By: Leandra Lederman, with thanks to my in-house comics expert, Nickolas Cole

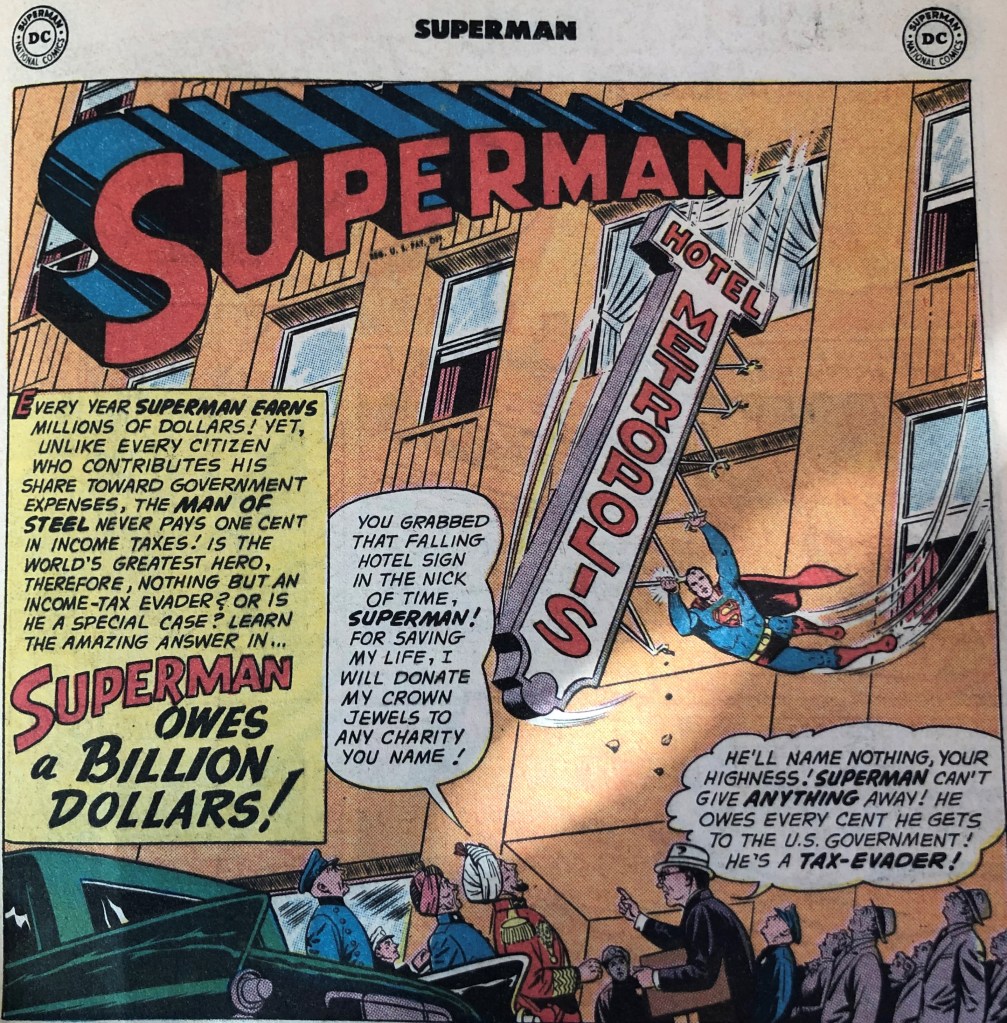

Nick, who’s been a Superman fan since childhood, got me the Oct. 1961 issue of the Superman comic for Christmas. It’s got a story in it billed as “Superman Owes a Billion Dollars” in taxes! Here’s the splash panel:

The basic premise is that a new Revenue Agent “at the Internal Revenue Bureau in Metropolis,” Rupert Brand,* discovers “no record that Superman has ever paid taxes!” (In case you’re wondering, nope, the IRS was not called the “Internal Revenue Bureau” back then. In 1953, it changed its name from the “Bureau of Internal Revenue” to the “Internal Revenue Service.” Perhaps a clue that not to rely on any of the tax statements in the story!)

