By: Sam Brunson

In August, the European Commission announced that Ireland had illegally granted state aid to Apple, and that it would be required to recoup over $13 billion in back taxes from Apple. (Surly coverage here.)

All of the analysis at the time was tentative, though, because, before it could release its decision, the EC had to redact it. And on Monday, it released the redacted version.[fn1] All 130 pages of the redacted version. So now we get to dig into its content.

I’m sure that at least some of my cobloggers are going to address the decision in the days and weeks to come, but I thought I’d give some preliminary thoughts.[fn2] (If you’d rather get my preliminary thoughts from the day of the release, and in audio format, I talked about it on Bloomberg Radio’s “Bloomberg Law.”)

Transfer Pricing

Like I said initially, the big deal is transfer pricing. Only it’s not transfer pricing in the way I thought it was. Rather, it’s like this:

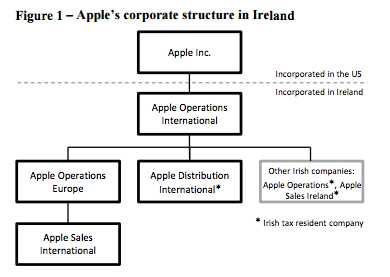

The opinion deals with AOE and ASI. Both are incorporated in Ireland, which has a worldwide tax system (meaning residents are taxed on their worldwide income). And corporate tax residency is determined by place of incorporation.

Except that there were a couple exceptions, including, notably, corporations that are subsidiaries of a resident of a treaty country that engage in trading activities in Ireland. That means that, although they were incorporated in Ireland, AOE and ASI weren’t taxable in Ireland on their worldwide income. Rather, they were treated as branches, and taxable only on their Irish income. The rest of their income was attributed to the “head office,” which technically didn’t exist, making it a quintessential example of Prof. Kleinbard’s “stateless income.”[fn3]

That raised the question of how to determine the portion of their profit that could be attributed to the fictional Irish branches. Why? When you have related parties engaged in business, you don’t have the usual market constraints on the pricing. So theoretically, the Irish branch could claim to have no profits, and the stateless “head office,” which pays no taxes to anybody, could claim to have all the profits. When that happens, most countries reserve the right to reallocate the costs to reflect the economics of the deal. Here, Ireland provided Apple with tax rulings that said how the profits would be split.

Under those tax rulings, the branches determined their share of net profits as a percentage of their branch operating expenses. While that seems odd, it is an indirect method of determining the allocable profits, and many countries allow that as one method of determining transfer pricing. (For Apple, it was a tremendously advantageous deal, too: in 2014, ASI had $25 billion in profits, but paid taxes of less than $10 million.)

The EC said this amounted to illegal state aid to Apple. Why? Because the transfer pricing method wasn’t an arm’s-length method: rather, it was one-sided.

And that, for me, was the really strange part of the ruling. Because the EC acknowledged that the OECD’s arm’s-length standard, while strongly recommended, wasn’t mandatory on member states. And Irish law did not require transfer pricing to meet the arm’s-length standard.

So the EC went to great lengths to explain why, although the arm’s-length standard wasn’t required, Ireland’s decision to not use the arm’s-length standard violated the EC treaty. And, on first reading, I found it’s explanation less than convincing.

Don’t get me wrong: this was totally a giveaway to Apple, and, although it’s complicated and administratively tough to actually do, I think the arm’s-length standard is central to transfer pricing. But the decision’s explanation of how the arm’s-length standard was required, even though it’s not actually required, didn’t convince me. Yes, as a normative matter, it should be the way transfer pricing is done, but it apparently wasn’t.

Why Doesn’t Ireland want the $13 Billion?

That question is a little misleading: the Irish people aren’t univocal on this. That said, the government is joining Apple in appealing the decision, so I’m going to treat Ireland as opposed.

And I can think of three reasons why it might not want the money. The first two are closely connected:

First, Apple employs 5,500 people in Ireland. And countries hate to lose jobs. Jobs for its citizens may be more important to Ireland than corporate tax revenue, and if it’s afraid Apple will relocate without the sweetheart tax deal, it may not want to drive Apple away.

Second and relatedly: presumably, Apple’s not the only company getting a good tax deal. To some extent, Ireland sells itself as a corporate and IP tax haven (though it wouldn’t use that language). If the EC can undermine its favorable tax treatment of companies, companies may rethink their Irish locations. And that would probably be bad.

The third reason struck me as I read the opinion: this opinion feels like an assault on Ireland’s tax sovereignty. Even if it wants the $13 billion, and even if it’s not worried about losing jobs, it may (justifiably) be uncomfortable with the EC’s willingness to say that it cannot follow its own tax laws. I don’t have a link for this proposition, but it’s my understanding that countries jealously guard their tax sovereignty. With the decision’s impingement on Ireland’s freedom to impose the tax system it chooses, Ireland may understandably be uncomfortable with the decision.

[fn1] I realize Monday—two days ago!—is forever in internet news cycle years, and that I should have blogged it back then. But it’s the week before Christmas and all through my house we’re racing to get all the Christmas prep done.

[fn2] Keep in mind that I don’t really know EC law or Irish law, so I’m taking that from the decision itself.

[fn3] Note that Irish law has since changed; now the exceptions only apply where the head office will pay taxes.