group is saxophone enthusiasts who occasionally sell instruments and mouthpieces on eBay and Reverb.)

And why are they worried? Basically because the American Rescue Plan Act of 2021 makes it much more likely that they’ll receive 1099s, even for casual selling. Section 6050W of the Code requires companies like Paypal and Venmo (and other non-credit card payment processors) to report payments made, both to the payees and to the IRS.

Continue reading “Taxing Venmo?!?”Advance Payments of the Child Tax Credit

By: Sam Brunson

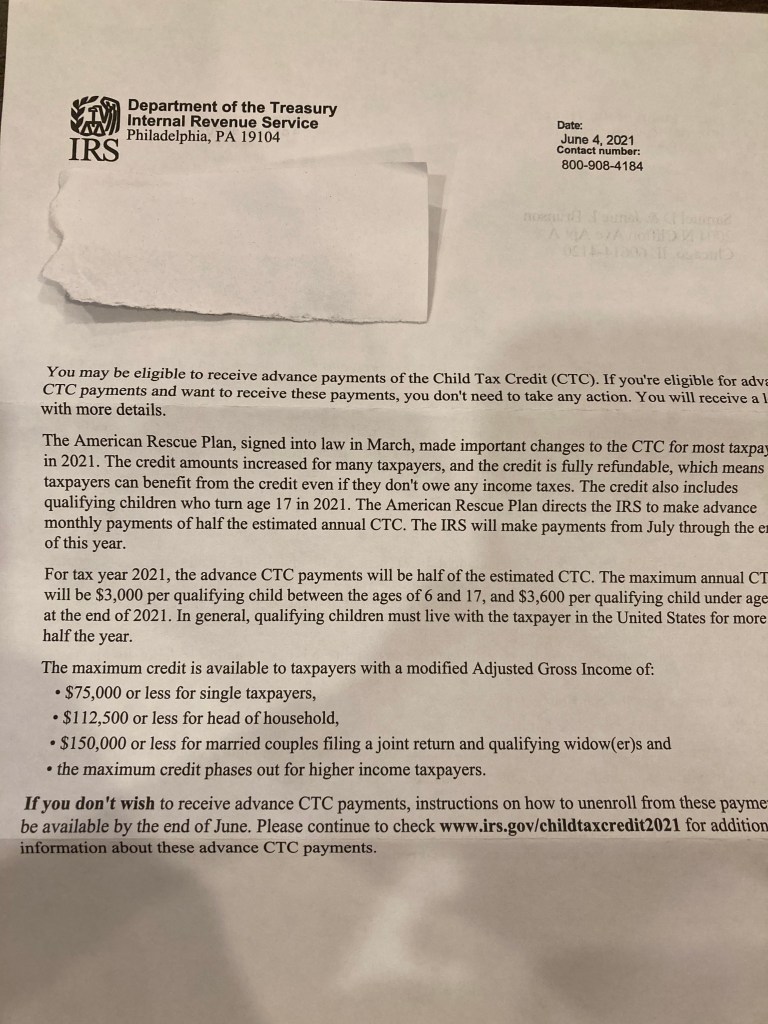

Yesterday my neighbor texted me to mention that three pieces of my mail had been left in his mailbox; he dropped them off in front of my door. Two were just standard junk mail but one is potentially important: a letter from the Department of the Treasury.

Perhaps you also got this letter: it has some important information about the way the the child tax credit now works. In short, the American Rescue Plan, a law signed in March, makes a number of significant changes to the child tax credit.

Two of those changes are particularly notable. First, it increases the amount of the credit to $3,000 for most children and $3,600 for children five and younger.

Second, it makes allows the IRS to make advance payments of the child tax credit. Essentially, unless parents choose otherwise, starting in July the will receive monthly payments of $250 or $300 per child (depending on the child’s age).

Third, the credit is fully refundable. Even if a parent doesn’t have enough income to owe taxes, they will receive the full amount of the child tax credit.

Finally, the age limit for the child tax credit has been increased from 16 to 17. (Note that currently these changes are all temporary–they only apply to 2021, though the may be extended as some point.)

Continue reading “Advance Payments of the Child Tax Credit”Project Veritas and Illegality

By Sam Brunson

On November 5—two days after the presidential election—James O’Keefe posted an interview with a postal worker claiming that he and his colleagues were instructed to backdate ballots that they received after election day. The next day he filed an affidavit swearing that he and his colleagues had been instructed to continue picking up ballots after the November 3 deadline.

After an interview with U.S. Postal Service investigators, Richard Hopkins, the postal worker, recanted his statements. He also told investigators that his affidavit had been written by Project Veritas, the organization O’Keefe founded and with which he is associated.