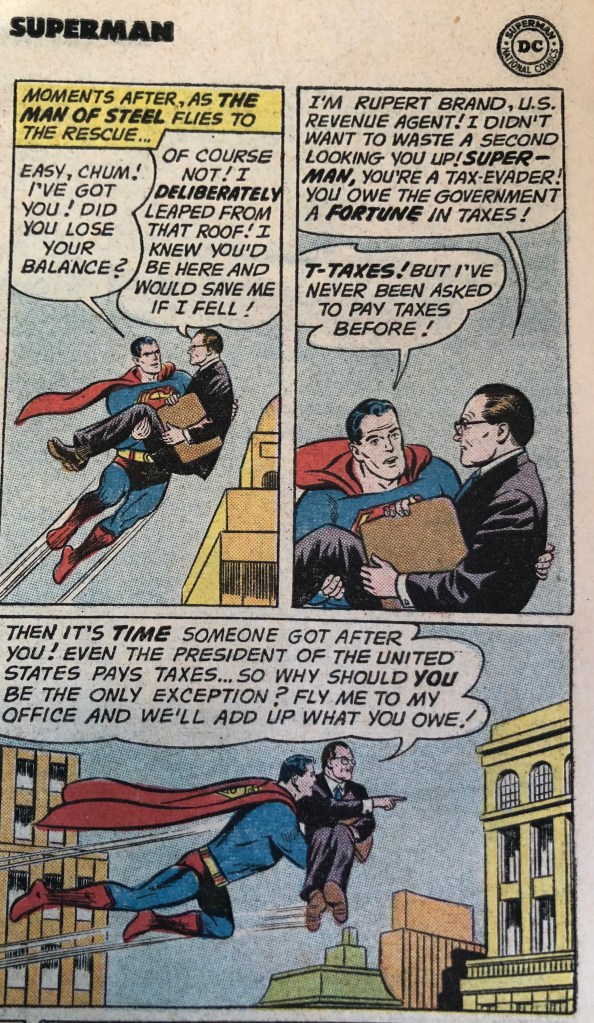

Brand figures out the quickest way to reach Superman about this apparent delinquency, and explains that even the President of the United States pays taxes (cf. these blog posts), and so must Superman!

Why does Superman owe tax? Well, the story explains that “each year, Superman captures countless criminals, collecting a fortune in reward money!” And not just that, “whenever he digs up buried treasure” [treasure trove, anyone?] “or squeezes coal into diamonds, he earns more untold millions! All that wealth is income!”

