The Roundtable includes three sessions: (1) Democracy and Disinformation – the Political Level; (2) Disinformation and Public Administration; and (3) Special Issues and Final Recommendations. The international panel includes experts from law, media, government, and civil society, along with whistleblowers. To join this exciting Roundtable session, register here!

Information lies at the heart of a sound democracy, good governance, and well-grounded decision making, whether at the individual, community, business, or government level. Yet every day we see how misinformation and disinformation undermines all of these goals.

As part of its project, Whistling at the Fake is hosting Roundtables on zoom– the first of which is this Friday, January 28, 2022 at 10:00am EST. The Roundtable, “Disinformation and the Private Sector” includes three sessions: (1) Exploring the Phenomenon, (2) Disinformation and Corporate Power and Wealth, and (3) Special Issues and Recommendations. The international panel includes experts from law, media, business, research, along with whistleblowers. To join what should be an amazing zoom Roundtable, register here!

A dominant theme of international taxation over the past 15 years has been that of cooperation and consensus—from the BEPS Project to the new Multilateral Instrument to the new BEPS Inclusive Framework. Regardless of one’s assessment of nations’ true commitments to such cooperation and consensus, it is clear that notable changes in the framework of international tax engagement are afoot.

Yet, countries themselves remain very different in terms of the wealth, GDP, natural resources, tax revenues, commercial base, infrastructure, technological capacity, and financial systems. It is not obvious that cooperation and consensus are uniformly in countries’ interests, particularly in light of who is drafting the agenda. Most pointedly, it is reasonable to ask why non-OECD, non-G20 countries would be willing to commit to global tax cooperation.

Just as summer is in full swing, the VIRTEU Project is back with a close look at a less than sunny side of economic life — the role that professionals (read lawyers, accountants and auditors) can play in enabling economic crime. This coming Wednesday July 21, 2021 (starting at 10:15am ET) join us in a three-panel zoom symposium that investigates how and why professionals may play this enabling role, and what responses and solutions we might consider. We will look carefully at real life case studies and talk with experts from various sectors as we explore this ongoing issue.

This summer, the Indiana University Maurer School of Law and the University of Leeds School of Law will run the Indiana/Leeds Summer Tax Workshop Series again. Like last summer, Dr. Leopoldo Parada and I will host it. It will meet online via Zoom on Fridays from 11:30am-1pm Eastern time (4:30-6pm British Summer Time), starting May 28, 2021. We expect to invite a couple of speakers and select the remainder from a call for papers.

The Call for Papers opens today and will close on May 14, 2021 at midnight British Summer Time (7pm Eastern Daylight Time). If you are interested in presenting in the Workshop, please send the following before then to both llederma@indiana.edu and L.Parada@leeds.ac.uk, with “Indiana/Leeds Workshop submission” in the subject line of your email:

Your name, title, and affiliation.

The paper title and an abstract of no more than 1,000 words.

Whether or not you already have a draft of the paper. (We plan to circulate a draft of each paper—a minimum of 10 pages—a week in advance of each talk.)

Whether or not the paper has been accepted for publication, and, if so, when it is expected to be published.

A list of any Fridays between May 28 and July 16 that you would not be available to present, or a statement that any Friday in that date range would work for you.

In selecting papers, preference will be given to tax topics of broad, general interest. These can involve international or domestic tax issues, but a preference will be given to topics that would be of interest to scholars in more than one country. Like last summer, we expect an international group of attendees. Note also that speakers will be strongly encouraged to limit their scripted remarks to 20 minutes, to allow ample time for questions and discussion.

Videos of all but one of last summer’s talks are online at http://www.tinyurl.com/indianaleeds. These recordings include only the introductory remarks and the scripted portion of the speaker’s presentation. We plan to take the same approach this summer for those speakers who grant permission.

