By: David J. Herzig

The Trump and Republican tax plans have circled around the idea of repealing the mortgage interest deduction. Although I’m not convinced it will happen (see e.g., Treasury Secretary Mnuchin’s remarks). The mere threat of the repeal has garnered a fair amount of attention.

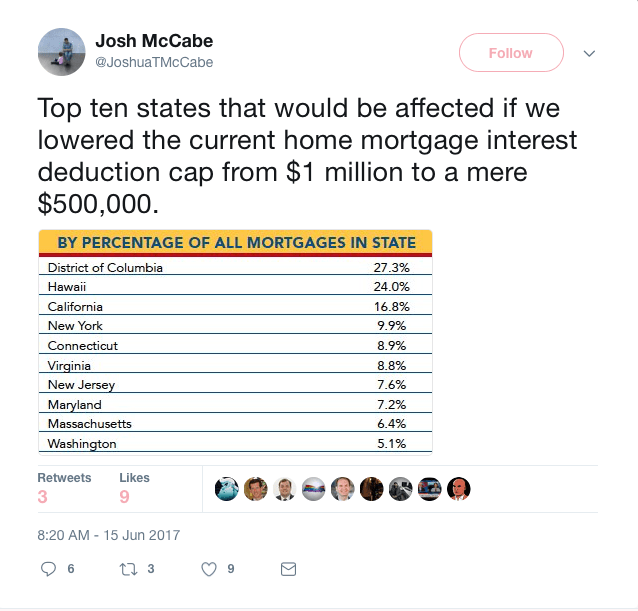

For example, the other day this chart was making its rounds on twitter.

I have not verified the methodology of the chart or the data. I interpret that the chart examines (in absolute numbers) how many mortgages exist at $1,000,000. The implicit conclusion of the chart is that homeowners in states like D.C., Hawai’i, California and New York have the most at stake in retaining the deduction.

Why?

Because there seems to be evidence that the mortgage interest deduction contributes to housing inflation. Back in 2011 the Senate held hearings on incentives for homeownership. [1] It has been suggested that the elimination of the deduction will drop home prices between 2 and 13% with significant regional differences. [2] So, if the mortgage interest deduction is eliminated, then the aforementioned states might have numerous problems, including a smaller property tax base.

What exactly is the Mortgage Interest Deduction?

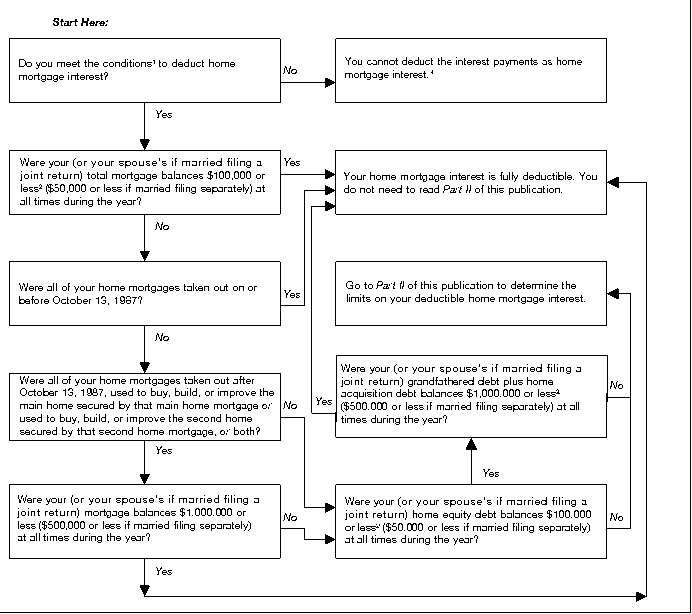

Generally, under IRC 163 the interest on a loan that is a qualifying mortgage is deductible. [3] There are many hoops to jump through to determine whether the loan qualifies. Here is the “simple” chart from the IRS:

As the chart shows, the main limitation to the home mortgage interest deduction is the amount of borrowing. Interest is deductible for home purchase debt up to $1,000,000. In addition to the purchase money debt the first $100,000 of home equity debt is deductible.