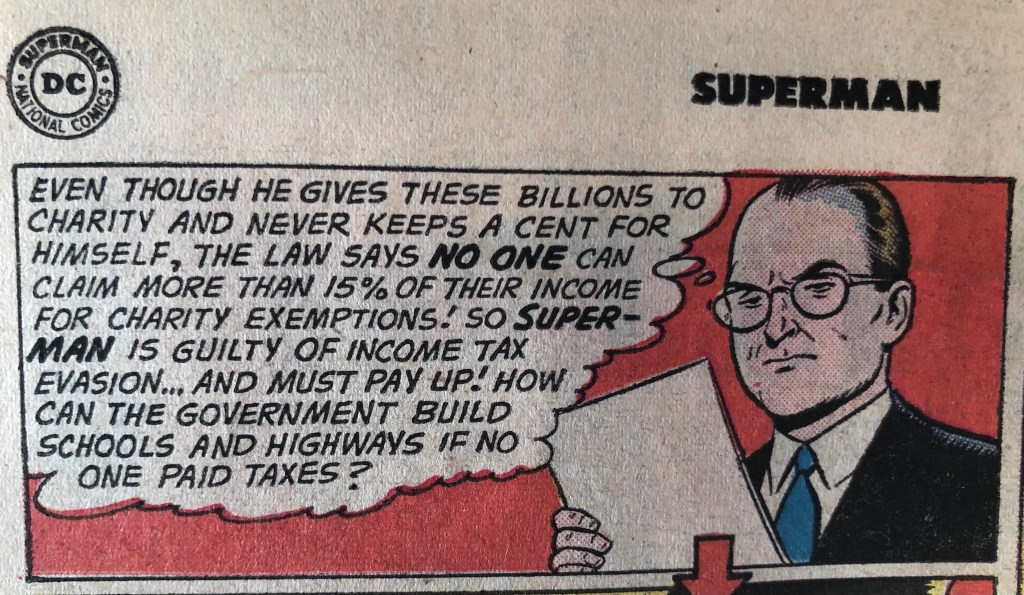

But wait! Superman does not keep any of the money—he’s the ultimate philanthropist! Here, the kids get a quick civics lesson, as well as a lesson on the charitable contribution deduction: You can’t just net your income and deductions and report nothing (although the comic doesn’t phrase it that way).

Wait, only 15% of charitable contributions are deductible? Is that historically accurate? Spoiler: Not really. According to this Congressional Research Service report, the 1954 Internal Revenue Code increased the limit “to 30% of AGI for donations to churches, educational institutions, or hospitals. (Donations to other organizations still subject to the 20% AGI limit.)” So, why 15%? Well, according to that report, 15% was the limit in 1917 (when the deduction was enacted), an exception for consistent donors was added in 1924, and the exception was removed in 1944. From 1944 to 1952, the cap for everyone was 15%, at which point it was raised to 20%.

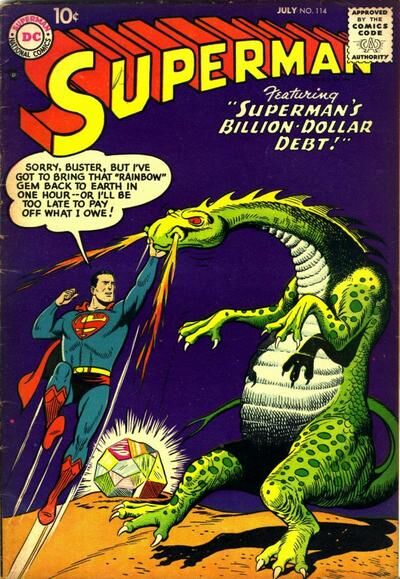

I had read that this 1961 story “recycles its plot from the story ‘Superman’s Billion-Dollar Debt!’ from Superman #114.” That issue has “a cover date of July, 1957.” (That comic looks very cool—the tax debt story is the cover story! And the details appear to be a bit different from the 1961 version.)

I thought perhaps the 15% cap was historically accurate at the time of this earlier comic, but the Congressional Research report I described above suggests that it was not. (I also don’t have the 1957 issue to check if the 15% figure was referenced there.) But I’m guessing that this was a historically salient limit, akin to how the 50% limit for individuals’ charitable contribution deductions is today.

In the story, Brand also reminds Superman that “Many millionaires give money to charity, too… yet they pay taxes!” And (oh, no!), “noon tomorrow is the tax deadline! If you don’t deliver $1,000,000,000… which includes your back taxes, I’ll order the F.B.I. to arrest you!” Wow, there’s a lot of creative license there. And what a high tax bill!

Nick told me that this kind of story is one in which Superman has a problem he can’t just easily solve with his superpowers. But Superman flies off to try to gather $1 billion in a day. He battles Bizarro; he brings in Aquaman for help producing the world’s biggest pearl; he contacts a professor for help—well, for a magic potion, actually; and Lori Lemaris (one of many, many LL characters in the Superverse) provides him with gold statues of his parents. (She is the sole female character with a speaking role in this story. )

We learn that Superman sent in Clark Kent’s tax return on time (phew!) but it looks like he fails to gather enough treasure to pay his billion dollar tax debt (not to mention that all that wealth he’s trying to produce would presumably also be gross income)! He hands Brand a check but—oops—“it was issued by the Bank of Krypton on your home world, which blew up long ago!” Was Superman intentionally writing a bad check, courting more prison time? Of course not. The Revenue Agent’s boss enters and saves the day!

