By: David Herzig

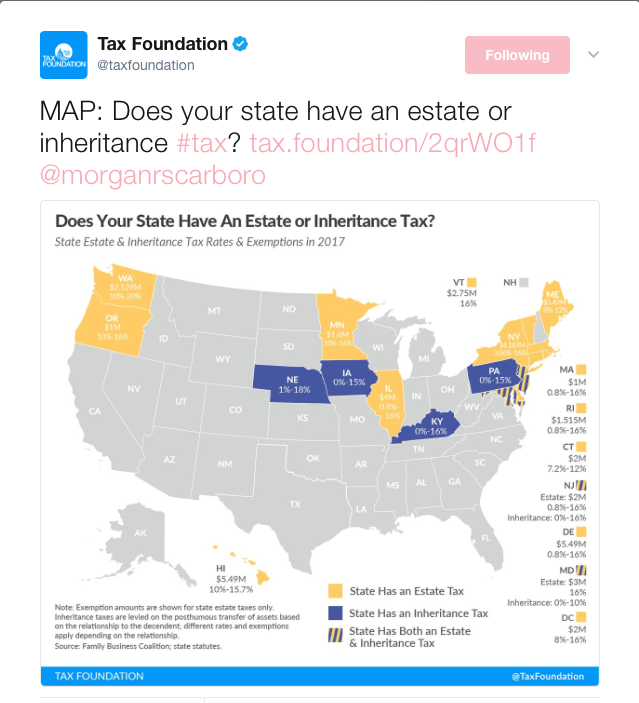

Last week Tax Foundation tweeted about the states that have either a state level estate or inheritance tax.

The map and subsequent conversations I have had reinvigorated my interest in the prospect of an estate tax. Briefly in this post, I wanted to say a couple things about the state level estate or inheritance tax, the map, and the effect of the Economic Growth and Tax Relief Reconciliation Act of 2001 (“EGTRAA“) on the prospects of the elimination of federal estate tax.

I’ll readily admit that it has been a while since I did an estate tax return. So, I needed some refreshing regarding the idiosyncrasies of the interaction between the state and federal taxes. Some recent history is not only necessary but illustrative of the prospects of permanent federal estate tax repeal.

Brief History of Switch From Credit to Deduction

Prior to the enactment of EGTRAA, the federal estate tax provided an tax credit for an amount paid because of a state level estate tax. The mechanics of credit was essentially a revenue sharing agreement for the tax collected between the federal government and the states – essentially, up to 16% of an estate’s value. The credit applied whether or not the state had an independent estate tax. This tax was known as a “pick-up” or “sponge” tax.

Under this regime, the estate would generally only pay the total federal amount.[1] For example, if your total tax was $1 million and the state credit was $160,000, you would remit $160,000 to the state (or states) of residence and $840,000 to the federal government. This credit tax regime permitted states that were barred by various state constitutions from enacting a state level estate tax to collect a tax. A state like Florida, for example, could collect an estate tax. Since the “sponge” tax was a give away, all 50 states and the District of Columbia had such taxes linked to the credit.

But EGTRAA changed the regime from a credit to a deduction for state taxes paid as of December 31, 2004. The switch meant two things: (1) the deduction was much lower therefore the federal government would collect more money; and (2) a state like Florida would no longer collect a share of the tax.

Well, what was the difference? What is the the magnitude of the impact of the change? During the potential sunsetting period of EGRTRAA, Urban Institute had estimates of the impact of restoration of the state credit in place of the state deduction. According to the white paper, “Restoration of the CSDT in 2013 would reduce federal revenues in 2013 by about $5 billion (assuming no behavioral changes and no additional estate planning) and increase revenue in 30 states that have dormant estate taxes by about $3 billion.” That is fairly significant.

