By: David Herzig

With all the diversions this week, it was easy to miss that the House Committee on Appropriations posted on June 28th the Appropriations Bill for FY 2018. The bill seems to include a couple items that not many were expecting. So, I thought I would highlight some of the key provisions. Since it is Friday before a Holiday weekend, I’ll keep it short for now. There are four main provisions I will address: (1) IRS Targeting/Johnson Amendment; (2) ACA Penalties; (3) Conservation Easements; and (4) 2704 (Estate/Gift Tax).

I. IRS Targeting/Death of Johnson Amendment

First, is a clear response to the “targeting” of groups from the Lois Lerner Administration. In three separate sections (107, 108 and 116), the bill attempts to regulate the IRS, not through legislation, by via the purse. The last section (116) is an apparent end around of the Johnson Amendment.

Then section 116 reads:

SEC. 116. None of the funds made available by this Act may be used by the Internal Revenue Service to make a determination that a church, an integrated auxiliary of a church, or a convention or association of churches is not exempt from taxation for participating in, or intervening in, any political campaign on behalf of (or in opposition to) any candidate for public office unless:

(1) the Commissioner of Internal Revenue consents to such determination;

(2) not later than 30 days after such determination, the Commissioner notifies the Committee on Ways and Means of the House of Representatives and the Committee on Finance of the Senate of such determination; and

(3) such determination is effective with respect to the church, integrated auxiliary of a church, or convention or association of churches not earlier than 90 days after the date of the notification under paragraph (2).

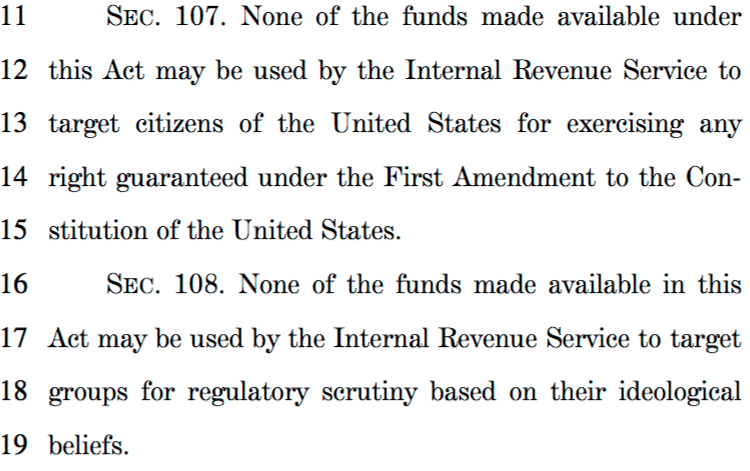

Sections 107 and 108

One could read sections 107 and 108 separately or with section 116. As stand alone sections, the intent seems as a clear response to the accusations made agains Lerner. These sections prevent the IRS from investigating any group for first amendment speech. Even without the later section 116, this section seems to prevent the IRS from investigating groups violating current laws. Should this pass, I would be interested to see if another Bob Jones University defendant even end up in court. Would this provision essentially gut the fundamental public policy doctrine?

Section 116 or the End of the Johnson Amendment

Many of us at Surly have written and opined about the Johnson Amendment including President Trump’s recent executive order. The Johnson Amendment is a provision that stops nonprofits that are registered as charities from receiving tax-deductible donations. The provision is thought to act as a backstop against turning churches into giant superpacs.

Section 116 seems to try to finish what President Trump started in his executive order. The section prohibits the IRS from enforcing the Johnson Amendment.

I have many thoughts, mostly for another day, but for now I wonder if the provision as written is even constitutional. The provision only makes reference to “churches.” I assume that this is just poor drafting. But assuming it is not this seems to be a provision that favors tax treatment of one religion over another. I can’t figure a rational basis for making this distinction let alone a basis that will survive strict scrutiny. It was suggested to me that if challenged, I suppose a court could try to read it to avoid the constitutional problem and read “church” to mean “place of worship” or something.

II. ACA Mandate Penalties.

Here the Appropriations bill is trying to eliminate the penalties for failure to carry health insurance. It is certainly interesting that during the same time that Trump/McConnell care is being debated in the Senate and a repeal and replace bill has already gone through the House, the House is still worried about the penalty provisions of the existing law. Sections 5000A and 6055 are the provision which requires individuals to maintain minimum essential coverage.

For now, I will leave it at this is interesting. Anyone want to guess how viable the insurance lobby and the business lobby thinks repeal and replace is?

III. Conservation Easements.

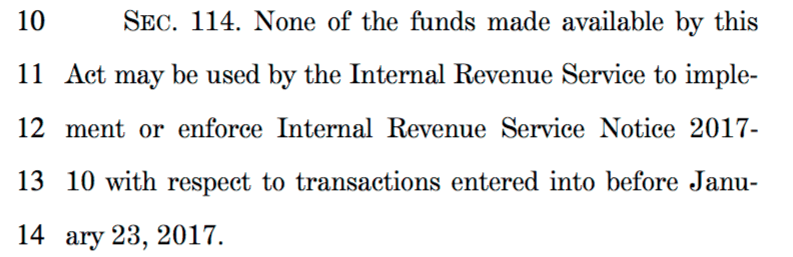

If you did not know that Notice 2017-10 listed syndicated conservation easements, this provisions would seem pretty benign. But, this is rather a big deal. I can’t remember ever seeing a syndicated group who promoted a listed tax shelter getting a get out of jail free card from Congress. As I read the section, if enacted, this would stop the IRS from getting promoter penalties against the syndicators of listed conservation easement transactions. That seems like a rather big deal (I’m sure KPMG, Anderson and E&Y wish they would have thought of this about 10 years ago). I will keep looking into other implications.

IV. Estate and Gift Tax 2704 Proposed Regulations.

Ok, so I know that like three of us still care about the estate and gift tax. But for those who care this is also a big deal. Last year, the IRS announced that new section 2704 regulations were going to be enacted. The practicing bar and related industries immediately mobilized. There were white papers drafted and trade organizations responses. The IRS was going after the “bread and butter” of the estate planning world, valuation discounts. Essentially, the IRS was going after the estate planning transaction in which Senior generation places marketable securities into a family limited partnership. Assume that the securities has a fair market value of $100x. Once Senior places the securities into the partnership, for decades estate planning professionals argued (successfully) that the gift or sale of the partnership units should be subject to valuation discounts for lack of marketability. control and the like.

Unfortunately, the proposed regulations go right after the heart of the estate planning industry. It was so important that the largest estate planning CLE in the country dedicated the first half of the first panel to the proposed regulations.

Once President Trump was elected two things happened: (i) priorities changed and (ii) the Executive Order on issuing regulations. The proposed regulations kind of stopped in their tracks. But this with this provision, the House GOP wants to ensure the proposed regulations never go anywhere by this section.