Project Veritas, it turns out, is a tax-exemption organization. And its association with Hopkins may have put its exemption at risk. By signing an untrue affidavit, Hopkins almost certainly broke the law. And several attorneys interview in the Salon story say that Project Veritas may also have broken the law as a result of its involvement in the false affidavit.

Continue reading “Project Veritas and Illegality”#TrumpTaxReturns

By Sam Brunson

For the last several months, I’ve been meeting a guitarist and sometimes other musicians at a Chicago park to play outdoor socially-distanced jazz. This Sunday, driving home, my wife asked me if we knew what Trump had paid in taxes. “Of course not,” I confidently responded. “It looks like we do now,” she said.

And with that, my work goals for this week changed. I’m sure everybody reading this has seen Sunday’s New York Times story (and probably also its follow-up from yesterday). Along with a ton of other tax people, I’ve been trying to make sense of and contextualize the story, both to myself and to the public. And I’ve largely been doing my thinking in real-time on Twitter.[fn1]

I thought that I’d assemble a lot of those Twitter threads here into one place. At most I’ll lightly edit them and I’ll link to the actual threads on Twitter, too. Because over there I included GIFs on almost every tweet and I think I outdid myself. The relevant content will be here, though. Continue reading “#TrumpTaxReturns”

How the Espinoza Tax Credits Work

By Sam Brunson

On Tuesday the Supreme Court issued its opinion in Espinoza, holding that Montana couldn’t prohibit “student scholarship organizations” from making tuition payments to religiously-affiliated private schools. I wrote about the decision over on the Nonprofit Law Prof Blog.

After writing the post, I saw this entry in a SCOTUSblog symposium on the Espinoza decision. And, like the authors of that piece, I found the Supreme Court’s decision unsurprising (for reasons that I mention on the other blog). But one part of their analysis jumped out at me as reflecting a critical misunderstanding of the way Montana’s tax credit scheme worked.

Specifically, the authors wrote:

The secular instruction in these schools means that the state gets full secular value for its money. There are complications in putting a dollar amount on this secular value. It might be the schools’ full cost, given that they satisfy compulsory-education requirements. Or some of the cost might be attributed to teaching religion. But one thing we know: the secular value is far more than zero. A $2,250 tuition voucher (the amount involved in the court’s 2002 decision in Zelman v. Simmons-Harris) can easily be allocated entirely to secular value. All the more so in Espinoza, where the tax credit was capped at $150.

(Emphasis mine.)

This paragraph isn’t critical to the blog post; it’s not mentioned in the majority’s analysis. And yet I’m afraid it may have been in the back of the mind of the Justices. Because, after all, what’s $150 out of private school tuition? Continue reading “How the Espinoza Tax Credits Work”

Taxing Student Athletes: An Explainer

By Sam Brunson

![]() About a month ago, California Governor Newsom signed the Fair Pay to Play Act, which allowed California college athletes to be paid for the use of their image, name, and likeness. Other states, including Illinois, have proposed similar legislation. And today, the NCAA caved; though its concession is not entirely clear, it looks like the NCAA has paved the way to allow NCAA athletes to make money off of their image.

About a month ago, California Governor Newsom signed the Fair Pay to Play Act, which allowed California college athletes to be paid for the use of their image, name, and likeness. Other states, including Illinois, have proposed similar legislation. And today, the NCAA caved; though its concession is not entirely clear, it looks like the NCAA has paved the way to allow NCAA athletes to make money off of their image.

For some reason, this has provoked backlash by Senator Burr of North Carolina. On Twitter, he announced that he plans on introducing legislation that would tax college athletes who accepted payment for the use of their image, etc., on their scholarships. Continue reading “Taxing Student Athletes: An Explainer”

The Kiddie Tax Needs a Better Fix Pt. 2

By Sam Brunson

As I explained in my previous post, the new kiddie tax is an absolute mess, with unintended and (I assume) unforeseen consequences that significantly harm, among others, poor college students and the children of service members killed in action. How is Congress going to fix this?

Poorly, I assume. And insufficiently.

I saw on Twitter yesterday that Rep. Cindy Axne is cosponsoring the Gold Star Family Tax Relief Act. Under the proposed legislation, the definition of “unearned income” will exclude survivor benefits received by the children of deceased service members. If this legislation were to pass, children of military members killed in action would no longer pay taxes at the top marginal rate on their survivor’s benefits. Continue reading “The Kiddie Tax Needs a Better Fix Pt. 2”

The New Kiddie Tax Needs a Better Fix Pt. 1

By Sam Brunson

One of the first articles I published as an academic was on the kiddie tax. It was a sleepy corner of the tax world; most of the academic literature on the kiddie tax came from the 1980s.[fn1] And, for its first three decades, the kiddie tax stayed almost exactly the same.[fn2] Then, in a little-noticed provision of the TCJA, Congress fundamentally changed the kiddie tax. In response, I addressed the kiddie tax a second time in a piece for Tax Notes entitled Meet the New “Kiddie Tax”: Simpler and Less Effective. [Paywall] It turns out that I underestimated the ways in which is was not only less effective, but actually dangerously counterproductive.