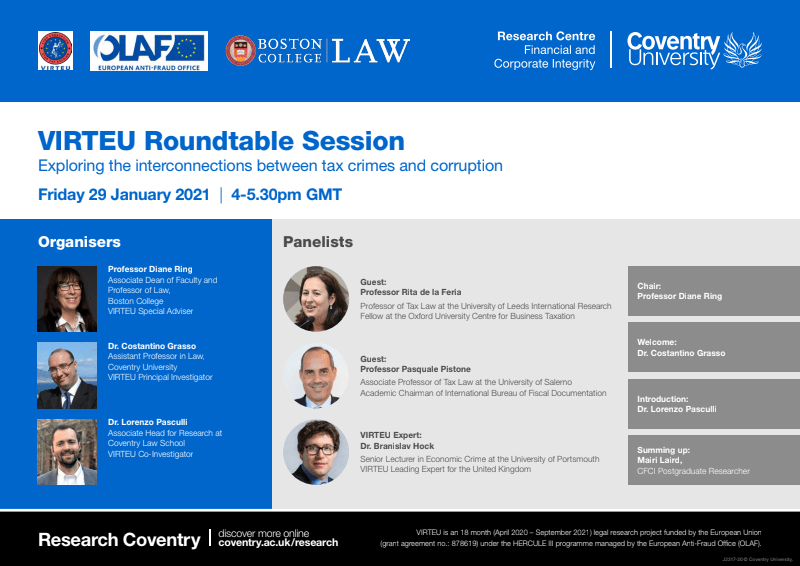

This March 12th discussion will examine corruption broadly understood to encompass not only the most direct forms of corruption (e.g. bribes) but more indirect forms (including implicit deals with officials), on to questions of undue influence, conflict of interest and the power of lobbying. Attention will be given to not only government actors, but also structural and institutional features that impact corruption and avoidance of taxation, including the role of large corporations, wealth, and power bases. For more information on the Roundtable, see below. To join us for the discussion, please register here.

We do not yet live in a world in which taxpayer compliance can simply be assumed. Instead, we must rely on the interplay of reporting requirements, internal and external auditing, and ultimately whistleblowing, to help ensure compliance with the tax system. How do they fit together? What can we expect from reporting and auditing? When do they breakdown, and why? How does whistleblowing–both the actual cases and the “threat” of whistleblowing–shape law, taxpayer behavior, and society’s understanding of compliance. And when does this tax noncompliance intersect with government corruption and fraud? What recommendations and options might we consider for the future?

The 3rd Roundtable, on “Whistleblowing, Reporting and Auditing in the area of taxation,” will be held Friday February 26, 2021 at 5:30-7:00pm GMT (12:30-2:00pm EST). For more information on the panel, see below. To join us, visit the registration link here.

Last month, the VIRTEU Roundtable Series launched with a discussion I had the opportunity to moderate on the basic connections between tax crime and corruption. (VIRTEU [Vat fraud: Interdisciplinary Research on Tax crimes in the European Union]). Clearly, we were only just getting started — the discussion ended because time was up but the questions continued. This week’s roundtable takes a closer look at the role that CSR (corporate social responsibility), business ethics and human rights can, should, or do play in business conduct, in tax enforcement strategies, and in the design of tax law itself.

These three frames for regulating (business) behavior are regularly examined and debated in the corporate and regulatory literature, but their application to the tax system remains under explored. If you are interested in thinking more about the tax side, join us this Friday February 12, 2021 at 5:30-7pm GMT (12:30-2:00pm EST). For more information on the panel, see below. To join, visit the registration link here.

We’ve started a new YouTube series we wanted to share with our readers! It’s called “Break Into Tax” (BiT) and can be found at tinyurl.com/BreakIntoTax.

The idea behind BiT is that we’ll discuss and break down tax-related concepts, broadly defined. This includes issues that may be of interest to law students and others newer to tax or to particular issues. The topics we plan to cover include substantive tax law concepts, tax policy concerns, the study of taxation, and the pursuit of tax as a career. We also welcome suggestions for topics in the comments on our videos!

We come at the issues from the perspective of tax law professors in the U.S. and Canada with cross-border interests. The BiT series is not at all designed to be of interest only to people from these two countries. We expect to focus on concepts that are foundational enough or general enough to be of broad interest.

Our introduction video, located here, is a good place to start. It shares more about us and the BiT channel. Our first playlist covers Tax Policy Colloquia: what are they, how to ask a good question in a tax workshop, and tips for students writing reaction papers.

It is no surprise to those working in the tax field, whether in government, private practice, academia or the nonprofit sector, that not all taxpayer mistakes are innocent. Some taxpayers affirmatively engage in fraud, and sometimes that fraud is wrapped up with corruption. The high profile spate of tax leaks beginning in 2008 helped put a more public face on many aspects of an old problem.