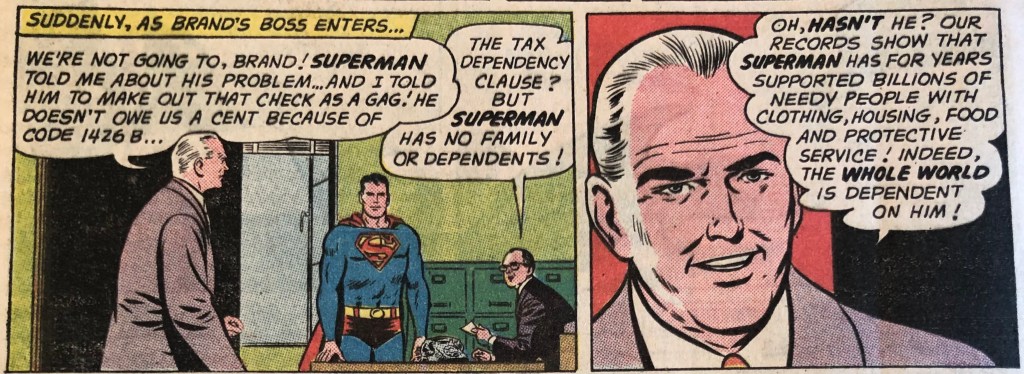

That’s an awfully specific citation in the left panel, “Code 1426B.” The dependency exemption was in section 151 of the 1954 Code (and in section 25 of the 1939 Code). I wasn’t sure if 1426B was invented to sound esoteric, or if it has some meaning. I Googled “Code 1426” and found a couple of U.S. Code references to aliens—8 U.S. § 1426 and 18 U.S.C. § 1426—but that could be coincidence. Superman’s status as an alien (perhaps a resident alien?) isn’t mentioned in the story. Nonetheless, CBR.com opines that “the ordinance quoted by Mr. Brand’s boss, ‘1426c’ (sic), was in all probability misprinted by the letterer instead of 26 U.S.C. 1441(c)(4), which provides that ‘[u]nder regulations prescribed by the Secretary, compensation for personal services may be exempted for deduction and withholding,’ if said services are rendered by a nonresident alien.”

I tend to doubt that the writer (Otto Binder, at least for the 1957 story) was trying to cite an actual Internal Revenue Code section in a story that doesn’t even reference the real IRS. For what it’s worth, my own preliminary guess is that “Code 1426B” is an Easter Egg referring in “Code” to a birthdate (the “B”). Superman’s creators, Jerry Siegel and Joe Shuster, were both born in 1914. “26” could be a reference to 1926, the year Superman was said to have landed on Earth in the 1950s’ Adventures of Superman TV series….

