Call for Papers

AALS Section on Nonprofit and Philanthropy Law

2023 Annual Meeting

January 4-7

San Diego, CA

Nonprofits & Philanthropy

The AALS Section on Nonprofit and Philanthropy Law announces a call for papers to be presented as works-in-progress in our committee session at the 2023 AALS Annual Meeting in San Diego, CA from January 4-7, 2023.

The Section seeks submissions on a variety of topics and methodological approaches related to Nonprofit and Philanthropy Law. Given the recent importance and novelty of state nonprofit law, we are especially interested in scholarship that illuminates, elucidates, and otherwise engages with the work states are doing in the nonprofit world, but are happy to consider any scholarship in the field. We are interested in all states of article development.

Eligibility: Scholars teaching at AALS member or nonmember fee-paid schools. We particularly encourage new voices in the field to submit.

Due Date: June 15, 2022

Form and Content of Submission: Submissions may range from early drafts to articles that have been submitted for publication, but not articles that will have already been published by January 7, 2023.

Submission Method: please submit papers electronically to sbrunson@luc.edu with “AALS Nonprofit and Philanthropy Law Submission” in the email subject line.

Submission Review: Papers will be selected for inclusion in the program after review by members of the AALS Section on Nonprofit and Philanthropy Law.

Additional Information: Presenters are responsible for their own expenses associated with the conference. If you have any questions, please contact the chair, Sam Brunson, at sbrunson@luc.edu.

Category: Conferences and Workshops

Whistleblowers and Disinformation — Roundtable #2: The Public Sector

By Diane Ring

We are back again this week looking at the role of misinformation and disinformation in democracy, good governance, and well-grounded decisionmaking! On Friday, we are hosting the second Roundtable in the Whistling at the Fake research project (with Dr. Costantino Grasso as PI, and funded by NATO’s Public Diplomacy Division). In our first Roundtable, we focused on disinformation in the private sector.

This Friday February 25, 2022 at 10:00am EST, the subject is Disinformation and the Public Sector.

The Roundtable includes three sessions: (1) Democracy and Disinformation – the Political Level; (2) Disinformation and Public Administration; and (3) Special Issues and Final Recommendations. The international panel includes experts from law, media, government, and civil society, along with whistleblowers. To join this exciting Roundtable session, register here!

Whistleblowers and Disinformation: “Whistling at the Fake” Roundtable

By Diane Ring

Information lies at the heart of a sound democracy, good governance, and well-grounded decision making, whether at the individual, community, business, or government level. Yet every day we see how misinformation and disinformation undermines all of these goals.

In response to this problem, a new research project, Whistling at the Fake (with Dr. Costantino Grasso as PI, and funded by NATO’s Public Diplomacy Division) aims to address the gap in the public’s understanding of the full scope and impact of misinformation and disinformation, and to empower the general public and regulators with tools, suggestions and recommendations for the future. The project focuses in particular on the role of whistleblowers and other informed insiders in “exposing misleading and hostile information activities and increasing public resistance to acts of this nature.”

As part of its project, Whistling at the Fake is hosting Roundtables on zoom– the first of which is this Friday, January 28, 2022 at 10:00am EST. The Roundtable, “Disinformation and the Private Sector” includes three sessions: (1) Exploring the Phenomenon, (2) Disinformation and Corporate Power and Wealth, and (3) Special Issues and Recommendations. The international panel includes experts from law, media, business, research, along with whistleblowers. To join what should be an amazing zoom Roundtable, register here!

International Symposium: “The Professionals: Dealing with the Enablers of Economic Crime”

By Diane Ring

Just as summer is in full swing, the VIRTEU Project is back with a close look at a less than sunny side of economic life — the role that professionals (read lawyers, accountants and auditors) can play in enabling economic crime. This coming Wednesday July 21, 2021 (starting at 10:15am ET) join us in a three-panel zoom symposium that investigates how and why professionals may play this enabling role, and what responses and solutions we might consider. We will look carefully at real life case studies and talk with experts from various sectors as we explore this ongoing issue.

Register here to join us for this zoom symposium.

Announcing the 2021 Indiana/Leeds Summer Tax Workshop Series!

By: Leandra Lederman

As I blogged previously, Dr. Leopoldo Parada from the University of Leeds School of Law and I (with the support of the Indiana University Maurer School of Law) will co-host the Indiana/Leeds Summer Tax Workshop Series again this summer. It will meet online via Zoom on Fridays from 11:30am-1pm Eastern Daylight Time (4:30-6pm British Summer Time). Last summer’s series went really well. If you are interested in cutting-edge tax issues, we hope you will consider attending!

