By: David J. Herzig

I, and others, certainly will have plenty of articles about what is wrong and right about the current tax cuts proposals. But, as I read the plan, I became frustrated with a proposal that was missing – fixing the Highway Trust Fund.

Infrastructure spending is a priority of this administration. In the spring President Trump announced his $1 Trillion ($1,000,000,000,000) infrastructure plan. According to the administration, the plan will rebuild the nation’s roads, tunnels and bridges. By September, the administration was contemplating how to pay for this spending from private sector credits to dumping the burden on the states.

The most recent discussion of how to pay for the $1 Trillion spend happened during discussions with the House Ways and Means members. According to the Washington Post, “At the meeting Tuesday, Higgins said Trump indicated the administration instead would seek to pay for infrastructure upgrades through direct federal spending — either by paying for projects with new tax revenue or by taking on debt.”

I was hoping, I know naivety, that another option would be discussed – pay for the infrastructure spending like always via the Highway Trust Fund which generates revenues via the gasoline and diesel tax. Since there would be a budgetary shortfall, maybe we should actually increase or fix the tax.

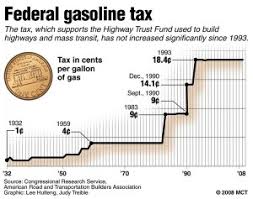

History of Gas Tax

I wrote about the gas tax for Tax Notes way back in 2013. As a refresher the gasoline and diesel tax was originally brought into existence in the 1930s as a general revenue raiser. In order to raise the tax in the future, it was necessary for presidents to tie the increase in the tax to actual benefits. For example, in the 1950s a correlation to the actual benefit was necessary under Eisenhower, thus, an earmarking of the tax to the dedicated Highway Trust Fund.

The tax worked rather well until the 1990s. As Joe Thorndike discusses “Congress broke the tax quite deliberately in the 1990s, when deficit hawks tried to transform it from a user fee to a deficit reduction tool.” By 1997, Congress sort of repaired the original link by redirecting all gas tax revenues back to the Highway Trust Fund. At the same time the continued is use the pegged amount of tax at 18.4 cents per gallon and 24.4 cents for diesel fuel. Did I mention that Congress did not index those rate? Kind of a big mistake. So, yes the rates have not changed since 1993.

The tax as it stands raises more than $30 billion annually, almost of all of which goes to the Highway Trust Fund. That is not enough to pay for current maintenance, let alone, a $1 Trillion spend. Currently, the shortfall, right now over $50 billion per year, is drawn from general revenue by Congress.

Proposed Fixes

A simple remedial fix would just be to re-index the tax. But the gasoline tax is such a political hot button that in the face of rising gas prices, presidential candidates even proposed eliminating the tax for the summer of 2008. Moreover, with truckers having it so hard with the estate tax, it is hard to believe that it would be politically via to raise the tax now. Even though the tax is also well below the per-gallon tax in other industrialized countries, including Germany ($6.28), the United Kingdom ($3.49), Japan (about $5.20), and Korea ($3.21).

Additionally, reindexing might be regressive. Although, there are studies that show it might not be as regressive as initially thought more work would have to be done to know for sure. If we are concerned there might be regressivity, then we can always employ additional instruments. But, reindexing the tax is a band-aid; the problem with the gasoline tax is in its design.

First, construction costs have continued to rise with inflation. Since 1993, the costs of roads is 55% higher. Second, the tax is a fixed amount (not a percentage of the sale) per gallon. Thus, if the price of oil rises or falls, the tax will not change. It depends solely on the number of gallons sold. There will be budgetary shortfalls if fewer gallons are sold because of vehicles’ increased fuel efficiency, or if there is equal consumption but greater use of the infrastructure — for example, if more miles are driven on the same number of gallons. Moreover, because the gasoline tax is not indexed to any metric, the problem is magnified because rates remain fixed over time while the cost of constructing and maintaining a transportation network inevitably becomes more expensive.

There are number of proposals that could fix the tax design to better get to the aforementioned problems. For example, a vehicle miles tax or vehicle miles traveled tax (VMT) would be better. Under a VMT, gasoline consumption would not be used as a proxy. Rather, the driver or a transponder would directly calculate the number of miles driven. There are three basic designs to a VMT: (1) a GPS-based mileage fee, (2) a pay-at-the-pump mileage fee, and (3) a prepaid manual mileage fee system.

According to the GAO, a mileage user fee would be more equitable and efficient. The effect on drivers would be an estimated ‘‘$108 to $248 per year in mileage fees’’ compared with the current $96 in gasoline tax. Obviously, that gasoline tax estimate does not take into account the deficiencies in the current structure.

There are also hybrid systems that account for political realities. If we want to switch instruments but do not want the baggage with the VMT, how about a VMT but in a more limited scope, it would be through the use of toll roads.

What would be nice if during this tax debate we actually start thinking about fixing the Highway Trust Fund so that we have more sustainable infrastructure spending mechanisms. Cutting taxes certainly increases the number of clickbait articles. Proposals that have real long term impact on how government can continue to provide for its most basic function, providing infrastructure, is a more important use of time.

Re-indexing the gas tax would certainly offset the disincentives created by abandoning the electric car credit!

LikeLike