By: David Herzig

Yesterday on Twitter, Scott Greenberg (@ScottElliotG) posted the following tweet from Matt Bruenig.

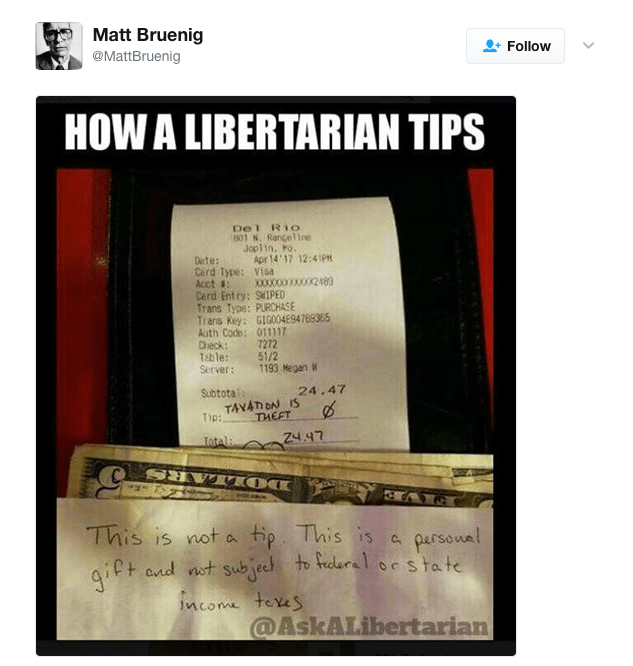

Well, David Gamage, Omri Marian, Andy Grewal and I had fun in 120 characters debating the quality of the tax advice provided on both the receipt and the note. Suffice to say: (A) this will be appearing on a number of basic income tax exams shortly;[1] and, (B) neither piece of advice provided by “Mr. Libertarian” seems to be correct. Both David and I pointed out that the “tip” did not seem to meet the old Duberstein detached and disinterested test. Clearly there was a quid-pro-quo; don’t spit on my food and I will give you extra money in addition to the bill.

Joking around about the gift/income distinction made me think that tipping is very tax inefficient. Assuming that what I said is true: tips are not gifts and they are income to the recipient. This means that the payment is not deductible by the payor (just personal consumption) yet income to the recipient, i.e. the server. If it is ordinary income to the recipient, then there should be a corresponding wage deduction, right?

Let’s assume the following counterfactual. The restaurant includes the tip as part of the bill. The restaurant pays the employee salary including the entire tip. Under this structure, the restaurant would receive an entire wage adjustment for the tip paid. The customer is still does not receive a deduction for paying the employee’s wages and the employee still pays the same amount of income tax. But the employer captures the unused deduction for wages by the customer. Theoretically, this deduction could be shared by all the stakeholders to reduce costs to all parties.

Who cares? Well, only economists and tax professors, probably. Back to finals preparation!

[1] Here is David Gamage’s hypo: customer leaves $1K and says, I just won the lottery and want to share some of my winnings as a “gift”.

Technically, if reporting is correctly followed, I think the tips should produce equivalent results either way. See https://www.irs.gov/businesses/small-businesses-self-employed/reporting-tip-income-restaurant-tax-tips.

Ignoring that, I think your counterfactual only works to produce tax efficiency if we assume in either case the tip is taken into the restaurant’s income but it’s only deductible in the counterfactual. (Or, more weirdly, that under either scenario the restaurant does not take the tip into income, but gets a deduction anyway in the counterfactual.) (Ignore that these assumptions seem hard to justifiy.)

Otherwise, e.g., if under the real scenario, the money is treated as a direct payment from customer to server without effect on the restaurant, then the real scenario is essentially equivalent to your counterfactual: Under the real scenario, the customer gets no deduction, the server gets ordinary income, and the restaurant has zero effect from the tip (because it neither generates income nor deduction from the tip); under your counterfactual, the customer gets no deduction, the server gets ordinary income, and the restaurant has zero effect from the tip (because it includes income from the tip only to deduct an equivalent amount).

This is very much like the fact that an allocation from a partnership to a partner is equivalent to a deduction to the other partners. And just as in that case, including something in income just to deduct it later is in fact a worse result than never including the income in the first place, due to potential limitations on deductions.

If in both cases the restaurant includes the tip in income and deducts it (which seems to be what should actually happen per the link at the top), we also get the same result in either scenario.

And lastly, of course we know many tips are unfairly tax efficient, thanks to the tax evasion technique of servers never reporting the tips…

Anyway, cheers and thanks for an interesting post.

LikeLike