We received numerous excellent submissions in response to this year’s Call for Papers. As stated there, we prioritized tax topics that would be of interest to scholars in multiple countries. Here is the list of speakers and the papers they’ll be presenting:

Like last year, the workshop will take place on Zoom, as a regular Zoom session. We will introduce the speaker, who will have about 20 minutes for scripted remarks, and the remainder of the time will be allocated to questions and discussion. Approximately a week in advance of each talk, we expect to share the draft paper online on the following website: law.indiana.edu/summer-tax.

The Indiana/Leeds Summer Tax Workshop Series is open to attendance by interested faculty, tax experts, and students. This summer, you will need to register in order to obtain the Zoom link and the password for any password-protected papers. Please register at TinyURL.com/INLeeds2021.

Students and other attendees who would like to list on their c.v. that they “participated in the 2021 Indiana/Leeds Summer Tax Workshop Series” should do the following:

- Attend at least 5 of the scheduled sessions.

- Type in the “chat” window of the Zoom session of each session you attend a brief introduction containing your name, school or other institution, location, and degree candidacy or job title.

We encourage all attendees to introduce themselves in the chat window, as well.

If you have questions, feel free to email us at llederma@indiana.edu and L.Parada@leeds.ac.uk. We hope to see you (virtually) this Friday and at the other sessions this summer!

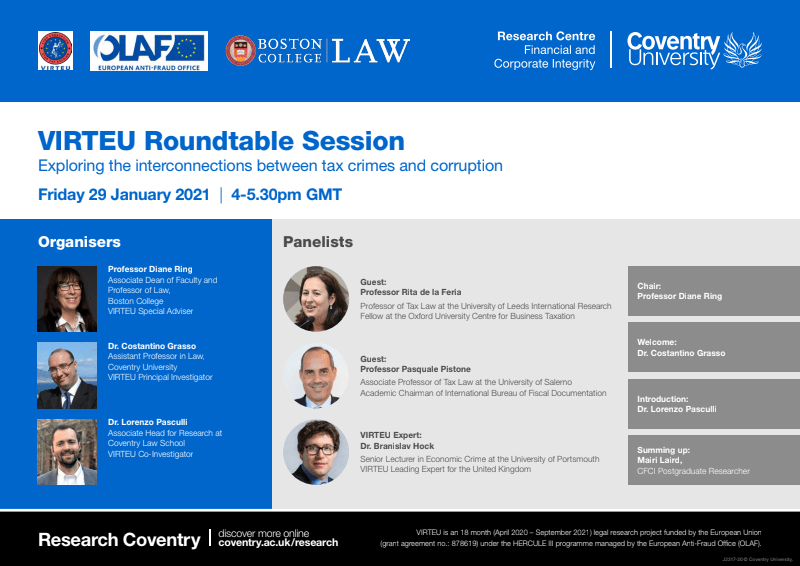

Institutional Corruption and Avoidance of Taxation: Final VIRTEU Roundtable

By Diane Ring

The most recent Roundtable session in the series of four VIRTEU [Vat fraud Interdisciplinary Research on Tax crimes in the European Union] sessions this spring focused on the limited success we have seen with the formal regimes of gatekeepers tasked with ensuring that taxpayers accurately meet their reporting and taxpaying obligations. The session then explored the role that whistleblowers play in remedying the resulting enforcement gaps. (A recording of this 3rd Roundtable is available here). Building on that discussion, the 4th and final Roundtable session, to be held Friday March 12, 2021 at 12:30pm EST (5:30pm GMT), will turn to the related topic, Institutional corruption and tax avoidance.

This March 12th discussion will examine corruption broadly understood to encompass not only the most direct forms of corruption (e.g. bribes) but more indirect forms (including implicit deals with officials), on to questions of undue influence, conflict of interest and the power of lobbying. Attention will be given to not only government actors, but also structural and institutional features that impact corruption and avoidance of taxation, including the role of large corporations, wealth, and power bases. For more information on the Roundtable, see below. To join us for the discussion, please register here.

VIRTEU Roundtable #3: Whistleblowing, Reporting, and Auditing in the area of taxation

by Diane Ring

We do not yet live in a world in which taxpayer compliance can simply be assumed. Instead, we must rely on the interplay of reporting requirements, internal and external auditing, and ultimately whistleblowing, to help ensure compliance with the tax system. How do they fit together? What can we expect from reporting and auditing? When do they breakdown, and why? How does whistleblowing–both the actual cases and the “threat” of whistleblowing–shape law, taxpayer behavior, and society’s understanding of compliance. And when does this tax noncompliance intersect with government corruption and fraud? What recommendations and options might we consider for the future?