But first, a quick primer into what the kiddie tax was and what it has become. In 1986, Congress had become worried that wealthy taxpayers were shifting income-producing assets to their children so that they could lower their tax bills. The tax game would go something like this: wealthy dentist father gives (or, I suppose, sells for a nominal amount) his x-ray machines to his 7-year-old daughter. He then leases back the x-ray machines for, let’s say, $10,000 a year. In 1985, the top marginal tax rate was 50%. Assuming our dentist was in that tax bracket, he could deduct the $10,000 he paid to lease the x-ray machines. Meanwhile, assuming that his 7-year-old daughter didn’t have any additional income, she would have been in the 16% tax bracket. According to Rev. Proc. 84-79 (and ignoring any exemptions or deductions she might have), the daughter would pay taxes of $1,054 on the $10,000 of income. Meanwhile, Dad’s $10,000 deduction saved him $5,000 in taxes. By shifting passive income to his daughter, then, Dad saved almost $4,000.[fn3] (Note that it didn’t have to be dental equipment: it could be any income-producing property). Continue reading “The New Kiddie Tax Needs a Better Fix Pt. 1”

Jussie Smollett and the Illinois Film Tax Credit

By Sam Brunson

On Tuesday, Joe Magats, first assistant state’s attorney for Cook County, announced that he was dropping the charges against actor Jussie Smollett. Instead of a trial and punishment, Smollett agreed to forfeit his $10,000 bond and do community service.

Cook County prosecutors say this is a relatively normal type of alternative prosecution, one that prosecutors have recommended for over 5,700 offenders. It allows prosecutors to use their resources to prosecute violent offenders.

Not surprisingly, there’s some outrage about this alternative prosecution, notably from Chicago Mayor Rahm Emanuel and CPD Superintendent Eddie Johnson. But this is a tax blog, not a criminal justice blog, so questions about the justice (or not) of dropping Smollett’s prosecution are outside of our usual scope. Which is why I’m going to focus, instead, on Illinois Representative Michael McAuliffe and his terrible, horrible, no good, very bad bill. Continue reading “Jussie Smollett and the Illinois Film Tax Credit”

More on the College Admissions Scandal

By Sam Brunson

On Wednesday, I posted about how tax law played a central role in the college admissions scandal. As I’ve read through a little more of the affidavit, I decided to highlight two additional detail in this whole scandal, details that suggest that, for at least some of the participants, the tax consequences were very important.

Bruce Isackson and Facebook Stock

Bruce Isackson is the president of WP Investments, a real estate investment and development fund.[fn1] According to the affidavit, he used the fake athlete thing (soccer for the older daughter, rowing for the younger) to get two daughters into USC. He seems to have also paid for his younger daughter to get a better ACT score.

What’s interesting for purposes of this post is how he paid. Continue reading “More on the College Admissions Scandal”

Key Worldwide Foundation and College Admissions Scams

By Sam Brunson

When I first read about the massive college admissions scam, I read it for roughly the same schadenfreude as everybody else. It was an interesting—and frankly, kind of pathetic—story of wealth and entitlement.

And then I read the affidavit supporting the criminal indictment. And I learned that, as much as this is a story of wealth and entitlement, it’s more than that: this is a story that revolves around taxes. And specifically, the abuse of a tax-exempt organization.

There seem to have been two main schemes to get participants’ kids into schools they wouldn’t have otherwise qualified for. The first involved cheating on entrance exams. The second involved bribing athletic directors and others to designate their kids as athletic recruits (often in sports the kids didn’t play), and , each of which had its own fee structure. But each scheme had something in common. The recipient of the payments was Key Worldwide Foundation. Continue reading “Key Worldwide Foundation and College Admissions Scams”