When I hear about Schedule A deductions, I immediately think about phase outs. The first potential backstop is the Alternative Minimum Tax. The AMT (which usually kicks in for incomes over $100,000) eliminates most deductions and replaces them with special tax rates and a special large AMT exemption. However, the AMT retains the full deduction for the purchase debt up to $1,000,000 and eliminates the deduction for home equity debt. [4]

The second limitation is the “Pease Limitation.” Pease gradually reduces the value of most itemized deductions for non-AMT taxpayers with high income (over $250,000). Pease does limit the value of all mortgage interest deductions. So for homeowners with over $250,000 Pease starts to limit the value of the deduction which should then affect the pricing pressure of elimination of the deduction.

The complicated nature of the mortgage interest deduction.

Creating a full law review type article is beyond the scope of this blog post. Rather, I would like to highlight some the narratives surrounding the home mortgage interest deduction and why simply stating the deduction should be reduced or eliminated is complicated in practice.

The primary argument against eliminating the mortgage interest deduction would induce housing prices to plummet by up to 15 percent and result in “trillions of dollars in wealth destruction.” [5] Well, why is the assumption that the mortgage interest deduction would destroy wealth? Won’t it just redistribute the inflated price from sellers to buyers? If that is true, then the justification of eliminating the deduction becomes more complicated because a second question must be asked: Who are we redistributing wealth to?

Second, not only would the lower prices redistribute from sellers to buyers, but, there would be real negative macroeconomic effects. Immediately eliminating housing subsidies would increase negative equity (if home prices go down 15%). This would then seemingly undermine consumer confidence and spending. That seems rather bad.

Third, besides the macroeconomic effects, what about the taxpayers expectation of the baked-in deduction when purchasing? “If, for example, Congress immediately eliminated the deduction without any related drop in marginal tax rates, a household expecting the deduction would be subject to a dual financial blow: a drop in home equity and higher tax liability. Without lowering marginal rates, that change would result in $215 in increased tax liability for households earning about $44,000 in after-tax income. For households earning approximately $72,000 in after-tax income, the change could increase tax liability by an average of $689.” [6]

Fourth, why is it assumed that the lowering of the mortgage interest deduction will lower rental pricing? Yes, there will be an initial shift to owner-occupied housing because of the reduced costs. This should result in an initial oversupply of rental housing which would lower rents. However, when there is excess supply, shouldn’t the assumption be that a reduction to rental housing construction will drop? If new supply drops, eventually then prices will rise again. “Over time, the government subsidies for home ownership will lower the long-run equilibrium price for rental housing, reducing the supply of rental housing below the level it otherwise would have been without government subsidies for home ownership.” [7]

Moreover, by lowering the mortgage interest deduction to $500,000, the goal would be to convert middle-income tenants into homeowners. Well, this credit worthy group are great tenants and prop up the value of rental real estate. If the tenant mix in changed to increase default risk, wouldn’t rental property values drop? Prices should drop. Which then begs the question, are we sure rents would drop? If the property has a higher risk profile, why do we believe that investors would bear that risk and not redistribute that risk to the tenants via higher rents?

Finally, many argue that the mortgage interest deduction is just the wrong instrument in encouraging home ownership. Professor Dennis Ventry in a 2012 Tax Notes article states:

“In the end, the net benefits of the MID are so skewed toward higher-income households that it is effectively worthless to lower-and middle-income taxpayers. Almost any other policy aimed at subsidizing owner-occupied housing would be more effective and would increase the progressivity of the income tax. Currently, the MID offers no help to three-quarters of all taxpayers; no help to two-thirds of taxpayers who claim the standard deduction; no help to more than half of all homeowners; no help to more than 20 percent of mortgaged homeowners; no help to renters; and very little help to the elderly who no longer service mortgages or who have too little taxable income to enjoy any savings from the deduction.” [8]

My point in this blog post is to challenge some of the thinking that the elimination of the mortgage interest deduction will fix all of the problems Dennis identifies. Yes, other instruments (like a credit) might be better. But, I would caution that any change will impact matters on many dimensions. What I initially thought of as a simple discussion has proved more nuanced and complicated in practice.