Next week, the VIRTEU Roundtable Series tackles these questions in its 3rd Roundtable: “Whistleblowing, Reporting and Auditing in the area of taxation.” (VIRTEU [Vat fraud: Interdisciplinary Research on Tax crimes in the European Union]). This session builds on the first two Roundtables which gathered experts from around the world to discuss tax crime, corruption, CRS, and business ethics, and which can be viewed online: (1) Roundtable #1: Exploring the Interconnections between tax crimes and corruption; and (2) Rountable #2: CSR, Business Ethics, and Human Rights in the area of taxation.

The 3rd Roundtable, on “Whistleblowing, Reporting and Auditing in the area of taxation,” will be held Friday February 26, 2021 at 5:30-7:00pm GMT (12:30-2:00pm EST). For more information on the panel, see below. To join us, visit the registration link here.

CSR, Business Ethics & Human Rights through a Tax Lens: VIRTEU Roundtable Series Continues

by Diane Ring

Last month, the VIRTEU Roundtable Series launched with a discussion I had the opportunity to moderate on the basic connections between tax crime and corruption. (VIRTEU [Vat fraud: Interdisciplinary Research on Tax crimes in the European Union]). Clearly, we were only just getting started — the discussion ended because time was up but the questions continued. This week’s roundtable takes a closer look at the role that CSR (corporate social responsibility), business ethics and human rights can, should, or do play in business conduct, in tax enforcement strategies, and in the design of tax law itself.

These three frames for regulating (business) behavior are regularly examined and debated in the corporate and regulatory literature, but their application to the tax system remains under explored. If you are interested in thinking more about the tax side, join us this Friday February 12, 2021 at 5:30-7pm GMT (12:30-2:00pm EST). For more information on the panel, see below. To join, visit the registration link here.

Tax Crime and Corruption: VIRTEU Roundtable Series and Research

by Diane Ring

It is no surprise to those working in the tax field, whether in government, private practice, academia or the nonprofit sector, that not all taxpayer mistakes are innocent. Some taxpayers affirmatively engage in fraud, and sometimes that fraud is wrapped up with corruption. The high profile spate of tax leaks beginning in 2008 helped put a more public face on many aspects of an old problem.

As part of an effort to better respond to tax crimes and corruption, the EU has funded an interdisciplinary and comparative research legal research project — VIRTEU [Vat fraud: Interdisciplinary Research on Tax crimes in the European Union]. This project is aimed at exploring connections between tax fraud and corruption. Focused in part on VAT fraud, the relevant issues and the kinds of questions that must be asked are universal across the tax system.

VIRTEU, for which I am a special advisor, is hosting a Roundtable Discussion Series this spring that brings together experts from academic institutions, nongovernmental organizations, and the private sector to engage in topical discussions around the general problem of tax fraud and corruption. Along with the the VIRTEU project’s Principal Investigator Dr. Costantino Grasso and Co-Investigator Dr. Lorenzo Pasculli, I will be organizing and hosting the series, which is also sponsored by Boston College Law School, Coventry University Research Centre on Financial and Corporate Integrity, and OLAF (the European Anti-Fraud Office).

The first session, “Exploring the interconnections between tax crimes and corruptions“, will be held via Zoom on Friday January 29, 2021 (at 11:00am EST/ 4:00pm GMT). Here is the registration link. See below for more details – and join us for what promises to be an invigorating discussion of the connections between the legal and policy frameworks for corruption and for tax crimes.

Wrap-Up of the 2020 Indiana/Leeds Summer Tax Workshop Series

By: Leandra Lederman

The 2020 Indiana/Leeds Summer Tax Workshop Series ended on Thursday, after 13 weeks of talks. It was terrific getting to spend the summer with so many tax enthusiasts–professors, practitioners, and students–from all over the world! Dr. Leopoldo Parada and I really enjoyed co-hosting this series, and we expect to continue it next summer!

We received speaker permission to share videos of most of the talks. The speaker’s scripted remarks and our introductions are included. Those videos can be found at this link.