After the shift, only states that either (i) had or (ii) enacted an estate or inheritance tax would be able to collect. Only a handful of states have an estate or inheritance tax and only a handful of states enacted a new estate or inheritance tax. If you are looking, ACTEC keeps a listing with some basic details of the various state level estate and inheritance taxes. [2]

As states struggle to balance budgets, the shift to the deduction for state taxes from a credit has caused states to contemplate various alternative regimes to raise the missing tax. For a summary of the state approaches see this Tax Analyst article. Unfortunately for states like Florida, are constitutionally prohibited from enacting an estate tax. Article VII, Section 5, (a) states “No tax upon estates or inheritances or upon the income of natural persons who are residents or citizens of the state shall be levied by the state, or under its authority, in excess of the aggregate of amounts which may be allowed to be credited upon or deducted from any similar tax levied by the United States or any state.” So without a credit system, Florida had to replace the lost revenues through alternative taxing instruments or increased taxes. By the way, Florida residents could amend the constitution (as unlikely as that sounds).

Which brings me back to a quick point on Tax Foundation map. I think that the way the map and issue are framed implies that these states have an additional burden that the other states do not. Let me clarify something – yes, technically, the map is accurate. If the federal estate tax is repealed, only these states will continue to have an estate tax. But, I think the map is a tad misleading since the current estate tax is really just an revenue sharing agreement (the states all have an estate or inheritance tax there is not more tax owed.). I know it is a small point, but, one that needs to be made.

Future of Federal Estate Tax

With time and reflection of the series of events, it now dawns on me that the switch to the deduction from the credit may have been a design feature not a design bug. [3] I think most pundits believed that the switch was more accidental (although somewhat necessary for CBO scoring] than purposeful. However, if the long term goal was repeal of the federal estate tax, then the switch was not accidental. Let me explain my thinking:

The switch caused a break from the “sponge” or “pickup” tax regime to a separate obligation. This put pressure on states to either (i) have an existing estate or inheritance tax, (ii) enact an estate or inheritance tax regime or (iii) lose out on the revenue stream. But, the federal government knew that a handful of states could not enact a regime because of constitutional constraints, and others would have a hard time convincing their electorate to add a new tax. The most likely outcome of decoupling the states from the the federal system would be a majority of the states could no longer rely on the federal tax. The benefit to this strategy is removal of states as stakeholders in the debate for the federal estate tax elimination.

After the switch states that either did not or could not enact an estate or inheritance tax would be indifferent to a federal elimination of the estate tax. Further, states that enacted or already had an estate or inheritance tax would be indifferent because the elimination of the federal estate tax would not effect them. Since the states became indifferent the pressure on the federal government from fairly power stakeholders disappears.

To say it another way, the main argument for eliminating the estate tax is that only about 0.1%, or 1 out of 700 estates, owed any estate tax and some 2,700 deaths raised about $14 billion in estate taxes.[4] Since the tax was limited in scope and revenue, the popular narrative is to eliminate the tax. Well, that argument will get push back when the states want $3 billion of taxes via the credit regime. Now that the states are decoupled, they do not care about the federal estate tax elimination proposals.

This makes me think that the elimination of the estate tax may be more realistic than many believe. I have been trying to think about which major stakeholders would show up to contest the elimination of the estate tax. Without the states at the table, the path is certainly easier for elimination.

Some Final Thoughts

If you are for the estate tax because of a concern that wealth continues to be concentrated at the top, this real development should give you pause. Further, if you want the estate tax to not only stick around but be more robust, you should think about structuring an estate tax that shares more revenues to the states; the more stakeholders the harder elimination becomes.

Notes

[1] I can remember a couple situations in Ohio and Kentucky where because of the class of takers, the state level tax due exceeded the credit slightly.

[2] If you are wondering, an estate tax and inheritance tax are the same thing with the only difference who is responsible for the tax.

[3]Although a friend pointed out that the switch made CBO scoring for the sunset easier. See https://www.cbo.gov/sites/default/files/107th-congress-2001-2002/reports/05-09-fedbudestimating.pdf.

[4] Tax Policy Center Table T13-0019 available at http://www.taxpolicycenter.org/numbers/displayatab.cfm?DocID=3775; and Chye-Ching Huang & Nathaniel Frentz, Myths and Realities About the Estate Tax, Center on Budget & Priorities (Aug. 29, 2013) available at http://www.cbpp.org/files/estatetaxmyths.pdf.