Shu-Yi Oei

Diane Ring and I were invited to write a guest post for the On Labor blog, to explain the potential effects of tax reform on work arrangements for a labor law audience. There was some interest in tax reform among labor law experts in light of the New York Times article that ran on December 9, titled “Tax Plans May Give Your Co-Worker a Better Deal Than You.”

We wrote a pair of posts, describing the potential effects of tax reform on work arrangements (including decisions to form a passthrough or to classify oneself as an independent contractor).

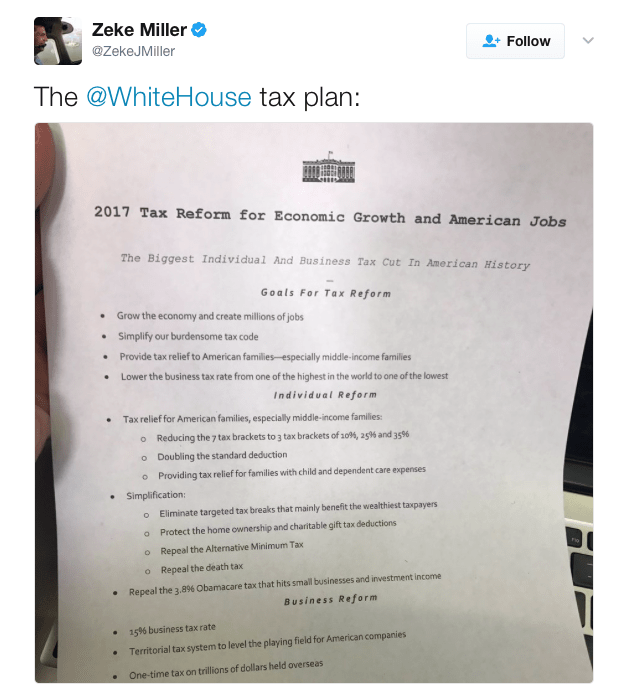

Something that struck us in our attempt to translate the policy issues for a non-tax legal audience was the sheer complexity of some of the new provisions in the new proposed provisions and the difficulty of discussing them with integrity–maintaining nuance, not oversimplifying or being hyperbolic, but still being understandable. As others have noted, the creation of the proposed tax legislation and the subsequent commentary on it have both happened very quickly. Our attempt to explain clearly the proposed legislative provisions to a non-tax legal audience and to discuss the policy issues at stake really highlighted for us the complexity of these proposed laws, the policy pitfalls, and the perils of operating at high speed.

In any case, here are the posts:

…The goal of this two-part blog post is to summarize for a labor law audience how the proposed tax legislation creates these outcomes and to highlight the important policy issues that observers and commentators might be concerned about. This Part 1 focuses on the statutory provisions, and Part 2 will discuss the key policy conversations that are taking place….

This post follows up on our prior post, which focused on the complex provisions of the proposed Senate tax bill. This post discusses some of the key concerns that have been expressed about the new tax bill. (Again, we focus here on the Senate version of the proposed legislation. The specifics of the analysis may change once we get the Conference version, though the broader policy and design questions are likely to persist.)

Today St. Louis University School of Law hosted the

Today St. Louis University School of Law hosted the