By: David Herzig

As the world braces for the upcoming Executive Order from President Trump,

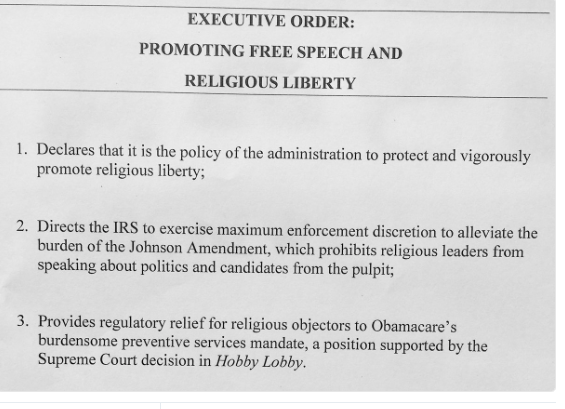

I wanted to take a minute and describe the Johnson Amendment. Later today, after the actual Executive Order is made public, Ben Leff will be writing up a more through post.

A couple of months ago President Donald Trump told the audience at the National Prayer Breakfast that he would “get rid of and totally destroy” the Johnson Amendment. Which raises the question: what is the Johnson Amendment. Because he brought it up at the National Prayer Breakfast, it also leads to the question of how does affects churches.

In 1954, without explanation, Lyndon Johnson proposed a small amendment to the tax law governing tax-exempt organizations: forbid them from endorsing or opposing candidates for office. One of the few consistent talking points during president-elect Donald Trump’s campaign was that this so-called “Johnson Amendment” should be repealed; since comprehensive tax reform is part of Trump’s plan for his first 100 days in office, the repeal may happen immediately. Continue reading “What is the Johnson Amendment?”

Back in June

Back in June