A Mission From God: Blues Brothers and Tax

By Sam Brunson

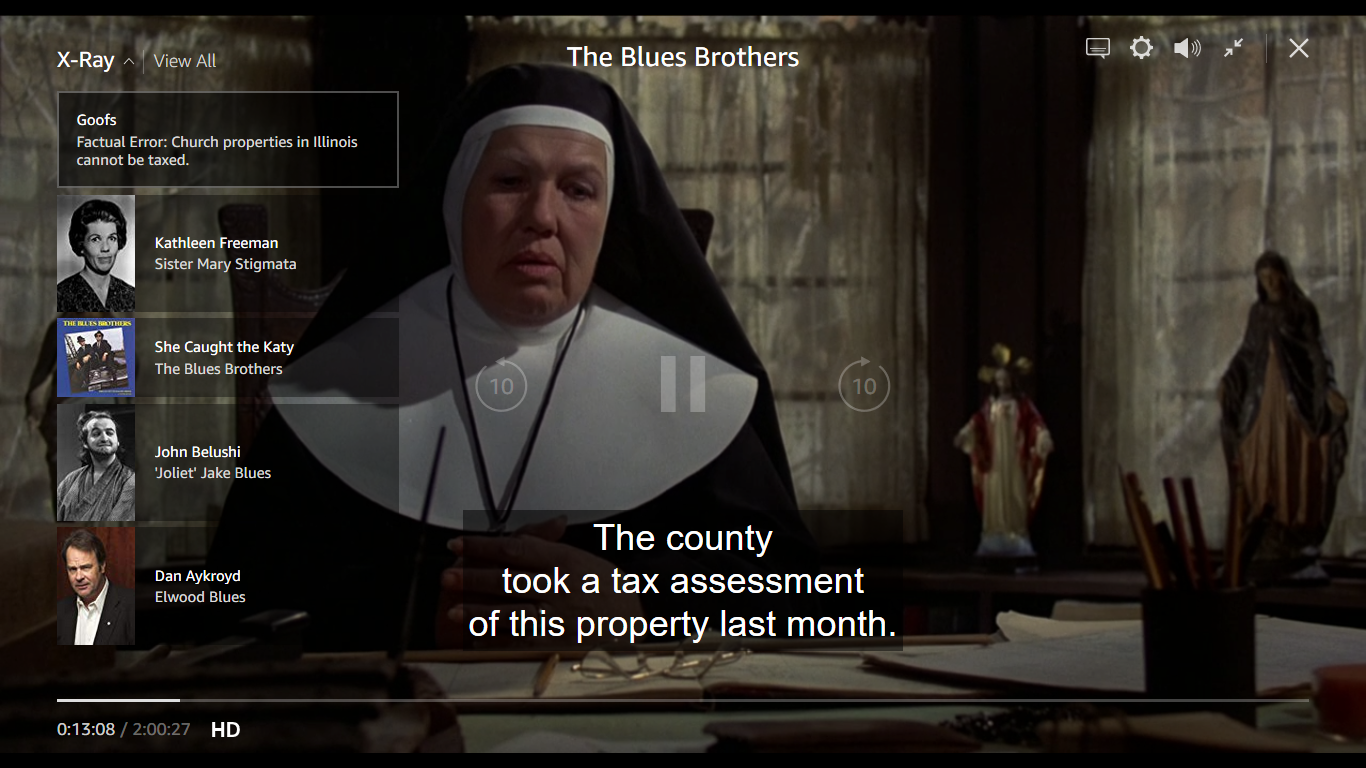

On February 1, Amazon Prime Video started streaming Blues Brothers. Now, in spite of its being one of the great movies of the 20th century, and having one of the greatest soundtracks ever, I hadn’t seen it in years, and definitely not since I moved to Chicago. So I decided to watch it, both because I love the movie and because I wanted to see its view of Chicago now that I know this city.

I remembered that the plot revolved around Jake and Elwood trying to raise $5,000 for the orphanage they grew up in or the orphanage will be closed, but I’d forgotten that the $5,000 was to pay the orphanage’s property tax assessment:

I’d also never watched a movie with Amazon’s X-Ray feature before. And X-Ray announced that the motivation for their mission from God is a factual error, because Illinois doesn’t tax church property.

Is that true? Continue reading “A Mission From God: Blues Brothers and Tax”

#AcademyAwards2019, Swag Bags, and the IRS

By Sam Brunson

Every year, it seems like there’s something in the news about the Academy Awards swag bags (valued at $100,000 this year!) and taxes. And, since the Academy Awards are tonight, and since this is a tax blog, we might as well say something about the taxation of swag bags. And wouldn’t you know it: an article had a decently bad take on the taxation, giving me a hook for a tweetstorm, which I now reproduce here for your reading pleasure. Happy Academy Awards Day!

I assume by now that everybody knows that #AcademyAwards2019 swag bags are taxable income to the recipients. But there are at least one thing in this article that needs to be corrected, and another than needs pushback. 1/ https://t.co/icqjcIlr9e

— Sam Brunson (@smbrnsn) February 24, 2019

Continue reading “#AcademyAwards2019, Swag Bags, and the IRS”

{kind=link}