The complete speaker list and papers presented were as follows:

| May 21 | Ruth Mason, University of Virginia | The Transformation of International Tax |

| May 28 | Stephen Daly, King’s College London | Trust, Tax Administration and State Aid |

| June 4 | Susan Morse, University of Texas | Modern Custom in Tax |

| June 11 | James Repetti, Boston College | The Appropriate Roles for Equity and Efficiency in a Progressive Income Tax |

| June 18 | Diane Ring & Shuyi Oei, Boston College | Regulating in Pandemic: Evaluating Economic and Financial Policy Responses to the Coronavirus Crisis |

| June 25 | Umut Turksen, Coventry University | The Role of Human Factors in Tax Compliance and Countering Tax Crimes |

| July 2 | Allison Christians, McGill University | Accurately Counting Value in the International Tax System |

| July 9 | Joshua Blank, University of California, Irvine | Automated Legal Guidance |

| July 16 | Michael Devereux, University of Oxford | The OECD GloBE Proposal |

| July 23 | Ana Paula Dourado, University of Lisbon | The Concept of Digital Economy for Tax Purposes: a Reassessment |

| July 30 | Ricardo García Antón, Tilburg University | Enhancing the Group Interest in Transfer Pricing Analysis |

| Aug. 6 | Steven Dean, New York University | A Constitutional Moment in Cross-Border Taxation |

| Aug. 13 | Monica Victor, University of Florida | The Taxman’s Guide to the Galaxy: Allocating Taxing Rights in the Space-based Economy |

Thank you again to all those who joined us, and we hope to see you next year! #IndianaLeedsSummerTax

Call for Papers for the Indiana/Leeds Summer Tax Workshop Series

By: Leandra Lederman

This summer, the Indiana University Maurer School of Law and the University of Leeds School of Law will run a new Summer Tax Workshop Series. Dr. Leopoldo Parada from U. Leeds and I will host it. It will meet online via Zoom on Thursdays from 10:30am-noon Eastern time (3:30-5pm British Summer Time), starting May 21, 2020.

The Call for Papers opens today and will close on May 10, 2020 at midnight British Summer Time (7pm Eastern Daylight Time). If you are interested in presenting in the Workshop, please send the following before then to llederma@indiana.edu and L.Parada@leeds.ac.uk:

- Your name, title, and affiliation.

- The paper title and an Abstract of no more than 1,000 words.

- Whether or not you already have a draft of the paper. (We expect to circulate a draft of each paper—at least 10 pages—a week in advance of each talk.)

- Whether or not the paper has been accepted for publication.

- A list of any Thursdays between May 28 and August 6 that you would not be available to present, or a statement that any Thursday in that date range would work for you.

Continue reading “Call for Papers for the Indiana/Leeds Summer Tax Workshop Series”

IU Tax Policy Colloquium: Layser, “When, Where, And How To Design Community-Oriented Place-Based Tax Incentives”

By: Leandra Lederman

On January 23, the Indiana University Maurer School of Law welcomed our first Tax Policy Colloquium guest of the year: Prof. Michelle Layser from the University of Illinois College of Law. She presented her draft paper on the design of place-based tax incentives, then called “When, Where, And How To Design Community-Oriented Place-Based Tax Incentives,” and since retitled “How Place-Based Tax Incentives Can Reduce Geographic Inequality.” An updated draft is available on SSRN.

Shelly explained that this draft is the second paper in a multi-part project she is conducting on place-based tax incentives. Last year, she published the first piece in the series, “A Typology of Place-Based Investment Tax Incentives,” 25 Wash. & Lee J. Civ. Rights & Soc. Just. 403 (2019). Place-based tax incentives are geography-based incentives that generally are intended to help low-income areas by fostering investment in those areas. The 2019 article distinguished among place-based tax incentives on two dimensions: direct and indirect tax subsidies and spatially-oriented versus community-oriented incentives. “Direct tax subsidies provide tax breaks directly to businesses that invest in low-income communities.” (p. 415) Indirect tax subsidies are instead provided to investors in such business (pp. 417-18). She cites as examples the New Markets Tax Credit (NMTC) of IRC § 45D and the Opportunity Zones (OZ) provisions in IRC § 1400Z-1 et seq. (The OZ provisions are the most oddly numbered Internal Revenue Code sections I’ve ever seen!). Spatially-oriented tax incentives focus on specific geographically-defined Continue reading “IU Tax Policy Colloquium: Layser, “When, Where, And How To Design Community-Oriented Place-Based Tax Incentives””

Call for Papers: “Social Equality in the ‘Sharing Economy?’” Symposium (Indiana University, Bloomington)

The Indiana University (IU) Maurer Law School’s Indiana Journal of Law and Social Equality, in collaboration with IU’s Kelley School of Business and IU’s Ostrom Workshop, is hosting a symposium on the “gig” or “sharing” economy on February 13 and 14, 2020 at the Maurer School of Law in Bloomington, Indiana. The call for participation can be found here. The deadline for full consideration is November 27, 2019 at 5pm.

The Indiana University (IU) Maurer Law School’s Indiana Journal of Law and Social Equality, in collaboration with IU’s Kelley School of Business and IU’s Ostrom Workshop, is hosting a symposium on the “gig” or “sharing” economy on February 13 and 14, 2020 at the Maurer School of Law in Bloomington, Indiana. The call for participation can be found here. The deadline for full consideration is November 27, 2019 at 5pm.

The Indiana Journal of Law and Social Equality serves as an academic forum for scholars, practitioners, policymakers, and students to improve race and gender relations, foster new research in and across the disciplines, and provide an intellectual foundation for the pursuit of social justice.

The Kelley School of Business is consistently named among the top business schools in the world and is home to the Department of Business Law and Ethics, one of the largest and most well-respected departments of its kind. The Department continues Kelley’s strong business law tradition and advances research in a variety of business law fields, especially privacy, big data, and cybersecurity.

The Ostrom Workshop was founded at Indiana University in 1973 by Nobel laureate Elinor Ostrom and her husband, Vincent. Today, it carries forward their legacy by seeking and sharing solutions to the world’s most pressing problems involving communal and contested resources—from clean water to secure cyberspace.

Workforce and Workplace Trends: The Empirical Challenges and Policy Significance

By Diane Ring

On Thursday, my co-author (Shu-Yi Oei) and I had the opportunity to present on “Tax Related Challenges for Platform Workers” at the United States Government Accountability Office in downtown Boston. We enjoyed discussing our past and current research regarding taxation, platform workers, labor and emerging workforce trends with GAO researchers.

Our talk at GAO was particularly timely because we’re in the process of writing a book chapter for a new empirical volume, tentatively entitled “The Law and Policy of the Gig Economy: Qualitative Analysis,” which is forthcoming at Cambridge University Press (ed. Deepa Das Acevedo). This volume will address the promise of qualitative empirical approaches to studying the gig economy. Our contribution will build on our previous work in which we looked at the public online conversations among Uber and Lyft drivers regarding challenges they face in tax compliance.

Even without considering the impacts of the 2017 Tax Reform on both the gig economy and the broader workforce (which we have examined here, here and here), significant empirical questions remain regarding the tax and economic pressures faced by gig and contingent workers. Some, but not all, of those questions can be addressed by examining tax return and survey data. Add in tax reform to the mix (think the new section 199A deduction, the suspension of employee business deductions and the offshoring international provisions (section 250 and 956A)) and it’s clear we have a lot of work to do to better understand the interplay between tax and labor policies across many fields and how this will impact the future of the workplace. Our view is that it will take a combination of empirical approaches to get a well-textured picture of how tax impacts work.

U.S. Business Community Calls for Ratification of Tax Treaties in U.S. — Again

By Diane Ring

I have been wondering for the past few years why the business community has not put more pressure on the Senate to resolve the tax treaty roadblock created by Senator Rand Paul (R-KY). In 2011, newly-elected Senator Paul announced objections to the ratification of tax treaties and protocols and sought to block Senate consideration of those tax agreements in the pipeline. Senator Paul contended that the exchange of information provisions in the treaties violated taxpayers’ 4th amendment rights to privacy in their banking and financial data and that U.S. disclosure of such data to treaty partners would violate the due process rights of taxpayers. He succeeded in blocking the agreements (none have been ratified since 2010) and the result is a backlog of negotiated but unratified U.S. tax treaties and protocols.

A single senator can delay vote on a treaty and keep debate open. Negotiation with Senator Paul has not proven fruitful because he fundamentally objects to the information exchange provisions. However, other senators do have procedural recourse to end debate on a treaty and bring it to a vote. Under a process known as “cloture” (see Senate Rule XXII), a vote of 60 senators can force the end of debate. But this procedural path also requires an additional 30 hours of debate and the Senate can conduct no other business during this time. Thus, the cloture option puts a significant price tag on efforts to end the ratification impasse.

In a 2016 article (When International Tax Agreements Fail at Home: A U.S. Example), I mapped the historical and Senate procedural factors leading to the standstill on tax treaty ratification in the U.S. and the business community’s failed efforts to lobby ratification of tax treaties. For example, in 2013 several major U.S. business trade groups (including the Technology Industry Council, the National Association of Manufacturers, the National Foreign Trade Council, the U.S. Chamber of Commerce, and the United States Council for International Business) sent a letter to Senator Bob Corker stressing the importance of approving pending tax treaties and protocols. Senator Paul remained unmoved by business community pleas and apparently, the problem had not been considered serious enough to warrant commencement of cloture.

But it now appears that the business community has been reviving its public efforts to pressure the Senate to act: Continue reading “U.S. Business Community Calls for Ratification of Tax Treaties in U.S. — Again”