For example, let’s circle back to the chart. My first reaction (and probably still my current reaction) is who cares? After all, it is hard to envision a taxpayer getting a $1,000,000 loan with less income than $250,000. If you have over $250,000 in income, the mortgage interest deduction starts to be phased out and therefore there really should not be home price sensitivity to the tax at the upper boundary. So, will the elimination really matter? Maybe for the middle class; but if that is the targeted group there seems to be many other concerns that come into play.

Notes:

[1] Tax Reform Options: Incentives for Homeownership: Hearing Before the S. Comm. on Fin., 112th Cong. (2011), available at http://www.finance.senate.gov/hearings/hearing/? id=279c1381-5056-a032-5260-1ce326dfc82b (statement of Dr. Richard K. Green, Director, Lusk Center for Real Estate, University of Southern California).

[2] Richard K. Green et al., “Metropolitan-Specific Estimates of the Price Elasticity of Supply of Housing and Their Sources,” 95 Am. Econ. Rev. 334, 335 (2005) (finding significant price premiums associated with the MID) and Nicholaus W. Norvell, Transition Relief for Tax Reform’s Third Rail: Reforming the Home Mortgage Interest Deduction After the Housing Market Crash, 49 San Diego L. Rev. 1333, 1359 (2012).

[3] For a detailed explanation see IRS Publication 936 available at https://www.irs.gov/publications/p936/ar02.html

[4] This is actually a more complicated determination than it appears on face value. For example, what if I refinance my mortgage? See, for example, Rev. Rul. 2005-11 for the interaction of IRC sections 163 and 55 (available at https://www.irs.gov/pub/irs-drop/rr-05-11.pdf).

[5] Lawrence Yun (chief economist, NAR), “Why the MID Deserves to Stay,” Realtor Mag (Sept. 2010), available at http://realtormag.realtor.org/news-and-commentary/economy/article/2010/09/why-mid-deserves-stay.

[6] Nicholaus W. Norvell, Transition Relief for Tax Reform’s Third Rail: Reforming the Home Mortgage Interest Deduction After the Housing Market Crash, 49 San Diego L. Rev. 1333, 1359–60 (2012). But see Louis Kaplow, An Economic Analysis of Legal Transitions, 99 Harv. L. Rev. 509, 523-24, 577, 616 (1986) (arguing that taxpayers should not have a normative expectation that tax policy will never change and that investors should treat the risk of government policy changes like the risk associated with traditional market forces–by incorporating it into their overall analysis in deciding whether to make an investment).

[7] William T. Mathias, Curtailing the Economic Distortions of the Mortgage Interest Deduction, 30 U. Mich. J.L. Reform 43, 57 (1996)

[8] Dennis J. Ventry, Jr., The Fake Third Rail of Tax Reform, Tax Notes, April 10, 2012 available at http://www.taxhistory.org/www/features.nsf/Articles/0099D39CD6F0BC1D852579DC006EDFEE?OpenDocument

I got those numbers from a NLIHC report: http://nlihc.org/research/rare-occurrence

Note that discussions of the potential complications arising from limiting or eliminate the HMID are typically theoretical. Americans rarely look empirically at the British case. They successfully retrenched and finally eliminated their mortgage interest relief (MIR) between 1974 and 2000 with very few complications.

LikeLike

Thanks Josh for sending alone the source data! I did not have a problem with the chart and it seemed to provoke a nice discussion. Thanks for thinking of it.

LikeLike

Interesting; generally, this seems similar to the policy discussions about the federal income tax deduction for property taxes–I find it surprising that more people don’t speak about both the mortgage interest deduction and the property tax deduction in the same breath.

LikeLike