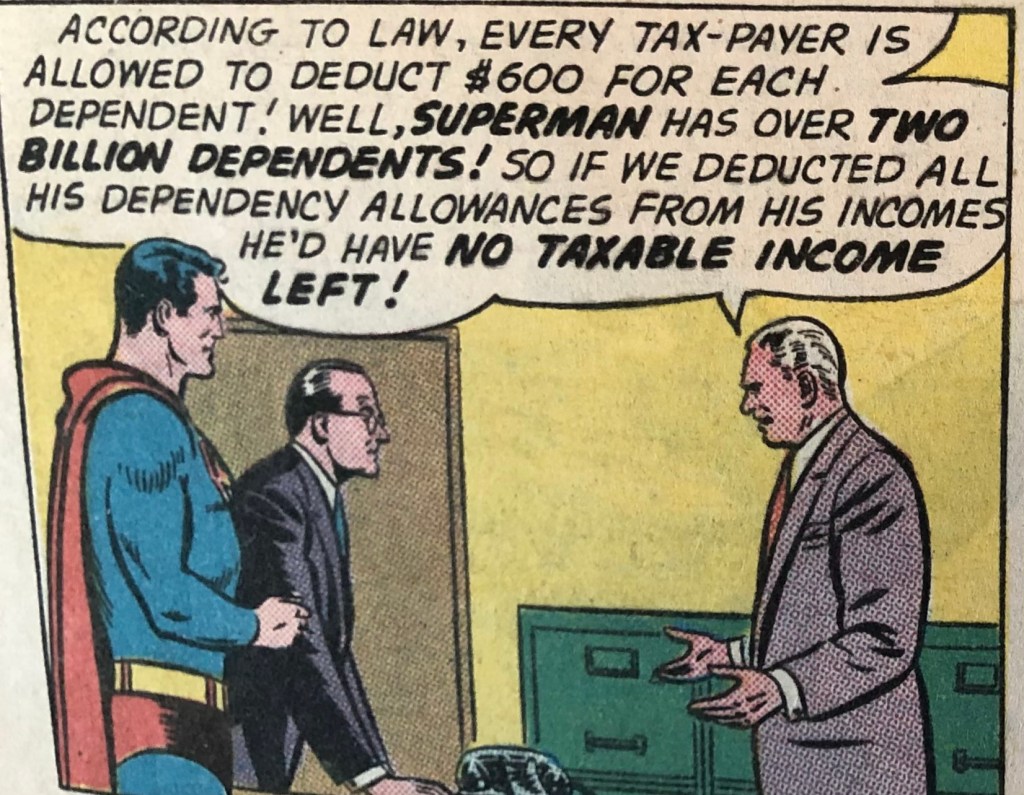

Anyway, Brand’s boss goes on to explain the dollar amount Superman can claim for each dependent:

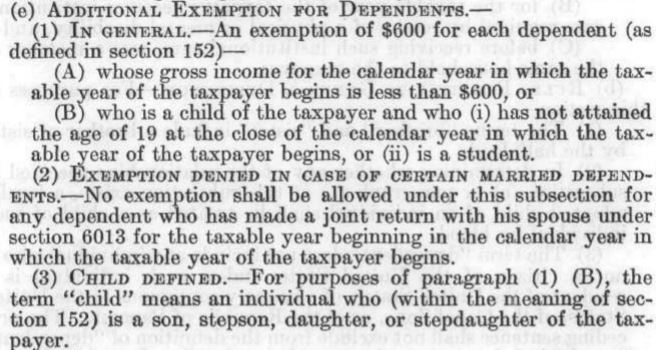

The $600 amount is correct as of the 1954 Code, though there were a lot more requirements in section 151 than the nameless boss makes it sound!

Section 152 also contains detailed requirements, starting with “the term ‘dependent’ means any of the following individuals over half of whose support … was received from the taxpayer….” I.R.C. § 152 (1954). So, more creative license was taken here, apparently! And this was an exemption, while the charitable donation provision that the story referred to as an exemption was actually a deduction…. Oh, well; it’s not tax advice. I suppose the important thing is that Superman is revealed not to be a tax evader! Brand admits it in the final panel and shakes Superman’s hand. Phew!

I’m not the first person to have written about this story. I found this post on The Legal Geeks; this one on CBR.com; and this similar one in the Times Union, in case you are interested in others’ takes. I also learned in the CBR.com post that this story was subsequently “reprinted in Superman #284” (in 1975) and in “Showcase Presents: Superman #3.”

Now, if you’re interested enough to have read this far, you may be wondering why a tax story was published as the cover story of a July issue. Comics are dated ahead of the actual release date (to be saleable for a longer period), but apparently only by two months. So, the July 1957 issue where this story first appeared would likely have appeared in stores in May of that year. The individual filing deadline was April 15 back then, as it is now, so my best guess was that kids’ parents were expecting tax refunds around the time the issue came out. But I’d welcome any intel on that or the 1426B reference!

* Does the Revenue Agent’s name, “Rupert Brand,” mean anything? No idea. But if the space between the first and last names is a blank that can stand for anything, one anagram of the name is “bankrupted”….