As part of an effort to better respond to tax crimes and corruption, the EU has funded an interdisciplinary and comparative research legal research project — VIRTEU [Vat fraud: Interdisciplinary Research on Tax crimes in the European Union]. This project is aimed at exploring connections between tax fraud and corruption. Focused in part on VAT fraud, the relevant issues and the kinds of questions that must be asked are universal across the tax system.

VIRTEU, for which I am a special advisor, is hosting a Roundtable Discussion Series this spring that brings together experts from academic institutions, nongovernmental organizations, and the private sector to engage in topical discussions around the general problem of tax fraud and corruption. Along with the the VIRTEU project’s Principal Investigator Dr. Costantino Grasso and Co-Investigator Dr. Lorenzo Pasculli, I will be organizing and hosting the series, which is also sponsored by Boston College Law School, Coventry University Research Centre on Financial and Corporate Integrity, and OLAF (the European Anti-Fraud Office).

The first session, “Exploring the interconnections between tax crimes and corruptions“, will be held via Zoom on Friday January 29, 2021 (at 11:00am EST/ 4:00pm GMT). Here is the registration link. See below for more details – and join us for what promises to be an invigorating discussion of the connections between the legal and policy frameworks for corruption and for tax crimes.

The 2020 Indiana/Leeds Summer Tax Workshop Series ended on Thursday, after 13 weeks of talks. It was terrific getting to spend the summer with so many tax enthusiasts–professors, practitioners, and students–from all over the world! Dr. Leopoldo Parada and I really enjoyed co-hosting this series, and we expect to continue it next summer!

We received speaker permission to share videos of most of the talks. The speaker’s scripted remarks and our introductions are included. Those videos can be found at this link.

The complete speaker list and papers presented were as follows:

May 21

Ruth Mason, University of Virginia

The Transformation of International Tax

May 28

Stephen Daly, King’s College London

Trust, Tax Administration and State Aid

June 4

Susan Morse, University of Texas

Modern Custom in Tax

June 11

James Repetti, Boston College

The Appropriate Roles for Equity and Efficiency in a Progressive Income Tax

June 18

Diane Ring & Shuyi Oei, Boston College

Regulating in Pandemic: Evaluating Economic and Financial Policy Responses to the Coronavirus Crisis

June 25

Umut Turksen, Coventry University

The Role of Human Factors in Tax Compliance and Countering Tax Crimes

July 2

Allison Christians, McGill University

Accurately Counting Value in the International Tax System

July 9

Joshua Blank, University of California, Irvine

Automated Legal Guidance

July 16

Michael Devereux, University of Oxford

The OECD GloBE Proposal

July 23

Ana Paula Dourado, University of Lisbon

The Concept of Digital Economy for Tax Purposes: a Reassessment

July 30

Ricardo García Antón, Tilburg University

Enhancing the Group Interest in Transfer Pricing Analysis

Aug. 6

Steven Dean, New York University

A Constitutional Moment in Cross-Border Taxation

Aug. 13

Monica Victor, University of Florida

The Taxman’s Guide to the Galaxy: Allocating Taxing Rights in the Space-based Economy

Thank you again to all those who joined us, and we hope to see you next year! #IndianaLeedsSummerTax

Susan Morse and Stephen Shay have blogged on Procedurally Taxing on both May 22 and June 11 on Altera’s efforts to have the U.S. Supreme Court grant certiorari in Altera v. Commissioner. Altera is a closely followed case involving an administrative law challenge to the validity of a Treasury regulation, so I wanted to flag those blog posts for Surly Subgroup readers.

Recall that in Altera, the Court of Appeals for the Ninth Circuit upheld a cost-sharing regulation under IRC § 482, reversing the Tax Court’s unanimous decision invalidating the regulation as arbitrary and capricious. The Ninth Circuit ruled 2-1 for the government in both its original opinion, which was withdrawn due to the death of one of the judges on the panel, and again in a revised opinion. The Ninth Circuit also denied rehearing en banc, a victory for the IRS’s rulemaking process. (Full disclosure: in addition to joining in two earlier amicus briefs in favor of the Commissioner, which Susie and Steve spearheaded, I co-authored with them and Clint Wallace a 2019 amicus Brief in Opposition to the Petition for Rehearing En Banc.)

As I posted previously, this summer, Dr. Leopoldo Parada from the University of Leeds School of Law and I (with the support of the Indiana University Maurer School of Law) will co-host the new Indiana/Leeds Summer Tax Workshop Series. It will meet online via Zoom on Thursdays from 10:30am-noon Eastern time (3:30-5pm British Summer Time). If you are interested in cutting-edge tax issues, we hope you will consider attending!

We received many terrific submissions in response to the Call for Papers. As stated there, we prioritized tax topics that would be of interest to scholars in multiple countries. We are very fortunate to have Professor Ruth Mason from the University of Virginia kicking off what promises to be an outstanding series! The following is the full list of speakers and the papers they’ll be presenting: Continue reading “Announcing the 2020 Indiana/Leeds Summer Tax Workshop Series!”→

The Tax Policy Colloquium at Indiana University Maurer School of Law, which I’ve been blogging about, ran in person in Bloomington until our Spring Break. The fourth talk of the semester was given by Prof. Orly Mazur of SMU Dedman School of Law on March 5, 2020. She presented her interesting law-and-technology paper titled “Can Blockchain Revolutionize Tax Compliance?” (In general, she argued that it can’t: blockchain is unlikely to dramatically change tax enforcement by, for example, replacing third-party information reporting.)

The subsequent IU Tax Policy Colloquium talk, by Prof. Rita de la Feria of the University of Leeds School of Law, was on March 27. She presented a paper, coauthored with Michael Walpole of UNSW, titled “The Impact of Public Perceptions on VAT Rates Policy,” which is part of a larger project proposing a progressive VAT. The paper argues that, although having a single consumption tax rate that is broadly applied is most equitable, there typically are numerous exemptions and/or lower rates, for political economy reasons.

Prof. de la Feria

With the move to online classes due to the pandemic, this talk occurred via Zoom. It was unfortunate that, due to the pandemic, we were not able to host Rita in Bloomington. However, the silver lining was that I was able to invite tax experts and other faculty from all over the world to attend. Rita and I also both publicized the talk on social media. As a result, several academics and other tax experts either asked to attend, or, if they saw the notice too late, asked if there is a video they could watch, which there is. In addition to me, Rita, and the students in the class, there were 22 attendees, which produced a terrific discussion. The students later told me how wonderful it was to have so many international tax experts asking questions and making comments. Continue reading “Virtual Tax Policy Colloquia”→

On February 6, 2020, the Indiana University Maurer School of Law welcomed our second Tax Policy Colloquium guest of the year: Prof. Werner Haslehner from the University of Luxembourg’s Department of Law, who is currently a Global Research Fellow and adjunct professor at NYU Law School. Werner presented his draft essay titled “International Tax Competition—the Good, the Bad, and the Ugly.”

States of course compete for tax base. Werner’s essay explains that “States’ general freedom to act (which we may call sovereignty) and taxpayer’s freedom to choose (which we may call liberty) – although neither is without limits – inescapably lead to competitive pressures and reactions.” (p.4) And some of this competition has been labelled as “harmful” by the OECD, the European Commission, and others. Yet, the essay points out, there is no accepted definition of the phrase “harmful tax competition.” The essay briefly reviews the literature and points out differences in approach to defining this concept. This part of the essay draws in part on Lily Faulhaber’s compelling article, The Trouble with Tax Competition: From Practice to Theory, 71 Tax L. Rev. 311 (2018), which pointed out the lack of definitional consensus and offered a typology of tax competition.

Werner’s essay further argues that, as commonly understood, there is no economic standard that supports a distinction between “harmful” and other types of tax competition. The essay thus proposes to replace the phrase “harmful tax competition” with “unfair tax competition.” (p.13) The essay specifically proposes “to refer as a basis for such a constraint to one of the most salient principles of moral philosophy: Immanuel Kant’s categorical imperative. According to this norm’s first formulation, one is to ‘act only in accordance with that maxim through which one can at the same time will that it become a universal law’.” (p.16). The essay provides two examples of behaviors that would be considered “unfair” under this standard: (1) ring-fencing (the provision of a tax benefit only to foreigners, not domestic taxpayers) and (2) secrecy (which, in response to a question I posed, Werner clarified refers to “secrecy as a service”—assisting foreign taxpayers in tax evasion). Continue reading “IU Tax Policy Colloquium: Haslehner, “International Tax Competition—The Good, the Bad, and the Ugly””→

By:

By: